IRS Streamlined Filing: How Non-Filing Expats Avoid $165K Fines

The IRS built a quiet backdoor for US expats who never filed a return abroad. Penalty: 0%. What it doesn't waive: interest on any tax you actually owe.

The IRS built a quiet backdoor for US expats who never filed a return abroad. Penalty: 0%. What it doesn't waive: interest on any tax you actually owe.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The IRS built a quiet backdoor for US expats who never filed a return abroad. Use it correctly and you walk away with zero penalties — not reduced penalties, not payment plans, zero. Miss the window and the same mistakes can cost you $165,353 per foreign account per year.

That backdoor is called the Streamlined Filing Compliance Procedures, and the State Department estimates anywhere from 5.5 to 9 million Americans live abroad. Most tax experts agree that a substantial share of them are behind on their filings — some by years, some by decades. If you're one of them, this is the most important tax document you'll read this year.

What the IRS Streamlined Procedures Actually Are

Streamlined Filing Compliance Procedures are a penalty-relief program the IRS launched in 2012 and expanded significantly in 2014. The pitch: if you failed to file US taxes while living abroad, and that failure was non-willful (meaning you genuinely didn't know the rules, not that you hid money), you can catch up on a limited window of back returns without facing the crushing penalties the IRS normally imposes.

There are two tracks:

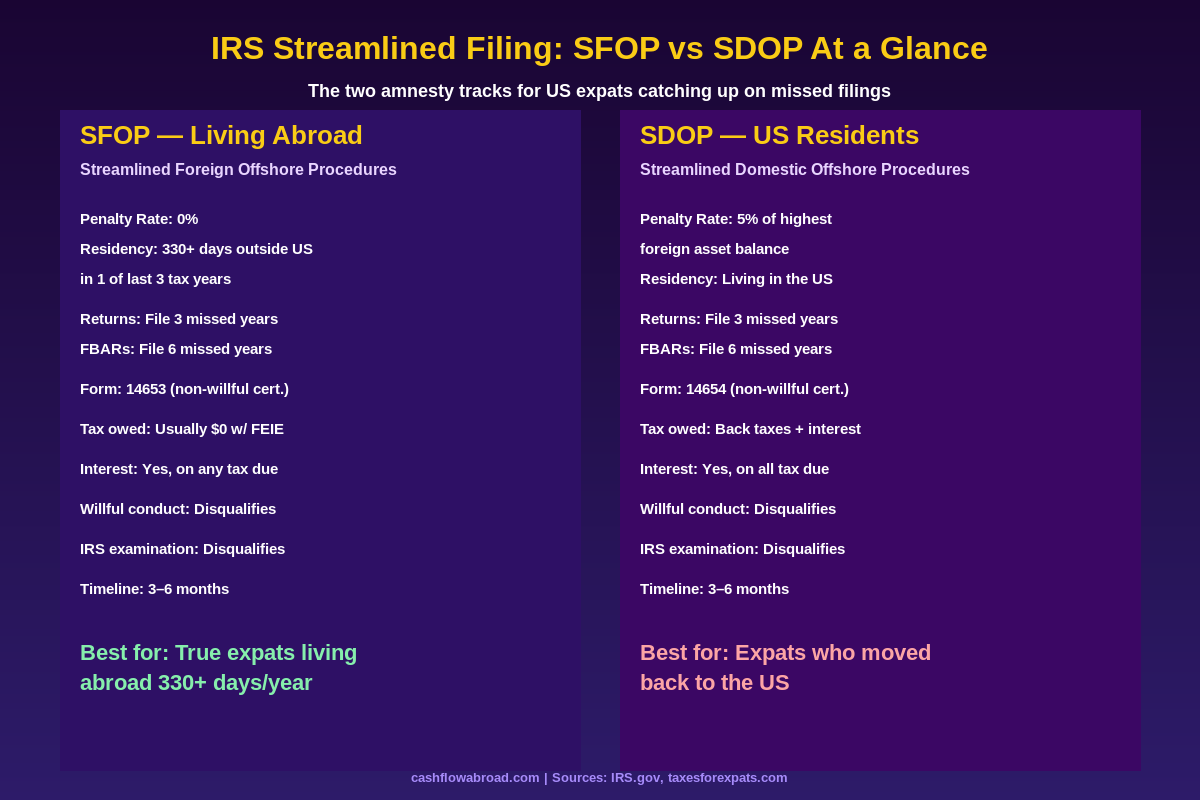

- Streamlined Foreign Offshore Procedures (SFOP) — for Americans currently living abroad. Penalty: 0%.

- Streamlined Domestic Offshore Procedures (SDOP) — for Americans who moved back to the US. Penalty: 5% of the highest aggregate balance of unreported foreign financial assets during the covered period.

That 0% versus 5% gap is why expats who are still abroad should act before they move home. Once you're a US resident again, you lose access to SFOP permanently.

The program waives failure-to-file penalties, failure-to-pay penalties, accuracy-related penalties, information return penalties, and FBAR penalties. What it doesn't waive: interest on any tax you actually owe.

SFOP vs SDOP: Which Track Are You?

The distinction comes down to where you live right now. The IRS uses a specific test for SFOP eligibility:

You must have had no US abode and been physically outside the United States for at least 330 full days in at least one of the three most recent tax years for which the filing deadline has passed. This mirrors the Physical Presence Test for the Foreign Earned Income Exclusion (FEIE), but it is not identical — the 330-day count for SFOP uses only full 24-hour days.

If you spent 330 days abroad in 2022, 2023, or 2024, you likely qualify for SFOP right now. If you've been back in the US for several years and only just discovered you were non-compliant, you're looking at SDOP — same paperwork, but with that 5% penalty tacked on.

| Feature | SFOP (Living Abroad) | SDOP (US Resident) |

|---|---|---|

| Penalty rate | 0% | 5% of highest unreported balance |

| Residency requirement | 330+ days outside US in 1 of last 3 years | Currently residing in US |

| Tax returns required | 3 most recent missed years | 3 most recent missed years |

| FBARs required | 6 most recent missed years | 6 most recent missed years |

| Certification form | Form 14653 | Form 14654 |

| Interest on tax owed | Yes | Yes |

The Full Eligibility Checklist

Before you start gathering documents, confirm you actually qualify. You are eligible for streamlined procedures if you meet all of the following:

- You are a US citizen, green card holder, or resident alien required to file US returns.

- Your noncompliance was non-willful. You didn't know about the requirement, misunderstood it, or received bad advice. You were not deliberately hiding assets.

- The IRS has not already contacted you. If you've received an IRS examination notice for any year, or if a civil examination of your returns has begun — even for unrelated reasons — you are disqualified. The program is strictly for voluntary disclosure before the IRS comes to you.

- You are not under criminal investigation.

- For SFOP: You meet the 330-day non-residency test for at least one of the three covered years.

The program is explicitly designed for people who simply didn't know the rules. Approximately 85% of what experts call "Accidental Americans" — US citizens raised abroad who may have never lived in America as adults — have never filed a return. Most genuinely didn't know they had to.

What You Actually Have to Submit

The filing package for SFOP has four components. There's no special form to trigger the program — you simply file the returns correctly and include the certification.

Three Years of Federal Tax Returns

You file the three most recent tax years for which the IRS deadline (including extensions) has already passed. For a submission in 2026, that typically means 2022, 2023, and 2024.

On these returns, you can retroactively claim:

- Foreign Earned Income Exclusion (FEIE): $126,500 for 2024, $130,000 for 2025. This eliminates tax on most expat employment income.

- Foreign Tax Credit (FTC): Offsets US tax dollar-for-dollar against taxes paid to your host country. You cannot claim both FEIE and FTC on the same income — pick whichever leaves you owing less.

- Foreign Housing Exclusion: Excludes a portion of qualifying housing costs on top of FEIE. Worth up to $35,000+ in expensive cities like London or Zurich.

The practical result: many expats who went through streamlined found they owed $0 in back taxes. Interest that accrued on zero is also zero.

Six Years of FBARs

An FBAR (FinCEN Form 114) is required for any year in which your foreign financial accounts collectively exceeded $10,000 at any point during the year. You file the six most recent missed years through FinCEN's BSA E-Filing system, separately from your tax returns.

Without streamlined, a non-willful FBAR violation can cost up to $16,536 per account per year. Willful violations: up to $165,353 per account per year, or 50% of the account balance, whichever is higher. Six accounts over six years at the non-willful rate alone could theoretically exceed $595,000 in penalties.

Under SFOP, all of that goes to zero.

FATCA Reporting and Other Information Forms

If you held foreign financial assets exceeding $200,000 on the last day of the year (or $300,000 at any point) while living abroad and filing single, you also file Form 8938 (Statement of Specified Foreign Financial Assets) with your 1040.

Other commonly missed forms depending on your situation:

- Form 5471 — If you owned 10%+ of a foreign corporation

- Form 8621 — If you held foreign mutual funds (PFICs)

- Form 3520 — If you received gifts from foreign persons or had foreign trusts

Form 14653: The Non-Willful Certification

This document makes or breaks your submission. Form 14653 is a signed statement explaining why your noncompliance was non-willful. It must be specific — "I didn't know" is not enough on its own. The IRS looks for a credible, fact-specific narrative.

Strong narratives include: you were a foreign national who acquired citizenship through a parent and never lived in the US as a tax filer; you moved abroad as a young adult and relied on a professional who incorrectly told you that living abroad eliminated US filing obligations; you were unaware that employer contributions to a foreign pension triggered separate reporting requirements.

Generic statements get scrutinized. Weak certifications may trigger an examination — the exact outcome you were trying to avoid.

How Much Will You Actually Owe?

For most genuine expats with wage or freelance income abroad, the answer is often close to nothing. A realistic example:

An American teacher in South Korea earning $65,000 equivalent per year who didn't file for four years (filing three under streamlined). She pays Korean income tax at 15–24%. Retroactively claiming FEIE eliminates all US federal tax on that income — she was below the exclusion cap every year. Her FBAR covered a single Korean bank account that peaked at $22,000. Result: $0 in back taxes, $0 in penalties, interest on $0 = $0. She pays only the tax preparation fees.

A more complex case: a freelance consultant in Germany earning $180,000 through a solo foreign company. FEIE covers $126,500. The remaining $53,500 may be subject to US tax, partially offset by German taxes paid via the Foreign Tax Credit. She might owe a few thousand in back taxes plus interest — still dramatically better than the six-figure FBAR exposure she faced outside the program.

One critical point: FEIE and FTC cannot be claimed on the same income. If your host country has a higher tax rate than the US (common in Germany, France, Scandinavia), the Foreign Tax Credit often produces a better outcome. A qualified expat tax preparer will model both scenarios.

For expat banking that works cleanly without triggering unnecessary complexity, Mercury offers a US-based business account well-suited to expat freelancers and entrepreneurs. For personal banking, Charles Schwab International gives you a US checking account with zero foreign transaction fees and fee-free ATM withdrawals anywhere in the world — which also gives you a valid US banking address for IRS correspondence.

Where People Get Into Trouble with the Certification

The biggest risk in a streamlined submission isn't the math — it's the certification. When you sign Form 14653, you're making a sworn statement. If the IRS later determines your conduct was willful, you're not just denied penalty relief — you've potentially provided an incriminating document in an IRS investigation.

The IRS defines non-willful as conduct resulting from "negligence, inadvertence, or mistake, or conduct that is the result of a good-faith misunderstanding of the law." Willful conduct means you knew about the requirement and deliberately chose not to comply — or acted with reckless disregard for the rules.

Red flags that suggest willful conduct (and may disqualify you or create legal risk):

- You actively moved money between accounts when you first heard about FATCA

- You used a nominee account or foreign structure to obscure ownership from the IRS

- You checked "No" on Schedule B Question 7 (foreign accounts) when you knew you had them

- A financial advisor specifically told you not to report certain foreign accounts

- You previously hired an attorney to help you avoid reporting obligations

If any of those apply, streamlined is likely not the right program. Consult an attorney — not a CPA — about the IRS Criminal Investigation Voluntary Disclosure Practice. It's more expensive and involves real penalties, but it provides protection from criminal prosecution that SFOP does not explicitly guarantee.

What Happens After You Submit

Streamlined is not a formal application with an approval letter. You file the returns with the IRS, submit the FBARs through FinCEN, and include Form 14653. Processing takes 3 to 6 months, sometimes longer during peak periods.

After that, one of three outcomes typically follows:

- Silence — the most common result. Returns are processed, any tax and interest owed is collected, and your record updates. No formal clearance letter arrives.

- A document request — the IRS may ask for additional records to support your narrative. This is routine, not a threat.

- An examination — returns filed under streamlined can be audited. If the IRS opens an examination and concludes your conduct was willful, all penalties are reinstated. This is uncommon for well-prepared submissions with credible narratives, but it happens.

After your submission, you must file correctly going forward. The program resolves the past — it does not provide ongoing immunity.

The 2026 expansion of CARF (Common Reporting Framework) means governments are now automatically exchanging financial data across 100+ countries. The era when non-filing expats could remain invisible to the IRS is closing fast — foreign banks are already reporting account data to local regulators who share it internationally under FATCA. Streamlined submissions have increased sharply as expats realize the window is narrowing.

When Streamlined Isn't the Right Option

Two other relief programs are frequently confused with streamlined:

Delinquent FBAR Submission Procedures — If you filed all your tax returns correctly but simply forgot FBARs, and you have no unreported income, you can file the missing FBARs directly through FinCEN with an explanation statement. No penalty if income was properly reported. No 6-year lookback, no certification form required. Far simpler and faster.

Delinquent International Information Return Submission Procedures — For missed forms like 5471 or 8938 where your income was correctly reported. Penalty abatement is available when reasonable cause is demonstrated.

| Situation | Best Program | Estimated Total Cost |

|---|---|---|

| Missed returns + FBARs, still abroad, non-willful | SFOP | $0 penalty + $1,500–$4,000 prep fees |

| Missed returns + FBARs, back in US, non-willful | SDOP | 5% of highest balance + prep fees |

| Filed returns, missed FBARs only, no unreported income | Delinquent FBAR Procedures | $0 + minimal filing time |

| Missed info forms (5471, 8938), income was reported | Delinquent Info Return Procedures | $0 with reasonable cause |

| Willful violations, criminal exposure | IRS Criminal Investigation VDP | Full penalties + $20,000–$60,000 in attorney fees |

DIY vs Hiring a Tax Professional

Straightforward cases — single filer, one country, wage income below the FEIE limit, one foreign bank account — can often be handled through expat-specialist tax services. Budget $1,500–$3,500 in professional fees for a clean 3-year submission. The cost reflects the narrative writing and multi-year complexity, not the arithmetic.

Hire an attorney (not just a CPA) if:

- You have any uncertainty about whether your conduct was willful

- You had foreign companies, partnerships, or trusts

- Your aggregate foreign accounts exceeded $1 million

- You previously checked "No" on Schedule B knowing you had foreign accounts

- You previously took steps specifically to conceal foreign income or accounts

Attorney-client privilege is meaningful here — communications with a CPA are generally not protected in an IRS examination, but attorney communications are. When the stakes involve potential willful findings, that distinction matters.

Staying Compliant Going Forward

Once you've gone through streamlined, annual compliance is simpler than most people expect. The core obligations for most expats:

- Form 1040 — filed by June 15 for expats (automatic extension from April 15), with FEIE or FTC applied

- FBAR (FinCEN 114) — filed by April 15, automatic extension to October 15 with no penalty extension form required

- Form 8938 — filed with your 1040 if assets exceeded thresholds

- Form 5471 — if you own 10%+ of a foreign company

Maintaining a valid US address is more critical than most expats realize. The IRS, your US bank, and your brokerage all need a US address for correspondence — and losing that address can create compliance gaps that snowball. A Traveling Mailbox provides a real US street address in 50+ cities with digital mail scanning and check deposit for $15/month. It's the simplest way to maintain your IRS correspondence address and US banking access while living abroad year-round — something many expats overlook until they need it urgently. We cover the full mechanics in our virtual mailbox guide for expats.

One more point: the statute of limitations for an unfiled return never expires. A 2015 return you never filed can still be examined in 2035. For a return you did file, the normal limitation is 3 years (6 years if you understated income by more than 25%). Filing — even late through streamlined — starts the clock. Not filing keeps it frozen indefinitely.

For the full picture on annual expat tax obligations, the US expat banking and taxes guide covers FBAR, FATCA, FEIE, and FTC in one place. And for anyone weighing whether the FEIE or Foreign Tax Credit produces a better outcome for their income level, the zero federal tax guide walks through the calculation with real numbers.

The Window Is Open — Act Before It Isn't

As of early 2026, the IRS confirmed that Streamlined Filing Compliance Procedures remain active. The program has no stated sunset date, but increased global financial data sharing under CARF and FATCA is making non-compliance progressively more visible — and more costly to resolve outside the streamlined framework.

If you qualify for SFOP and you're still abroad, submitting now while the penalty rate is 0% is categorically better than waiting. The moment the IRS contacts you — for any reason — the window closes permanently and the standard penalty structure applies. A $16,536-per-account-per-year non-willful penalty on a modest foreign savings account over six years adds up to sums that make the cost of getting current look trivial.

The IRS doesn't advertise this program. That makes it one of the most underused forms of relief available to the millions of Americans abroad who accidentally fell out of compliance — and one of the most time-sensitive decisions a non-filing expat can make.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Tax laws change frequently and individual circumstances vary significantly. Consult a qualified tax attorney or CPA specializing in US expat taxation before making decisions about your compliance situation.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 29, 2026

Expat Tax & FinanceJuly 29, 2026

Form 4868 vs 2350 for Expats

Compare Form 4868 and Form 2350 for expats, choose the right extension, and protect cash flow before claiming Form 2555.

Expat Tax & FinanceJuly 28, 2026

Expat Tax & FinanceJuly 28, 2026

US Mortgage as an Expat: Document Checklist

Prepare the income, asset, credit, translation, and closing documents lenders ask for when expats apply for a U.S. mortgage.

Expat Tax & FinanceJuly 27, 2026

Expat Tax & FinanceJuly 27, 2026

EU VAT for US Ecommerce Sellers

Learn when U.S. ecommerce sellers need EU VAT, OSS, or IOSS, and fix checkout rules before taxes erase profit margins overseas.