Ireland for US Expats: Taxes, Visas & the EU Passport Play

In the 12 months ending April 2025, 9,600 Americans packed up and moved to Ireland — a 96% jump from the year before. It's not cheap.

In the 12 months ending April 2025, 9,600 Americans packed up and moved to Ireland — a 96% jump from the year before. It's not cheap.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

In the 12 months ending April 2025, 9,600 Americans packed up and moved to Ireland — a 96% jump from the year before. For the first time in modern recorded history, more Americans are moving to Ireland than Irish are moving to the US. That stat alone should make you stop and think.

Ireland isn't a typical expat destination. It's not cheap. It has one of the highest marginal tax rates in the developed world — 52.2% once you stack income tax, the Universal Social Charge, and PRSI. For a high-income American, that sounds like a nightmare. But there are three reasons the numbers keep climbing: an EU passport available to millions of Americans for free, a remittance-basis tax rule that can legally shield offshore income from Irish tax, and a Dublin tech scene that pays serious money. The trick is knowing which angle applies to you.

Why Americans Are Choosing Ireland

Ireland checks boxes that few countries in Europe can match simultaneously. It's English-speaking, inside the EU, politically stable, and ranks among the safest countries in the world. Dublin is the EMEA headquarters for Google, Meta, Apple, Microsoft, and Amazon — which means both corporate transfer opportunities and a highly competitive local tech market paying US-level salaries.

Beyond the job market, Ireland has a disproportionate pull on Americans with ancestry ties. An estimated 32 to 40 million Americans claim some Irish heritage. For a meaningful chunk of that group, the Irish passport is not a distant aspiration but a legal right — one that unlocks the entire European Union at zero cost. That's the angle most financial content on Ireland completely ignores, and it's where we start.

The EU Passport Play: Irish Citizenship by Descent

Here's the hook that most expat coverage buries: if one of your grandparents was born on the island of Ireland, you are almost certainly entitled to Irish citizenship via the Foreign Births Register. You don't need to move to Ireland first. You don't need to pass a language test or prove any income. The application fee is a few hundred euros. Processing takes roughly 2 to 3 years due to backlogs, but once approved, you receive an Irish passport — which is also an EU passport, giving you the right to live, work, and retire in any of the 27 EU member states.

No points system. No salary threshold. No sponsoring employer. Just your grandparent's birth certificate, your parent's birth certificate, and your own. Ireland's Department of Foreign Affairs estimates that tens of millions of people globally are eligible but haven't claimed it. If you have any Irish ancestry, checking the Foreign Births Register eligibility before anything else is the single highest-leverage move in expat financial planning.

Already have Irish citizenship or in the process? You can move immediately and work for any employer in the EU, including in countries with far lower tax rates than Ireland — Portugal, Bulgaria, Georgia, Hungary. The Irish passport is worth far more than its face value as a gateway document. See our Geographic Arbitrage Playbook for how to stack this strategically.

Visa Options If You Don't Have Irish Ancestry

If the Irish grandparent route isn't available, US citizens can enter Ireland without a visa for up to 90 days. Staying longer and working legally requires one of the following:

Critical Skills Employment Permit — Ireland's priority pathway for in-demand workers. You need a job offer from an Irish-registered employer paying at least €40,904 annually (as of March 2026). Tech, engineering, healthcare, and financial services dominate the eligible occupations list. This permit allows family reunification immediately and converts to a General Work Permit after 2 years without a new job offer. Processing typically runs 4 to 8 weeks.

General Employment Permit — Broader role coverage, minimum salary of €36,605, but quota-based and slower. Requires the employer to demonstrate no suitable EU/EEA candidate was available (the Labour Market Needs Test). Better for roles not on the Critical Skills list.

Stamp 0 — Ireland's route for financially independent non-workers. No employment with Irish companies, but you can work remotely for foreign clients or live on passive income. Irish Immigration typically expects at least €50,000 per year in verifiable private income. This is the cleanest route for established freelancers and remote workers with non-Irish client bases — and it pairs directly with the remittance basis strategy covered below.

Naturalization to Irish citizenship without heritage ancestry requires 5 years of continuous legal residence. There is no investment fast-track.

Irish Taxes: The Brutal Math

Ireland taxes residents on worldwide income. Three charges stack on each other, and you need to understand all of them to see the real picture:

Income Tax: 20% on the first €44,000 for a single person; 40% on everything above. That 40% rate kicks in far earlier than most comparable countries — Germany doesn't hit 42% until €68,000; the US doesn't reach 37% until $609,000.

Universal Social Charge (USC): 0.5% on the first €12,012; 2% on €12,013–€28,700; 3% on €28,701–€70,044; 8% above €70,044. The USC was introduced as an emergency measure in 2011 during Ireland's financial crisis. Like most temporary taxes, it's still here fifteen years later.

PRSI (Pay Related Social Insurance): 4.2% on most employment income, rising to 4.35% from October 2026. In return, you accrue contributions toward Ireland's state pension and social insurance system.

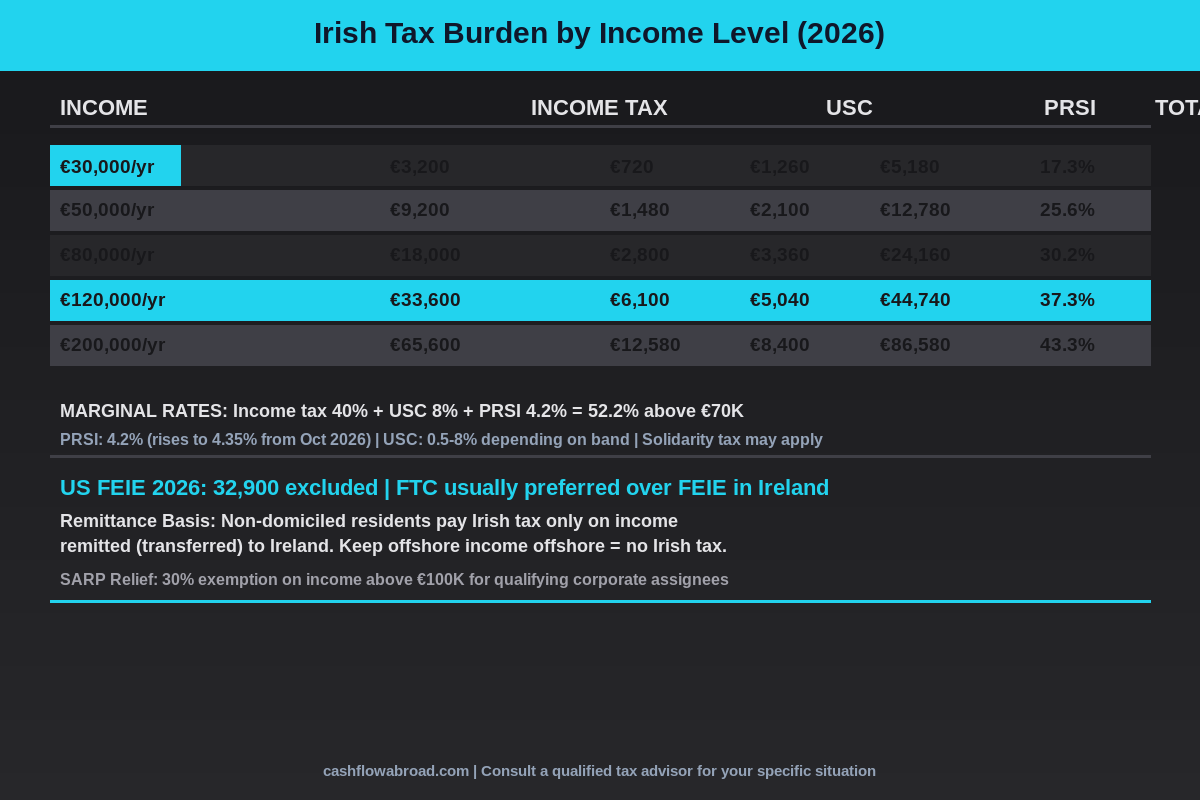

| Annual Income | Income Tax | USC | PRSI | Total Tax Paid | Effective Rate |

|---|---|---|---|---|---|

| €30,000 | €3,200 | €720 | €1,260 | €5,180 | 17.3% |

| €50,000 | €9,200 | €1,480 | €2,100 | €12,780 | 25.6% |

| €80,000 | €18,000 | €2,800 | €3,360 | €24,160 | 30.2% |

| €120,000 | €33,600 | €6,100 | €5,040 | €44,740 | 37.3% |

| €200,000 | €65,600 | €12,580 | €8,400 | €86,580 | 43.3% |

The effective rates look manageable up to €80,000. The problem is the marginal rate — every euro above €70,044 loses 52.2 cents to combined income tax, USC, and PRSI. If you earn €150,000, that last €80,000 gets sliced almost in half before you see it. For high earners without a tax mitigation strategy, Ireland is genuinely punishing.

Your US Tax Obligations Don't Disappear

America taxes on citizenship, not residence. Moving to Dublin doesn't end your IRS obligation. But the US-Ireland tax treaty and the Foreign Tax Credit mechanism mean most Americans in Ireland end up paying very little or nothing extra to the IRS.

The key question: FEIE or Foreign Tax Credit? In high-tax countries like Ireland, the Foreign Tax Credit almost always wins. The FEIE excludes up to $132,900 (2026) of foreign-earned income from US tax — powerful in zero-tax countries like the UAE or Cayman Islands. But in Ireland, you've already paid 30–43% to Irish Revenue. The FTC lets you credit those taxes dollar-for-dollar against your US liability. On €80,000 of Irish employment income, you've paid roughly €24,000 to Irish Revenue. Your US tax on that same income might be €18,000. The FTC wipes it out entirely, with excess credits carrying forward to future years.

Using FEIE in Ireland, by contrast, means you can't use the FTC for excluded income — and you lose the ability to make Roth IRA contributions on excluded amounts. This is the FEIE trap that costs American expats thousands. Full breakdown: FEIE vs Foreign Tax Credit: Which One Wins.

US expats in Ireland still need to file Form 1040, FBAR if foreign accounts exceed $10,000 at any point in the year, and potentially Form 8938 under FATCA. For the complete filing picture, our Complete US Expat Banking and Taxes Guide covers every form.

The Remittance Basis: Ireland's Underused Tax Shield

Here's what makes Ireland genuinely interesting for the right type of American: the remittance basis of taxation for non-domiciled residents.

Domicile in Irish tax law is not the same as residency. It refers to the country you consider your permanent home — your "domicile of origin." For virtually all Americans who move to Ireland, the US remains their domicile of origin unless and until they take concrete steps to change it. This matters enormously because non-domiciled Irish tax residents only pay Irish tax on:

- Income earned in Ireland

- Foreign income and gains that are remitted (transferred) into Ireland

Foreign income that stays in offshore accounts is not taxed by Irish Revenue. If you earn $200,000 from US investment dividends, rental properties, or foreign clients and leave that money in a US account, Ireland has no claim on it. You transfer only what you need for monthly living expenses — that amount gets taxed, the rest does not.

What makes Ireland uniquely valuable here: unlike the UK's non-domicile regime, Ireland charges no annual fee to access remittance basis treatment. The UK charges £30,000 per year after 7 years of residence, pricing out most non-ultra-high-net-worth individuals. Ireland's version is free indefinitely (with one caveat: after 15 years of Irish residence, a €200,000 annual charge may apply on foreign income above €1 million).

This strategy suits Americans with significant passive income — dividend portfolios, US rental income, royalties, or business profits from non-Irish entities — who live in Ireland on a fraction of their total earnings. The math: transfer €30,000 per year for living costs, pay Irish tax on that amount (~€5,000), leave $200,000 offshore untouched by Irish Revenue. You still owe US taxes on the offshore income, but you're not doubling up with Irish charges on top.

Important caveat: you cannot claim Foreign Tax Credit against Irish taxes on income you haven't remitted. The FTC strategy only applies to income you do bring into Ireland. For US-sourced investment income left offshore, US taxes apply, but Irish tax does not.

SARP: The Corporate Transfer Play

If your employer is assigning you to an Irish office, the Special Assignee Relief Programme (SARP) offers a 30% income tax exemption on earnings above €100,000, capped at €1 million. A qualifying employee earning €180,000 pays income tax as if they earned €124,000 — saving roughly €22,400 in Irish income tax per year.

The 2026 requirements: minimum base salary of €125,000, you must have worked for the same employer for at least 12 consecutive months outside Ireland immediately prior to the assignment, and the relief runs for a maximum of 5 years. If your employer is moving you from New York, Chicago, or San Francisco to Dublin, ask your HR team explicitly about SARP eligibility before signing the assignment paperwork. Most companies don't raise it proactively.

Cost of Living: Dublin vs Everywhere Else

Dublin is genuinely expensive. It consistently ranks as one of the priciest cities in Europe, driven almost entirely by a housing market squeezed by chronic supply constraints. A one-bedroom apartment in Dublin currently averages €1,570–€2,600 per month. Add groceries (€450/month), utilities (€160/month), and public transport (€120/month on a Leap Card), and a single professional realistically needs €3,200–€4,000 per month all-in.

What most articles miss: Ireland outside Dublin is a different financial planet. Cork, Galway, Limerick, and Waterford are culturally rich, well-connected cities where rent runs 25–40% lower than Dublin. Rural Ireland is startlingly affordable.

| Expense | Dublin | Cork / Galway | Rural Ireland |

|---|---|---|---|

| 1-bed apartment rent | €1,800–€2,600 | €1,100–€1,600 | €700–€1,100 |

| Groceries (1 person) | €400–€550 | €350–€450 | €300–€400 |

| Utilities | €140–€200 | €120–€180 | €100–€160 |

| Transport | €120 (Leap card) | €80–€100 | €50 (car needed) |

| Dining out (2x/week) | €250–€350 | €180–€280 | €120–€200 |

| Monthly total (approx.) | €2,900–€3,900 | €1,950–€2,700 | €1,450–€2,000 |

If your income is remote and non-Irish-sourced, the remittance basis lets you base yourself in County Clare, Kerry, or Connemara and live on €2,000/month transferred in while leaving the rest untouched offshore. Dublin is a lifestyle choice, not a requirement — and for geographic arbitrage purposes, the rest of Ireland is where the real value lies.

Banking and Healthcare Setup

Opening an Irish bank account requires proof of address, which creates the classic catch-22 when you first arrive. Bank of Ireland and AIB both offer personal accounts to new residents, but the process takes 2–4 weeks. N26 and Revolut work immediately as a bridging solution and are widely accepted across Ireland.

Keep your US banking infrastructure intact regardless. Irish banks don't offer the ATM fee reimbursements, US-dollar accounts, or brokerage access that expat finances require. Charles Schwab International remains the go-to for expats who need a US brokerage and checking account that reimburses all global ATM fees and won't close accounts due to foreign residence. If you run a US-based business while living in Ireland, Mercury handles US business banking cleanly from anywhere.

The IRS still requires a US mailing address on your return. A Traveling Mailbox virtual mailbox gives you a real US street address starting at $15/month — mail scanning, check deposits, and a physical address that keeps your banking relationships, IRS correspondence, and state domicile intact. Without a US address, financial institutions will eventually close accounts or flag returns. Full walkthrough: Why Every US Expat Needs a Virtual Mailbox.

Healthcare is a hybrid public-private system. The public HSE system is nominally free but operates with long waiting lists for non-emergency care. Most working expats pick up private insurance through VHI, Laya, or Irish Life Health at €800–€1,500 per year for individual coverage. If you're arriving on a Stamp 0 or in the gap before PRSI-based entitlements kick in, SafetyWing Nomad Insurance covers you internationally at around $56/month. Full comparison: Expat Health Insurance: SafetyWing vs Cigna vs Allianz.

For moving money between US and Irish accounts, Remitly consistently beats bank wire rates on USD-EUR transfers. For larger sums, see our Expat Money Transfer Guide for a full fee analysis across providers.

Who Should Move to Ireland

Ireland is the right move for a specific profile of American — not a universal answer.

Best fit: Americans with an Irish grandparent who want an EU passport as a foundation for continental mobility. Tech workers being transferred by US multinationals who qualify for SARP. Remote workers with substantial non-Irish passive income who can use the remittance basis to limit Irish tax exposure while living well outside Dublin. Anyone who wants English-speaking EU life with world-class healthcare and genuine cultural connection.

Poor fit: W-2 earners joining Irish companies at €100K+ without SARP — the 52.2% marginal rate is unforgiving. Americans chasing near-zero total tax — Ireland doesn't offer that and shouldn't be compared to Andorra, Georgia, or Paraguay on that dimension. Anyone seeking a cheap cost-of-living arbitrage — Dublin runs comparable to many major US cities, and even provincial Ireland won't dramatically undercut the US Midwest.

The setup that actually works financially is layering two or three advantages: the ancestry passport plus low-cost rural living, or SARP plus remittance basis on offshore investment income. Running a single lever — just the lifestyle, or just the tech salary — rarely pencils out for high earners compared to the alternatives.

Bottom Line

Ireland's 96% surge in American arrivals isn't primarily a tax-optimization story — it's a legal access and cultural pull story. The Foreign Births Register citizenship play is one of the most valuable free moves in personal finance for the estimated tens of millions of Americans with Irish grandparents. The remittance basis provides a legitimate structure for shielding offshore income for non-domiciled residents. And Dublin pays well for people who land in the right sectors.

But the 52% marginal rate is real, and there's no easy workaround for people doing standard Irish employment. Ireland rewards those who plan carefully around its tax structure — and charges everyone else at European rates. Run the numbers before you romanticize the pubs and the coastline.

This post is for educational purposes only and does not constitute tax or legal advice. US expat tax law is complex and highly individual — the interaction between US citizenship-based taxation and Irish residence rules creates scenarios that require professional guidance. Consult a qualified CPA or attorney experienced in US-Ireland cross-border taxation before making any financial decisions.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.