IRS Streamlined Filing: Catch Up on Expat Taxes for Free

The IRS offers a penalty-free amnesty program for US expats who missed tax filings. SFOP lets you catch up on 3 years of returns and 6 FBARs with zero penalties.

The IRS offers a penalty-free amnesty program for US expats who missed tax filings. SFOP lets you catch up on 3 years of returns and 6 FBARs with zero.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's a number that should rattle you: 9 million Americans live outside the United States. The IRS receives roughly 1.1 million returns filed from foreign addresses each year. That means somewhere between 7 and 8 million American expats are out of compliance—a quiet, sprawling noncompliance problem mostly driven not by tax cheats, but by people who genuinely didn't know they had to file.

The kicker? About 62% of expats who actually do file owe zero US federal tax after the Foreign Earned Income Exclusion and foreign tax credits. Most of these 7–8 million delinquent filers are one IRS letter away from a nightmare—and they wouldn't even owe money. They just need to file the paperwork.

There's a program built exactly for this situation. It's called the Streamlined Filing Compliance Procedures, and for Americans living abroad, it offers something almost unheard of from the IRS: a full penalty waiver. Zero. For catching up on potentially years of missed returns.

Most expats have never heard of it.

What Are the IRS Streamlined Filing Compliance Procedures?

Launched in 2012 and significantly expanded in 2014, the Streamlined Filing Compliance Procedures are an IRS amnesty-style program for Americans who failed to file their US tax returns, FBAR reports, or FATCA disclosures due to non-willful conduct—meaning negligence, honest mistake, or a good-faith misunderstanding of the law, not deliberate evasion.

There are two versions:

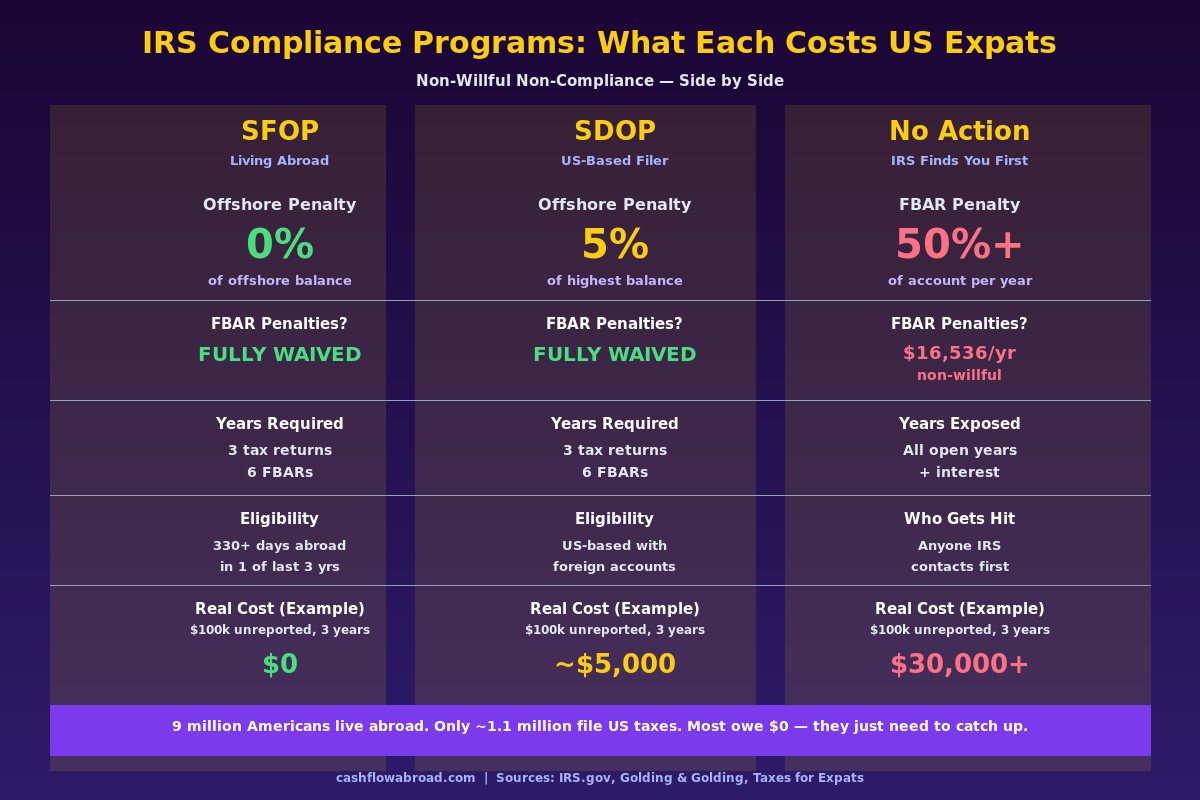

- SFOP (Streamlined Foreign Offshore Procedures) — For Americans who were genuinely living abroad. Penalty: $0.

- SDOP (Streamlined Domestic Offshore Procedures) — For US-based filers who had unreported foreign accounts. Penalty: 5% of the highest aggregate balance of unreported offshore assets during the 6-year lookback period.

If you've been living outside the US and weren't filing, SFOP is the relevant program—and its $0 penalty figure is not a typo or a loophole. It's the official mechanism the IRS designed to bring non-willful non-filers back into compliance without punishing people who simply didn't know the rules.

Who Qualifies for SFOP

SFOP eligibility has four requirements. You need to check every box:

- Physical presence abroad: You were physically outside the US for at least 330 full days in at least one of the three most recent tax years for which the filing deadline has passed. This is the same test used for the Foreign Earned Income Exclusion.

- Non-willful conduct: Your failure to comply must have been due to negligence, inadvertence, or honest misunderstanding—not intentional tax evasion. Checking "No" on Schedule B (foreign accounts question) while knowing you had foreign accounts crosses into willful territory.

- Not currently under IRS audit or investigation: The moment the IRS contacts you about your delinquency, the window closes. SFOP is only available to people who come forward voluntarily before the IRS finds them.

- Valid US Taxpayer Identification Number: SSN or ITIN required.

The non-willful standard is broad and generally favorable. Genuinely not knowing you had a US filing obligation because you paid taxes in your host country—a mistake millions of Americans make—qualifies. So does moving abroad young and never having been told by anyone that US citizenship creates a global tax obligation regardless of where you live.

What it does not cover: deliberate offshore structuring, actively hiding accounts, or using nominees to conceal assets. Those situations require the IRS Criminal Investigation Voluntary Disclosure Practice—a different program with real penalties but criminal prosecution protection.

What You Actually Have to File

The SFOP submission package is specific. Here's exactly what it requires:

| Document | Quantity | Notes |

|---|---|---|

| Federal Tax Returns (Form 1040) | 3 years | Most recent 3 years for which the filing deadline has passed. As of mid-2026: tax years 2022, 2023, 2024. |

| FBARs (FinCEN Form 114) | 6 years | Required if foreign accounts exceeded $10,000 aggregate at any point during any of the past 6 years. |

| Form 14653 | 1 | Signed certification under penalties of perjury that non-compliance was non-willful. This is the most important document—write it carefully. |

| Form 8938 (FATCA) | As applicable | Required if foreign assets exceeded FATCA thresholds (see below). Attached to each applicable 1040. |

You pay only the back taxes actually owed—calculated using all the deductions and exclusions you were legally entitled to, including the Foreign Earned Income Exclusion, which in 2025 is $130,000 per person (up from $126,500 in 2024). For many expats earning under that threshold in a foreign country with its own income tax, the amount owed is zero. You also pay statutory interest on any taxes owed—but zero penalty.

The FBAR Bomb Most Expats Don't Know About

Here's where the stakes become vivid. Most expats who haven't filed know they're missing tax returns. Far fewer realize there's a separate reporting obligation—the FBAR—with its own completely independent penalty structure.

The FBAR (FinCEN Form 114) is required if the combined maximum value of all your foreign financial accounts exceeded $10,000 at any single point during the year—even for one day. This is not an IRS form. It's filed separately with the Financial Crimes Enforcement Network (FinCEN), due April 15 with an automatic extension to October 15.

The penalties for not filing are severe:

| Violation Type | Maximum Penalty |

|---|---|

| Non-willful | Up to $16,536 per violation (2025 inflation-adjusted) |

| Willful | Greater of $165,353 OR 50% of account balance per violation |

| Criminal (willful) | Up to $250,000 fine and 5 years in prison |

Before the Supreme Court's 2023 ruling in Bittner v. United States, the IRS was assessing non-willful penalties per account, per year. Someone with 5 foreign accounts who missed 3 years of FBARs could face $225,000 in penalties despite technically never intending to evade anything. The Bittner ruling changed that: non-willful penalties now apply per form filed, not per account—dramatically reducing worst-case exposure for inadvertent non-filers.

But here's the thing: under SFOP, all FBAR penalties are completely waived. The Bittner ruling matters if you end up outside the program. If you qualify for SFOP, it's moot—you pay nothing.

This makes SFOP potentially worth tens or hundreds of thousands of dollars in avoided penalties for expats with multiple foreign accounts. For context on the full FBAR and FATCA reporting picture, the US expat banking and taxes guide covers how these accounts trigger overlapping obligations.

The FATCA Layer: Form 8938

FBAR and FATCA are not the same thing. Filing one does not satisfy the other. Many expats who know about FATCA assume they've handled FBAR—or vice versa—and end up with a gap.

Form 8938 (FATCA) is filed with your federal tax return and covers "specified foreign financial assets." The filing thresholds for expats living abroad are significantly higher than for US-based filers:

| Filing Status | Year-End Balance Threshold | At Any Point During Year |

|---|---|---|

| Single / MFS | $200,000 | $300,000 |

| Married Filing Jointly | $400,000 | $600,000 |

The thresholds are much more forgiving than FBAR's $10,000 trigger—but FATCA covers a broader universe of assets: foreign stocks held directly, interests in foreign entities, foreign life insurance contracts with cash value, and more. Real estate held directly does not go on Form 8938, though rental income from it is still taxable.

The penalty for not filing Form 8938 when required: $10,000, climbing to an additional $50,000 if you ignore IRS notices. Under SFOP, these penalties are also waived.

How the IRS Actually Tracks Non-Filers Abroad

Many expats operate under the assumption that living abroad makes them invisible to the IRS. FATCA ended that assumption permanently.

Since FATCA's implementation, foreign banks are legally required to report US account holders to the IRS or face a 30% withholding on their US-source income. This means your Swiss savings account, your German brokerage, your Canadian pension—the IRS may already know about them. The agency cross-references these reports against filed returns, which is how non-filers get flagged.

Additional detection vectors: passport applications and renewals, Social Security claims, information-sharing treaties with over 100 countries, and employer reporting from US multinationals. The "they'll never find me" strategy is increasingly a fantasy—and CARF, the global data-sharing successor to FATCA, is extending that reach further. See the full breakdown of how AI audits and CARF are ending expat financial invisibility.

The crucial point: SFOP eligibility disappears the moment the IRS contacts you. If you receive an audit notice, a CP notice about an unfiled return, or any direct IRS inquiry about your delinquency, you are no longer eligible for the program. At that point, your options become significantly more expensive.

SFOP vs. Other Programs: Choosing the Right Path

If you believe your non-compliance was willful—you knew about the obligation and deliberately chose not to comply—SFOP is not your program. Using SFOP falsely by certifying non-willful conduct on Form 14653 creates criminal exposure on top of whatever you were originally avoiding. The IRS Criminal Investigation Voluntary Disclosure Practice (VDP) exists for willful cases; it carries meaningful penalties but provides a formal path back into compliance and shields from criminal prosecution.

There's also the Delinquent FBAR Submission Procedures—a narrower option for expats who did file their tax returns but simply missed the FBAR. If all income from the foreign accounts was properly reported on US returns and there are no tax penalties, you can file late FBARs electronically with a brief explanatory statement and receive zero penalty. SFOP is the broader program for filers who missed both returns and FBARs.

The OVDP (Offshore Voluntary Disclosure Program) that used to handle many willful cases closed permanently in September 2018 and has not been replaced—only the CI Voluntary Disclosure Practice fills that role now, with different mechanics and less certainty on penalty outcomes.

The Form 14653 Is the Most Important Document You'll Write

The non-willful certification on Form 14653 is what unlocks the penalty waiver. It's a narrative statement—your explanation of why you didn't comply, signed under penalties of perjury. The IRS reviews these carefully.

A credible, specific Form 14653 explains:

- When and why you moved abroad

- What you believed about your US filing obligations and why

- How you discovered you were required to file

- What steps you've taken to come into compliance

Common non-willful narratives that hold up: moving abroad young without ever being taught about citizenship-based taxation, relying on an accountant who incorrectly said foreign taxes eliminated US obligations, being an "accidental American" (born in the US to foreign parents) who was raised without knowledge of US tax rules, or simply assuming a spouse handled it.

Weak Form 14653 statements—vague, generic, or internally inconsistent—can invite scrutiny. Most expats working with an experienced expat tax professional can prepare this correctly. Expect to pay $500–$3,000 for SFOP preparation depending on complexity; the savings in avoided penalties can be orders of magnitude larger.

A Real-World Cost Comparison

To make the math concrete: imagine you've lived in Germany for 4 years, earned €85,000 annually (roughly $92,000), paid German income tax, and maintained a €60,000 savings account. You didn't file US taxes because you assumed German taxes covered everything.

Using SFOP:

- File 3 years of 1040s. With the FEIE covering up to $130,000 in 2025, US taxable income is zero. Tax owed: $0.

- File 6 years of FBARs for the €60,000 account. Penalty: $0.

- Total IRS liability: $0 (plus accountant fees of $500–$2,000).

If the IRS finds you first (non-willful, post-Bittner):

- FBAR non-willful penalty: $16,536 × 6 years = $99,216.

- Failure-to-file penalties on any taxes owed: 5% per month, up to 25%.

- FATCA penalties if Form 8938 was required: $10,000–$60,000.

The difference between acting voluntarily and waiting: potentially $100,000+. Pre-Bittner, with penalties assessed per account, that figure was higher. And none of this requires willful intent—just the IRS getting to you before you got to them.

Maintaining Your US Financial Footprint While You Catch Up

Coming into compliance often raises practical banking concerns. Expats who catch up on taxes frequently want to consolidate foreign accounts to reduce future FBAR complexity, and they need to preserve their US banking access in the process.

A US mailing address is essential for keeping US accounts open while living abroad. A virtual mailbox service like Traveling Mailbox gives you a real US street address in one of 50+ cities, handles mail scanning and check deposits, and runs about $15/month. Critical for maintaining your IRS address on file and state domicile while abroad—and for keeping US banks from flagging your account for a foreign address.

For US banking, Charles Schwab International remains the gold standard for expat banking and brokerage—no foreign transaction fees, free global ATM reimbursements, and no history of closing accounts purely because the holder lives abroad. The full zero-fee expat banking stack covers the complete setup. For international transfers between accounts, Remitly covers most corridors at competitive rates.

The Bottom Line

The IRS built SFOP because it recognized an undeniable reality: millions of Americans abroad were non-compliant through ignorance, not malice, and threatening them with catastrophic penalties for paperwork errors was counterproductive. The program remains active, unchanged in its core mechanics, and is arguably the best deal in the US tax code for the people who qualify for it.

If you've been living abroad and haven't been filing—and especially if you have foreign accounts that crossed the $10,000 FBAR threshold—the calculus is simple: SFOP now costs you almost nothing. SFOP later, after an IRS notice, costs you the program itself. And no action costs you whatever the IRS decides to assess when they eventually match FATCA data to your non-existent return history.

The only people who regret using SFOP are the ones who waited until it was no longer an option.

For more on managing your US obligations abroad: the complete guide to the Foreign Earned Income Exclusion, the FEIE vs. foreign tax credit decision, and the PFIC trap that catches expat investors.

Financial disclaimer: This article is for informational and educational purposes only and does not constitute legal or tax advice. Tax laws are complex and subject to change. Consult a qualified US expat tax professional—a CPA or attorney experienced in international taxation—before making any compliance decisions. SFOP requires a signed perjury declaration on Form 14653; work with a professional to prepare it accurately.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 16, 2026

Expat Tax & FinanceJuly 16, 2026

FBAR for US Expats: FinCEN 114 Rules, Deadlines & Penalties

Who files the FBAR, 2026 penalties up to $16,536/year, the July 2026 closure of the late-filing lane, and what to do if you have missed years.

Expat Tax & FinanceJune 23, 2026

Expat Tax & FinanceJune 23, 2026

FBAR vs Form 8938: Expat Reporting Guide

US expats with foreign accounts over $10,000 must file FBAR. Learn how Form 8938 differs, current penalty amounts, and how to catch up.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.