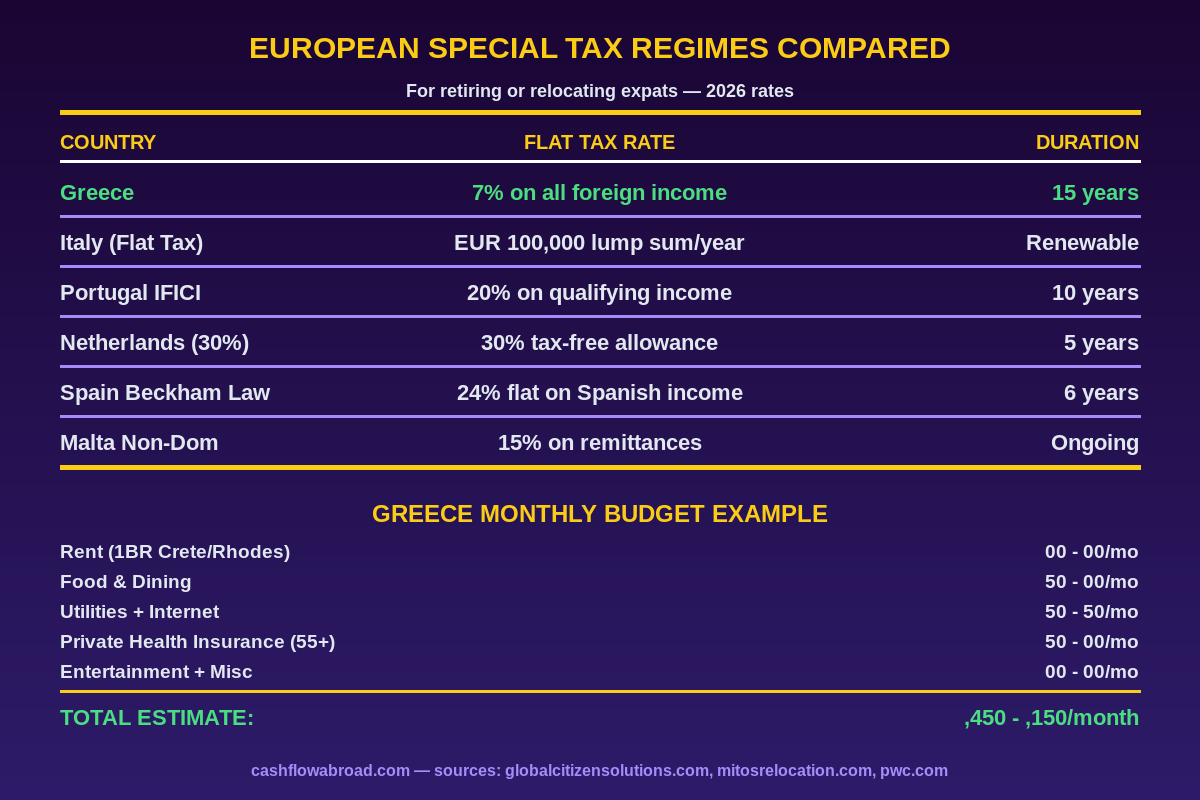

Somewhere between Italy's €100,000-per-year lump-sum tax deal and Portugal's now-defunct NHR scheme sits a regime almost nobody talks about: Greece's 7% flat tax on all foreign-sourced income, available for up to 15 years to anyone who relocates their tax residency to Greece. Seven percent. On dividends, pensions, rental income, capital gains — everything coming from outside Greece's borders.

For context: a US retiree collecting $80,000 in Social Security, pension, and investment income pays $5,600 to Greece under this regime. A comparable income in Germany faces a marginal rate above 40%. The math is blunt.

Greece launched this incentive in 2020 specifically to attract foreign retirees, and it's been quietly popular with Northern Europeans while most American expats haven't heard of it. That's partly because it has real limitations for US citizens — limitations this guide addresses directly rather than burying in fine print.

How Greece's 7% Flat Tax Actually Works

The regime lives in Article 5B of the Greek Income Tax Code. Once approved, you pay a flat 7% on all foreign-sourced income — pensions, dividends, interest, rental income from properties outside Greece, and capital gains from foreign assets. Greek-sourced income (if you have any) remains subject to normal progressive rates.

Three mechanics worth understanding before you get excited:

The minimum tax floor. Even if 7% of your income would be €800, you owe a minimum of €7,500 per year (plus €500 for each dependent). So the regime makes the most sense if your annual foreign income exceeds roughly €107,000 — below that, you're effectively paying a higher effective rate than 7%. For most retirees with $50,000–$90,000 in income, the floor is the actual number they're paying.

The irrevocable election. Once you're in, you can't retroactively switch back to standard Greek taxation and then return to the 7% regime later. You can exit voluntarily, but re-entry isn't allowed. This matters if your income structure changes significantly.

The 15-year ceiling. The regime is available for a maximum of 15 tax years from the date of approval. After that, you fall back into standard Greek tax brackets.

Who Qualifies

The requirements are stricter than they appear on most blog posts. You need to satisfy all four of these:

| Requirement | Details |

|---|---|

| Tax residency history | Must NOT have been a Greek tax resident in at least 5 of the past 6 years |

| Qualifying pension | Must receive a pension linked to prior employment — investment pensions, self-funded annuities, and IRA withdrawals generally don't qualify |

| Tax treaty country | Must be a tax resident of a country that has a Double Taxation Treaty with Greece (the US qualifies) |

| Physical presence | Must spend at least 183 days per year in Greece to establish tax residency |

That second requirement is the one that trips people up. If your "pension" is actually a 401(k) distribution, IRA withdrawal, or self-funded investment income — technically not an employment-linked pension — it may not qualify under the regime's definition. Greek tax authorities have been strict on this point. If your primary income source is investment withdrawals rather than a defined-benefit pension or Social Security, consult a Greek tax attorney before making any moves.

The US Citizen Problem (And How to Work Around It)

Here's the honest version that most "retire in Greece" articles skip: the 7% flat tax is significantly less powerful for US citizens than for Europeans, because Americans are taxed on worldwide income regardless of where they live.

You cannot escape US taxation by moving to Greece. What you can do is coordinate:

The Foreign Tax Credit (FTC) lets you claim Greek taxes paid as a dollar-for-dollar credit against your US tax liability. If you pay €5,600 to Greece, that amount (roughly $6,100) reduces your US tax bill. The net result: you pay the higher of the Greek rate (7%) or your US marginal rate — not both rates stacked.

For retirees in lower US brackets, this creates genuine savings. A married couple with $80,000 in combined pension and Social Security income likely faces a 12% effective US rate. After the FTC from Greece's 7%, they're paying roughly 5% extra to the US — total effective rate around 12%, same as staying in the US, but with the lifestyle upgrade of living in Crete.

The Foreign Earned Income Exclusion (FEIE) is largely irrelevant here — it covers earned income from work, not pension or investment income. Most retirees using the 7% regime will rely on the FTC, not the FEIE.

Note: The US and Greece do not have a comprehensive income tax treaty (the existing agreement is limited in scope), but they do have a Social Security Totalization Agreement that prevents double Social Security taxes. Pension and investment income flows through the FTC route. Consult an expat CPA familiar with both jurisdictions — this is the kind of dual-filing situation where DIY is not advisable.

Getting There: The FIP Visa

Greece doesn't have a "retirement visa" by name. What it has is the Financially Independent Person (FIP) Visa — a long-stay D-type visa for non-EU nationals who can demonstrate passive income without needing to work in Greece.

Income requirement: €3,500/month minimum (approximately $3,800 at current rates), plus 20% for a spouse and 15% per dependent child. A couple needs to show roughly €4,200/month in provable income. Sources can include pensions, Social Security, dividends, rental income, or investment distributions.

The FIP visa process:

- Apply at the Greek consulate in your home country (not possible after arrival as a tourist)

- Submit proof of income, health insurance, clean criminal record, and a Greek address (rental contract)

- Initial visa valid for 1 year; renews for 3-year periods

- After 5 years of legal residency, you can apply for permanent residency

- After 7 years, Greek citizenship becomes possible

Important: The FIP visa grants you residency. Once resident, you register with the Greek tax authority (AADE) and apply separately for the 7% flat tax regime. These are two distinct bureaucratic processes.

Applications for the 7% regime are accepted once per year, between January 1st and March 31st. Miss that window and you wait another year. Plan your move timeline accordingly.

What $1,800/Month Buys You in Greece

Greece runs 30–35% cheaper than the US and about 20% below Northern European averages, depending on location. The islands are pricier than the mainland, and Athens is pricier than smaller cities.

| Expense | Athens | Crete / Rhodes | Thessaloniki |

|---|---|---|---|

| 1BR apartment rent | €600–€900 | €450–€700 | €350–€550 |

| Groceries (couple) | €300–€400/mo | €250–€350/mo | €230–€320/mo |

| Dining out (meal) | €10–€18 | €8–€15 | €7–€13 |

| Public transport pass | €30/mo | Limited service | €30/mo |

| Utilities (avg apartment) | €150–€200/mo | €130–€180/mo | €120–€170/mo |

A couple living comfortably — nice apartment in Chania (Crete), eating out 3–4 times per week, taking occasional island ferry trips — realistically spends €1,800–€2,400/month (roughly $1,960–$2,600). That's a lifestyle that would cost $5,000+ in a US coastal city.

Best Cities for American Retirees in Greece

Chania, Crete. The consensus favorite for Anglophone expats. Venetian harbor, established expat infrastructure, direct flights to major European hubs, and a slower pace than Athens. Rents run €450–€700 for a one-bedroom. Mediterranean climate means mild winters, though summers hit 35°C (95°F).

Athens. Best for people who want urban conveniences, the full metro system, proximity to nightlife and culture. The northern suburbs (Kifisia, Glyfada) attract wealthier expats. More expensive than the islands but still cheaper than any major Western European capital.

Rhodes. Second most popular island after Crete, with a good hospital and year-round expat community. The medieval old town is UNESCO-listed. Warmer winters than Crete and more reliably sunny.

Thessaloniki. Greece's second-largest city, underrated by expats. Lower cost of living than Athens, vibrant food scene, cosmopolitan culture, and direct rail connections to Bulgaria and North Macedonia. Winters are colder than the islands.

Corfu. Popular with British expats for decades. Greener and wetter than most Greek islands, lower summer temperatures. Direct UK flights make it easy for retirees splitting time between countries.

Healthcare: What You Need to Know

Greece's public healthcare system (ESY) is accessible to legal residents who contribute to the EOPYY social insurance system. Non-EU retirees arriving via FIP visa who aren't working in Greece won't automatically have access to subsidized public healthcare — you'll need private insurance, at least until you establish social insurance contributions through residency.

Private health insurance for a 55-year-old in Greece runs €150–€200/month for comprehensive coverage. For a 65-year-old, expect €250–€350/month. Note that many providers won't issue new policies to applicants over 65, so sorting this before you move is essential.

A practical solution for the early years is international health insurance through providers like SafetyWing, which provides coverage across countries including Greece and satisfies FIP visa health insurance requirements. Once you're established as a resident and contributor, transitioning to local Greek private insurance becomes an option. For a full breakdown of how expat health coverage works, see our expat health insurance guide.

Greece also has high-quality private hospitals (Iaso, Hygeia in Athens) with English-speaking staff that rival anything in Western Europe at 30–50% lower cost.

Banking and Money Management

You'll need a Greek bank account once you're a resident. The major banks — Alpha Bank, Piraeus, Eurobank — all accept non-EU residents with a tax registration number (AFM) and proof of address. Opening takes 1–2 business days with the right documents.

For maintaining US financial infrastructure — brokerage accounts, credit cards, IRS correspondence — you'll want a virtual US mailbox that gives you a real street address in your preferred US state. This is critical for keeping accounts at US institutions that won't serve foreign-address clients, and for maintaining state domicile in a no-income-tax state like Florida or South Dakota. See the guide on how expats use virtual mailboxes to keep their US financial life intact.

For US-based investment accounts, Charles Schwab International is the standard recommendation for expats — they won't close your account when you move abroad, offer fee-free international ATM withdrawals worldwide, and their brokerage arm handles the PFIC-aware investing that expats need. More in the expat investor's playbook.

For transferring money from the US to your Greek bank account regularly, Remitly offers competitive USD→EUR rates.

How to Apply for the 7% Regime

The application timeline has hard deadlines. Here's the sequence:

- Establish Greek tax residency. Spend 183+ days in Greece during the tax year. Register your Greek address with the local municipality (Δήμος).

- Get your AFM (tax number). Register at the local AADE (tax authority) office with your passport, FIP visa, and proof of address.

- Submit the flat tax application. File between January 1st and March 31st of the year following the one in which you became a tax resident. Submit to the AADE's centralized processing center in Athens — not your local office. Include proof of pension income (official statement from the Social Security Administration, pension fund, or employer).

- Pay the lump sum. If approved, pay your flat 7% tax (minimum €7,500) by the last business day of July each year.

The election is reviewed annually, but once approved you remain in the regime until you exit voluntarily, the 15 years expire, or AADE determines you no longer qualify (e.g., you spend fewer than 183 days in Greece in a given year).

Working with a local Greek tax accountant (λογιστής) for the first filing is strongly recommended. Expect to pay €500–€1,500 for initial setup and application support.

The Four Catches Worth Knowing

1. Employment pensions only. If your retirement income comes primarily from IRA/401(k) withdrawals rather than a formal employment pension or Social Security, qualification is uncertain. Greek tax authorities have discretion here, and the law was written with traditional pensions in mind.

2. The minimum floor changes the math. At €7,500/year, the minimum tax only equals 7% if your annual foreign income exceeds €107,142. For someone living on $60,000/year, their effective Greek tax rate isn't 7% — it's 12.5% (€7,500 / €60,000). Still lower than most European alternatives, but worth calculating accurately before you move.

3. The 183-day rule is strict. You must actually live in Greece for more than half the year. Spending the summer abroad or wintering in Florida undermines your residency status and can invalidate the regime retroactively for that year. This is Greece's flat tax, not a paper arrangement.

4. The irrevocability cuts both ways. If Greece raises the rate or if your income changes in ways that make the regime less favorable, you're locked in for the election period. You can exit, but you can't re-enter.

Who This Is Actually For

The Greece 7% regime is strongest for:

- European retirees from high-tax countries (Germany, France, Netherlands) who would otherwise face 35–45% marginal rates — for them, the savings are dramatic

- US retirees with high incomes ($120,000+/year) where the FTC coordination becomes genuinely advantageous, especially combined with Greece's much lower cost of living

- US retirees with traditional defined-benefit pensions or Social Security who meet the employment-pension definition cleanly

- Anyone who genuinely wants to live in Greece — the Mediterranean lifestyle, EU residency pathway, and access to all of Europe make this attractive independent of the tax angle

It's weaker for US retirees with modest incomes who rely primarily on IRA withdrawals — the qualification risk plus the minimum tax floor make the benefit less clear. If Greece doesn't appeal geographically but you're drawn to the flat-tax-Europe idea, Bulgaria and Romania both offer 10% flat rates on all income with simpler qualification. Greece's 7% specifically for pensioners remains the most generous rate in the EU.

For the full landscape of expat tax options, the retirement abroad guide covers how Social Security stretches across dozens of countries with different tax treatments.

Bottom Line

Greece's 7% flat tax isn't a magic loophole for US citizens the way it is for Europeans — worldwide taxation means Americans still file with the IRS. But coordinated with the Foreign Tax Credit, it simplifies Greek tax obligations dramatically and keeps the effective rate reasonable while handing you a Mediterranean retirement at a fraction of what it costs in the US or Western Europe.

The barriers are real: the March 31st annual application deadline, the employment-pension requirement, the 183-day residency rule, and the minimum €7,500 floor. Work through those honestly, and for the right retiree — one with a government or corporate pension, comfortable income, and a genuine desire to live in Southern Europe — Greece is one of the most financially rational retirement destinations on the planet.

Disclaimer: This article is for informational purposes only and does not constitute tax or legal advice. US citizens living abroad have complex dual-filing obligations. Consult a qualified expat CPA and a licensed Greek tax advisor before making any residency or tax election decisions.