Most US expats close their HSA — or stop thinking about it entirely — the week they land abroad. That's a mistake worth, conservatively, $180,000 in tax-free retirement savings. The account doesn't expire. The money doesn't disappear. The IRS doesn't care which country your doctor practices in. What changes when you move abroad is narrower than you think.

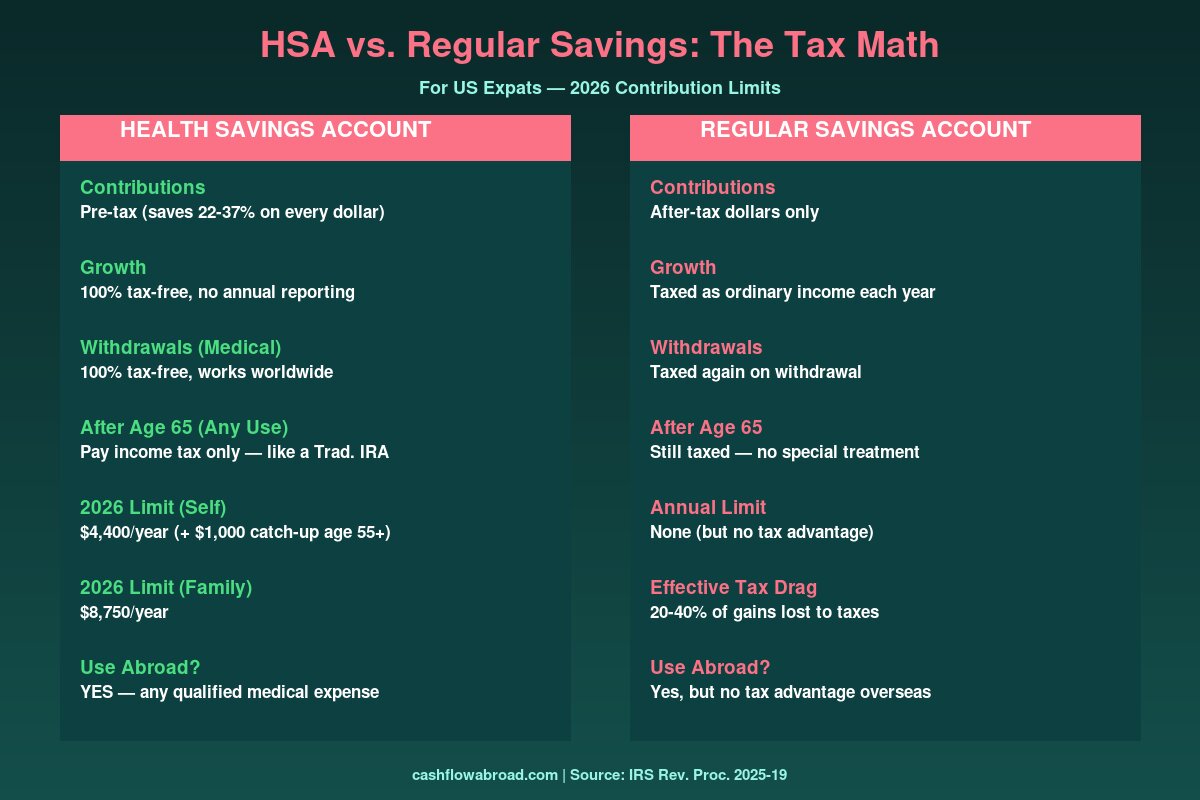

The Health Savings Account is the only financial account in the US tax code with a triple tax advantage: contributions go in pre-tax, growth compounds tax-free, and withdrawals for qualified medical expenses come out tax-free. A Roth IRA only gives you two of those three. A 401(k) gives you one. The HSA, if you play it right, gives you all three — and you can spend it at a dentist in Medellín or a hospital in Bangkok just as easily as one in Chicago.

What Actually Changes When You Move Abroad

Here's the thing most expats get wrong: they conflate losing contribution eligibility with losing the account. These are entirely different things.

To contribute to an HSA, you must be enrolled in a qualifying High-Deductible Health Plan (HDHP) and have no other disqualifying coverage. When you leave the US and enroll in foreign health insurance — a SafetyWing Nomad plan, local coverage in Mexico, or a private policy in Portugal — that foreign plan doesn't meet IRS HDHP criteria. Contribution eligibility pauses.

But the account itself? Fully intact. Your existing balance stays invested. It keeps compounding. You can still spend it on qualified medical expenses anywhere in the world. Nothing closes. Nothing gets penalized.

The three things that are always true for expats with existing HSAs:

- Your balance remains invested and grows tax-free

- You can withdraw for qualified medical expenses globally, penalty-free

- After age 65, you can withdraw for any reason (pay ordinary income tax on non-medical, just like a traditional IRA)

The 2026 HSA Contribution Limits

For those who can maintain or establish qualifying HDHP coverage while abroad, the 2026 limits are:

| Coverage Type | 2026 Contribution Limit | Catch-Up (Age 55+) | Effective Maximum |

|---|---|---|---|

| Self-Only HDHP | $4,400 | +$1,000 | $5,400 |

| Family HDHP | $8,750 | +$1,000 | $9,750 |

The HDHP minimums for 2026: a minimum annual deductible of $1,700 (self-only) or $3,400 (family), and an out-of-pocket maximum no higher than $8,500 (self-only) or $17,000 (family).

The 2026 Rule Change That Helps Some Expats

IRS Notice 2026-5, released December 2025, expanded which plans qualify as HDHPs. Starting in 2026, bronze-tier and catastrophic health plans qualify as HDHPs regardless of deductible structure, and telehealth services can be covered before the deductible without disqualifying the plan.

This matters for expats who want to maintain HSA contribution eligibility. A US catastrophic plan — the cheapest category, designed for healthy people — now works. Several catastrophic plans for a 35-year-old cost $80–$150/month on healthcare.gov. Pair that with local foreign insurance for day-to-day care, and you're back to contributing $4,400/year into the most tax-efficient account that exists.

One important caveat: you cannot have "other coverage" that covers benefits before the HDHP deductible kicks in. Most foreign insurance policies, including SafetyWing's Nomad Insurance, are generally not classified as primary US-style health coverage in the same way, but this area is unsettled. Confirm with a qualified expat tax advisor before continuing contributions from abroad.

The Math: Why Abandoning Your HSA Costs $180,000

Let's run two scenarios for a 40-year-old expat who moves abroad and either keeps contributing $4,400/year (self-only) or stops entirely:

| Scenario | Annual Contribution | Years | 7% Annual Return | Value at 65 |

|---|---|---|---|---|

| Keeps contributing | $4,400 | 25 | 7% | $283,000 |

| Stops contributing | $0 | 25 | 7% | Existing balance only |

| Family coverage | $8,750 | 25 | 7% | $563,000 |

That $283,000 is entirely tax-free if spent on qualified medical expenses. Spent on anything else after 65, it's taxed as ordinary income — the same as a traditional IRA, but with 25 years of no annual tax drag. A comparable taxable brokerage account generating the same returns would net roughly $70,000–$100,000 less after long-term capital gains taxes, depending on your bracket.

Using HSA Funds for Medical Care Abroad

The IRS defines "qualified medical expenses" by type of service, not geography. As long as the expense meets the IRS definition under Section 213(d), it's eligible — whether the doctor's office is in Lisbon or Louisville.

What qualifies:

- Doctor visits, specialist consultations, urgent care abroad

- Dental and orthodontic care (a major reason expats choose Mexico and Colombia)

- Vision care: eye exams, glasses, contact lenses, LASIK

- Prescription medications, including those purchased abroad

- Mental health services: therapy, psychiatry

- Medical tourism procedures: surgery, major dental, fertility treatments

- Ambulance services, hospital stays, lab tests

What does not qualify (even if your foreign insurer covers it):

- Gym memberships, vitamins, supplements (without a prescription)

- Cosmetic procedures not medically necessary

- Nonprescription drugs purchased outside the US

- Health insurance premiums in most cases

The documentation rule is non-negotiable: keep every receipt. It should include the date of service, patient name, provider name, type of service, and amount paid. The IRS doesn't audit every HSA withdrawal, but when they do, documentation is everything. A dedicated folder in Google Drive — one receipt per visit — takes 30 seconds and could save you thousands.

The HSA Investment Strategy: Don't Leave It in Cash

Most people with HSAs have them sitting in a money market or savings sub-account earning 2–4%. That works for an emergency fund — it doesn't work for a tax-free wealth-building account. The HSA's power comes from long-term compounding, and that only works if you're invested in something that actually grows.

The three best HSA custodians for expats who want genuine investment access:

| Custodian | Annual Fees | Investment Minimum | Notable Options |

|---|---|---|---|

| Fidelity HSA | $0 | $0 | Fidelity Zero funds, full brokerage access |

| Lively HSA | $0 (individual) | $0 | TD Ameritrade integration, ETFs |

| HealthEquity | $0–$3.95/month | $1,000 | Vanguard funds, wide selection |

Fidelity's HSA charges zero fees and offers the Fidelity Zero Total Market Index Fund (FZROX) — no expense ratio, no minimum. For an expat who won't be making frequent small transactions, Fidelity is the cleanest option. You'll want a US mailing address to maintain the account; a virtual mailbox like Traveling Mailbox handles that for $15/month and keeps your US domicile intact for banking and IRS purposes.

The optimal long-term strategy: invest everything in index funds and pay all current medical expenses out-of-pocket. Save every receipt. Years later — even decades later — you can reimburse yourself from the HSA with no time limit. The IRS doesn't require reimbursement in the same year as the expense. A $5,000 dental surgery in Thailand paid out-of-pocket today can legally become a $5,000 tax-free HSA withdrawal at age 60 — after that money has compounded for 20+ years.

The Age-65 Retirement Hack

The penalty for non-medical HSA withdrawals vanishes entirely at 65. Before 65, using HSA money for non-medical reasons costs a 20% penalty plus ordinary income tax. After 65, the penalty disappears — you pay ordinary income tax on non-medical withdrawals, exactly like a traditional IRA, but with the permanent option of tax-free medical withdrawals throughout your lifetime.

This means the HSA functions as a backup IRA with an opt-in bonus: if you have significant qualified medical expenses, it outperforms a Roth IRA. If you don't, it performs identically to a traditional IRA. There's no scenario where it's worse than both — which is why financial planners who specialize in expat clients increasingly treat the HSA as the second account to fill after capturing an employer 401(k) match.

What to Do Before You Leave the US

If you're planning a move abroad in the next 6–12 months:

- Maximize your contribution before you lose HDHP eligibility. The pro-rated rule lets you contribute for each month you're covered. Leave in July? That's 6 months of contributions ($2,200 for self-only in 2026).

- Move to a zero-fee custodian before you go. Employer HSAs often charge $2–$4/month. Roll to Fidelity or Lively before departure.

- Invest the entire balance in index funds. Don't leave it in the default money market account.

- Keep your US address active. A virtual mailbox gives you a permanent US street address for your custodian, IRS, and US banking like Mercury or Charles Schwab International.

- Build the receipt habit immediately. A Google Drive folder called "HSA Medical Receipts" that you add to after every foreign medical expense is the simplest system that works.

HSA Inside a Full Expat Financial Stack

The HSA doesn't live in isolation. For a US expat building a tax-efficient portfolio abroad, the contribution priority generally runs:

- 401(k) to employer match (free money first)

- HSA maximum (triple tax advantage)

- Roth or backdoor Roth IRA (if FEIE income permits)

- Taxable brokerage (unrestricted, but taxed on gains)

If you're using the FEIE to exclude foreign earned income — up to $126,500 in 2024 — note that FEIE-excluded income cannot fund a Roth or traditional IRA contribution. HSA contributions don't have this restriction if you have qualifying HDHP coverage. That's another edge case where the HSA wins for active FEIE users: it's the one tax-advantaged account that FEIE doesn't disqualify.

For expat health insurance strategy, the full comparison of international plans covers this in detail. The short version: SafetyWing Nomad Insurance ($40–$60/month for most ages) provides solid international coverage, but if maintaining HSA contribution eligibility matters to you, pair it with a qualifying US catastrophic plan.

Keep the Account. Build the Fund.

The HSA's biggest problem isn't its rules — those are more expat-friendly than most realize. The problem is that the account gets abandoned at departure because people assume moving abroad makes it irrelevant. It doesn't.

The account is portable. The tax advantage is permanent. The funds work globally. The only thing you need to do is not abandon it when you get on the plane.

Start with the basics: if your HSA is sitting at a legacy employer custodian charging fees and parked in a money market, move it to Fidelity today. Invest it in an index fund. Build the receipt folder. Come back to it at 65 — you'll be glad you did.

This article is for informational purposes only and does not constitute tax or financial advice. HSA rules are complex and individual circumstances vary. Consult a qualified expat tax professional before making contribution or withdrawal decisions while living abroad. Rules referenced are based on IRS guidance current as of early 2026.