Your HSA Abroad: The Rules That Surprise Every Expat

You can spend your HSA at clinics worldwide — but contributing from abroad is a different story. The rules that trip up every expat who moves.

Can you use your HSA abroad? Contribute while on FEIE? Which expat plans qualify? The complete 2026 HSA rules for US expats living overseas.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Roughly 34 million Americans hold Health Savings Accounts with a combined balance north of $116 billion. When those account holders move abroad, most assume their HSA works the same way it always did. It doesn't — and the gap between what people expect and what the IRS actually allows creates some expensive mistakes.

The strangest part: the rules are almost backwards from what makes intuitive sense. You can spend your HSA at clinics across Southeast Asia, Latin America, and Europe without any IRS restriction. But whether you can add to it — that depends entirely on your health plan, and almost every international insurance product fails the test.

Why Moving Abroad Usually Kills New Contributions

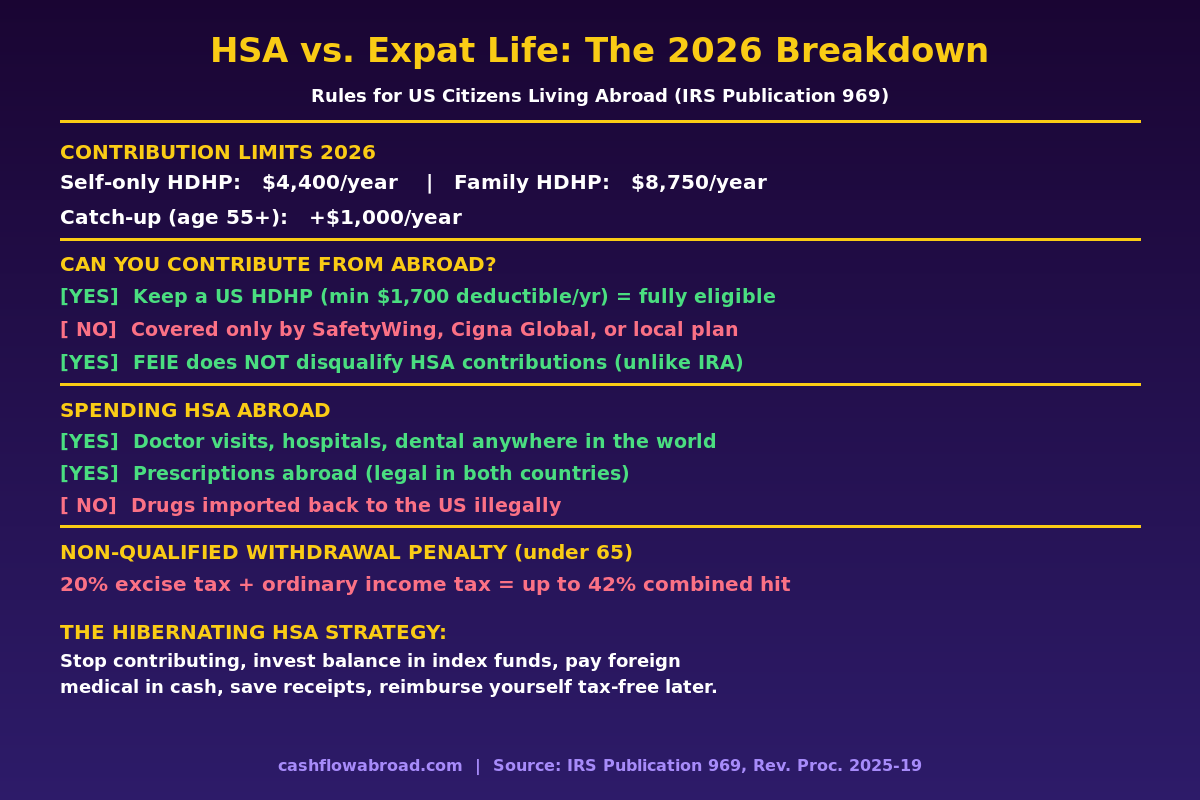

To contribute to an HSA in any given month, you must be enrolled in a qualifying High-Deductible Health Plan (HDHP). The IRS defines this precisely: for 2026, the plan must carry a minimum annual deductible of $1,700 (individual) or $3,400 (family) and cap out-of-pocket costs at no more than $8,500 (individual) or $17,000 (family). Crucially, the plan itself must be certified as an HDHP under US insurance regulations.

Foreign health plans are not. It doesn't matter if your policy in Thailand, Portugal, or Colombia has a $5,000 deductible — if it's not structured and regulated as a US HDHP, the IRS doesn't count it. The plan's deductible number is irrelevant; what matters is whether the plan qualifies under IRS Notice 2004-50 and Publication 969.

This knocks out the most popular expat insurance products immediately:

- SafetyWing Nomad Insurance — subscription-based international coverage with no minimum deductible structure; not HDHP-qualified. (SafetyWing's Essential plan isn't even available to US residents by design.)

- Cigna Global, Allianz Care, IMG Global — international expat plans, but not filed or regulated as US domestic HDHPs. Not HSA-eligible.

- Local foreign health plans — covered by your host country's national health system or a local insurer. Categorically excluded.

The narrow exception: if you work for a US employer that keeps you on a domestic HDHP (Cigna, Aetna, BCBS domestic) even while you're based abroad, you retain HSA eligibility. Aetna International also offers a "Traditional Choice Indemnity" plan with an HDHP variant specifically designed to be HSA-compatible — one of the very few international products that passes the test. Outside of those situations, new contributions stop the moment you swap US coverage for foreign coverage.

The FEIE Twist: Good News Most Expats Miss

Here's where the rules get counterintuitive in your favor. Unlike IRAs and Roth IRAs, HSA contributions have no earned income requirement.

IRA contributions require compensation — if your Foreign Earned Income Exclusion (FEIE) wipes out your entire taxable earned income, you cannot contribute to a traditional or Roth IRA. Many expats assume the same rule applies to HSAs. It doesn't. A retired expat, a spouse with no income, or someone whose entire salary falls under the 2026 FEIE cap of $132,900 can still contribute to an HSA — as long as they have qualifying HDHP coverage.

The trade-off is that the deduction may do nothing for you right now. The HSA deduction reduces US taxable income. If FEIE already reduces your taxable income to zero, the deduction has no immediate effect. But the contribution is still valid, the funds grow completely tax-free inside the account, and you can withdraw them tax-free for qualified medical expenses at any point.

High earners above the FEIE cap get the full benefit. Earn $175,000 abroad in 2026, exclude $132,900 via FEIE, and you have roughly $42,000 of taxable income. A $4,400 individual HSA contribution directly reduces that — real money at a 22% or 24% bracket.

What You Can Actually Use HSA Funds For Abroad

The spending rules are far more permissive than the contribution rules. Per IRS Publication 502, qualified medical expenses are not limited to US soil. Pay for surgery in Chiang Mai, dental work in Medellín, or a specialist consultation in Lisbon — all of it qualifies for HSA reimbursement, as long as the type of care would be a qualified expense if rendered in the United States.

What qualifies abroad:

- Doctor visits, specialist consultations, hospital stays, surgery at licensed facilities

- Dental and vision care (not cosmetic)

- Prescription drugs legally prescribed and consumed in the foreign country (also legal in the US)

- Physical therapy, chiropractic care, acupuncture

- Diagnostic lab work, X-rays, MRI scans

- Medical evacuation and ambulance services for medically necessary transport

- Lodging for medical travel: up to $50 per night per person when lodging is essential to the medical care

What doesn't qualify: cosmetic procedures, gym memberships, treatments illegal in the US (even if legal locally), and drugs you purchase abroad and import back to the US. Foreign transaction fees on your HSA debit card — typically 1–3% — also don't qualify.

Keep documentation. Foreign receipts should include the date of service, type of service, and amount in local currency. A receipt in Thai baht or Colombian pesos is fine; just make clear what it was for.

The Most Expensive HSA Mistake Expats Make

People cash out their HSA when they leave. Don't.

A non-qualified HSA withdrawal under age 65 triggers two simultaneous hits: a 20% excise penalty plus ordinary income tax on the same amount. If you're in the 22% bracket, a $10,000 withdrawal costs you $4,200 in taxes and penalties — you keep $5,800. Cashing out a $30,000 HSA could easily wipe out $12,600.

Your HSA is yours permanently. There's no "use it or lose it" expiration, no rule that it must stay active, no requirement to keep contributing to maintain it. The account sits there, grows, and waits. The only thing that changes when you move abroad without HDHP coverage is that you can no longer add to it — you can still spend existing funds and grow the balance tax-free indefinitely.

The Hibernating HSA Strategy

Healthcare in most expat destinations is dramatically cheaper than in the US. A doctor visit in Vietnam might cost $15. Dental work in Colombia runs 60–80% less than US prices. Minor surgery in Thailand is often cheaper than a US urgent care copay. Many expats pay entirely out-of-pocket and never touch their HSA for years.

This creates an unusual opportunity. If you invest your HSA balance in low-cost index funds — most major custodians (Fidelity, Lively, HSA Bank) offer ETF options — the account compounds completely tax-free. No tax drag on dividends, no capital gains events, no annual tax reporting on growth. It's one of the most tax-efficient investment wrappers that exists.

At age 65, the HSA changes character. Non-medical withdrawals stop incurring the 20% penalty and become subject only to ordinary income tax — identical to a traditional IRA. For qualified medical expenses at any age, withdrawals remain 100% tax-free. An expat who contributed aggressively during their US-working years, moved abroad at 40, stopped contributing, and let the account grow for 25 years in index funds arrives at retirement with a meaningful tax-advantaged asset they essentially forgot about.

The Receipt-Stacking Bonus

There is no IRS deadline on when you must reimburse yourself for a qualified medical expense. You can pay a doctor in Bali in 2026 and reimburse yourself from your HSA in 2046. The IRS only requires that the expense occurred after the HSA was established and that you have documentation.

The strategy: pay all foreign medical expenses in cash or on a regular credit card, photograph every receipt, store them in a folder, and let your HSA compound untouched. Years later, pull out a lump sum equal to your accumulated documented expenses — completely tax-free. Your HSA becomes a tax-free reserve you can access on demand, provided you've maintained records.

For an expat who lives cheaply in Southeast Asia or Latin America for 15 years, documented medical receipts of $15,000–$40,000 in cash payments are entirely plausible. That's a meaningful tax-free withdrawal available whenever you need it.

What the One Big Beautiful Bill Changed (And What It Didn't)

IRS Notice 2026-05, issued December 9, 2025, implements several HSA expansions from the One Big Beautiful Bill Act signed into law in 2025:

| Change | Effective | Helps Expats? |

|---|---|---|

| Telehealth permanently allowed pre-deductible without disqualifying HSA | Plan years beginning Jan 1, 2025 (retroactive) | Only if you have a US HDHP |

| ACA Bronze & Catastrophic plans qualify as HDHP | Jan 1, 2026 | Only with a US address and ACA plan access |

| Direct Primary Care (DPC) arrangements allow HSA contributions | Jan 1, 2026 | No — DPC is a US-domestic model |

| Foreign/international plans qualify as HDHP | Not applicable — still excluded | No change for expats on foreign-only coverage |

The OBBBA expansion benefits US-based workers meaningfully. For expats on foreign-only coverage, it changes nothing. International health plans still don't qualify. The ACA bronze plan change matters only if you maintain a US address and can access Exchange plans — which is itself a challenge for full-time expats.

2025 and 2026 HSA Contribution Limits at a Glance

| Coverage Type | 2025 Limit | 2026 Limit |

|---|---|---|

| Self-only HDHP | $4,300 | $4,400 |

| Family HDHP | $8,550 | $8,750 |

| Catch-up contribution (age 55+) | +$1,000 | +$1,000 |

| HDHP minimum deductible (self-only) | $1,650 | $1,700 |

| HDHP minimum deductible (family) | $3,300 | $3,400 |

| HDHP max out-of-pocket (self-only) | $8,300 | $8,500 |

| HDHP max out-of-pocket (family) | $16,600 | $17,000 |

Source: IRS Revenue Procedures 2024-25 and 2025-19.

What to Do With Your HSA Before and After Moving Abroad

Before you leave: Max out your HSA contribution for the year. Under the "testing period" rule, you can contribute the full annual limit even if you'll only be HDHP-eligible for part of the year — provided you remain HSA-eligible through December 1st of the following year. Front-loading $4,400 or $8,750 before you lose HDHP access is worth the effort.

Invest the balance. Check whether your custodian charges fees on uninvested cash. Fidelity and Lively allow you to invest the full balance in ETFs with no minimum cash threshold. Move the funds into a diversified index fund and leave it.

Consider keeping a US HDHP if your income is materially above the FEIE cap. The math on maintaining HDHP coverage abroad: a bare-bones plan might cost $250–450/month ($3,000–$5,400/year). At a 24% marginal rate, a $4,400 HSA deduction saves $1,056. That doesn't pencil unless your taxable income above the FEIE exclusion is large enough to make the deduction savings meaningful. Run the numbers for your specific situation.

Maintain a US address. Some HSA custodians flag foreign addresses and may restrict account access or send tax forms to unreliable foreign mail. A virtual US address from Traveling Mailbox ($15/month, real US street address with mail scanning) keeps your HSA custodian happy and preserves your US banking and domicile infrastructure simultaneously.

Start the receipt folder today. Date-stamped digital photos of medical receipts paid abroad are your ticket to future tax-free withdrawals. There's no minimum or maximum — every qualifying expense counts.

For broader strategy on US financial accounts while abroad, see our guides on expat banking and taxes and IRA and 401(k) strategy for expats. If you're deciding between FEIE and Foreign Tax Credit — which has downstream effects on your HSA deduction value — the FEIE vs. FTC guide walks through the trade-offs. For expat health insurance options that won't qualify for HSA contributions but provide solid coverage, the expat health insurance comparison covers the major plans.

The Bottom Line

Your HSA doesn't become useless when you move abroad — it becomes a different kind of asset. You probably can't add to it without maintaining expensive US HDHP coverage, but the balance you've built grows tax-free, can be spent on qualified medical care anywhere in the world, and converts to a penalty-free retirement account at 65. The receipt-stacking approach turns years of cheap foreign healthcare into a future tax-free withdrawal that most people never plan for.

The expensive mistake is treating your HSA as a relic of your US life and cashing it out. It travels with you. Understand the rules and use it accordingly.

Financial disclaimer: This article is for informational and educational purposes only. It does not constitute tax, legal, or financial advice. HSA rules are complex and highly situation-specific. Consult a qualified tax professional with experience in US expat taxation before making decisions about HSA contributions, investments, or withdrawals. IRS Publication 969 and Publication 502 are the authoritative sources for HSA eligibility and expense rules.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Health & InsuranceMay 18, 2026

Expat Health & InsuranceMay 18, 2026

The Expat HSA Guide: Triple Tax-Free Medical Savings Abroad

How US expats can use their HSA for tax-free medical expenses worldwide, who can still contribute abroad, and how FEIE interacts with HSA deductions.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.