GILTI Tax: The IRS Rule That Taxes Profits You Never Touched

You moved abroad, incorporated a local company, and started building a business. You kept profits in the company to reinvest.

You moved abroad, incorporated a local company, and started building a business. You kept profits in the company to reinvest.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You moved abroad, incorporated a local company, and started building a business. You kept profits in the company to reinvest. You paid yourself nothing. Then your CPA told you the IRS was sending a tax bill for those profits anyway — profits sitting in a foreign bank account you hadn't touched.

This is not hypothetical. It happens to thousands of US expat business owners every year. The culprit: GILTI — Global Intangible Low-Taxed Income — a provision of the 2017 Tax Cuts and Jobs Act designed to prevent US multinationals from parking profits offshore. The problem is it catches solo entrepreneurs, freelancers, and small business owners who never meant to park anything anywhere. They just built a company abroad.

In 2026, the rules got a rebrand and a rate hike. Here is everything you need to know to avoid a surprise bill.

What Is GILTI — and Why Should Expats Care?

GILTI stands for Global Intangible Low-Taxed Income. Congress invented it in 2017 to tax US shareholders on foreign corporate profits that escape adequate taxation overseas. The theory was that tech giants were routing intellectual property income through low-tax jurisdictions to avoid US tax indefinitely. GILTI was the weapon to stop them.

The collateral damage: every American who owns a controlling stake in a foreign corporation — from a Bali consulting company to a Medellin software firm to a Dubai trading LLC.

The brutal core mechanic: you owe US tax on your foreign corporation's profits each year, whether you take a distribution or not. You can leave every dollar in the company. The IRS still wants its cut.

You are in GILTI territory if you meet all three criteria:

- You are a US citizen or resident (the "US shareholder" test)

- You own 10% or more of a foreign corporation (by vote or value)

- US shareholders together own more than 50% of that corporation — making it a Controlled Foreign Corporation (CFC)

If you are an American freelancer who formed a one-person company abroad, you likely own 100% of a CFC. GILTI almost certainly applies to you.

The 2026 Rebrand: GILTI Becomes NCTI

Starting January 1, 2026, GILTI was officially renamed Net CFC Tested Income (NCTI) under the One Big Beautiful Bill Act (OBBBA). The mechanics shifted, and for many expats, the changes are not in their favor.

Here is what changed:

QBAI Deduction Eliminated

Under the old GILTI rules, you could subtract a deemed 10% return on your company's tangible assets (Qualified Business Asset Investment, or QBAI) before calculating your taxable GILTI inclusion. If your company had $200,000 in equipment and furniture, you could shield $20,000 from the GILTI calculation. Starting 2026, that carve-out is gone. Every dollar of tested income is now potentially subject to NCTI. Service businesses — consulting, software, writing — that never had tangible assets feel no difference. Asset-heavy businesses now owe more.

Section 250 Deduction Reduced

The Section 250 deduction — available to individuals who make a Section 962 election (more on that below) — dropped from 50% to 40% starting in 2026. This raises the effective US tax rate on foreign business income from 10.5% (through 2025) to 12.6% (from 2026 forward).

Foreign Tax Credit Haircut Reduced

There is one piece of genuinely good news. The "haircut" on foreign tax credits available against NCTI dropped from 20% to 10%. Through 2025, only 80% of foreign taxes paid by your CFC were usable as credits against your GILTI bill. Starting 2026, 90% of those taxes apply. For expats operating in moderate-tax countries, this meaningfully reduces double taxation.

How GILTI/NCTI Is Actually Calculated

The math trips up even experienced accountants. Here is a simplified walkthrough.

Suppose you own a Colombian consulting company that generates $100,000 in net profit. Colombia's corporate tax rate is around 35%, so your company paid approximately $35,000 in Colombian corporate tax, leaving $65,000 in retained earnings.

Under GILTI with a Section 962 election:

- Tested income: $100,000

- QBAI deduction (through 2025): $0 (service business)

- GILTI inclusion: $100,000

- Section 250 deduction (50%): taxable GILTI = $50,000

- US corporate rate: 21% x $50,000 = $10,500 tentative tax

- Foreign tax credit (80% haircut applies): proportional share of Colombian tax likely offsets the entire $10,500

- Net GILTI bill: $0 (Colombia's 35% rate exceeds the 18.9% threshold)

Run the same business through a zero-tax jurisdiction instead:

- Tested income: $100,000

- GILTI inclusion: $100,000

- Section 250 deduction (50%): taxable = $50,000

- US corporate rate 21% x $50,000: $10,500

- Foreign tax credit: $0 (no foreign taxes paid)

- Net GILTI bill: $10,500

Starting 2026, the Section 250 deduction drops to 40%, producing a 12.6% effective rate. The same zero-tax scenario generates a $12,600 NCTI bill. Without the Section 962 election at all, individual rates up to 37% apply to the full $100,000 inclusion — a $37,000 US tax bill on profits you never received.

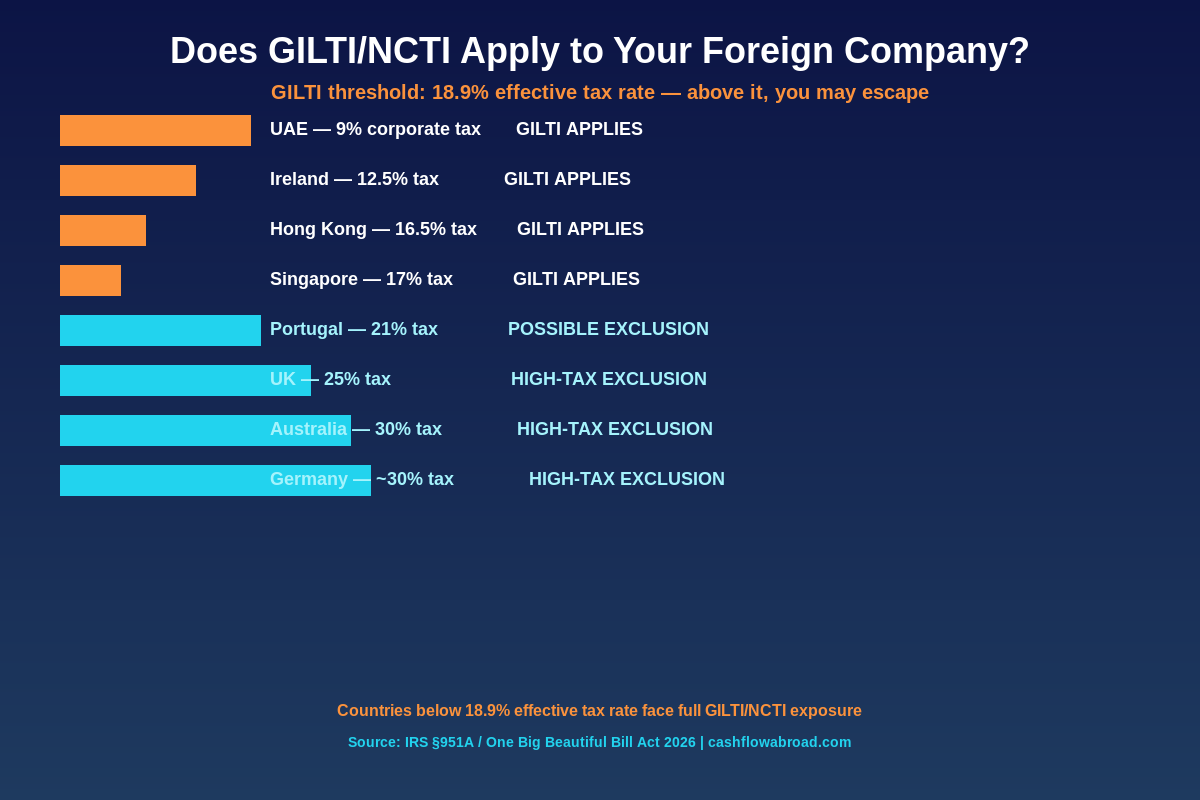

Which Countries Trigger GILTI — and Which Do Not

The escape hatch is the high-tax exclusion: if your foreign corporation pays an effective tax rate of at least 18.9% (90% of the 21% US corporate rate), you can exclude that income from GILTI/NCTI entirely. Note the keyword: effective rate, not statutory rate.

| Country | Corporate Tax Rate | GILTI/NCTI Status | Notes |

|---|---|---|---|

| UAE | 9% | Fully exposed | Below threshold; free zone carve-outs may not help |

| Ireland | 12.5% | Fully exposed | Below 18.9% threshold |

| Hong Kong | 16.5% | Fully exposed | Territorial system does not shield US shareholders |

| Singapore | 17% | Fully exposed | Just below threshold; credits partially offset |

| Georgia | 15% | Fully exposed | Popular nomad hub; GILTI applies at full rate |

| Portugal | 21% | Possible exclusion | Just above statutory threshold; verify effective rate |

| UK | 25% | High-tax exclusion | Usually qualifies comfortably |

| France | 25% | High-tax exclusion | Usually qualifies |

| Australia | 30% | High-tax exclusion | Qualifies with room to spare |

| Germany | ~30% | High-tax exclusion | Combined rate clears threshold easily |

| Colombia | 35% | High-tax exclusion | Exceeds threshold; FTCs typically offset residual |

The practical takeaway: building your company in a zero-tax or very low-tax jurisdiction does not shield your US tax liability. It redirects it entirely to the IRS, with no foreign tax credits to cushion the blow. Many expats discover this only after their first Form 5471 is due.

Three Strategies to Reduce GILTI/NCTI Exposure

Strategy 1: High-Tax Exclusion

If your foreign company's effective tax rate exceeds 18.9%, you can exclude its income from NCTI entirely. This is the cleanest solution — no US tax, no credits to track, no elections to calculate. The catch: you must elect this exclusion annually, and the associated foreign taxes cannot be used to offset other US income. If your only US-taxable income comes from the CFC, the exclusion almost always makes sense. If you have complex cross-border credit situations, the math can cut the other way.

Strategy 2: Section 962 Election

A Section 962 election lets an individual US shareholder elect to be taxed on CFC income at corporate rates rather than individual rates. This unlocks the 40% Section 250 deduction (as of 2026), bringing the effective rate to 12.6%, plus 90% usable foreign tax credits. The downside: a second layer of tax when you actually take distributions. When dividends come out of a 962-elected company, they do not qualify as qualified dividends — they are taxed as ordinary income, reduced by previously-taxed earnings credit. A CPA with hands-on Form 8992 experience is not optional here.

Strategy 3: Operate Through a Higher-Tax Entity

Some expats restructure operations to run through an entity in a country with a statutory rate above 18.9% — even if they physically work elsewhere. This requires real substance: employees, office space, actual business operations in that country. Not a mailbox. Not a shelf company. The IRS has sharpened its substance requirements significantly. If your "UK company" has no UK employees and no UK economic activity, the IRS will look through it.

A fourth path worth considering: if you operate as a sole proprietor rather than through a foreign corporation, GILTI does not apply. You will owe US self-employment tax (15.3%) plus income tax on earnings above the Foreign Earned Income Exclusion limit ($130,000 for 2025). For many expat business owners, comparing the corporate structure versus sole proprietorship tax profiles is where tens of thousands of dollars per year are won or lost. The FEIE guide explains the exclusion mechanics in detail.

GILTI vs. Subpart F: Not the Same Thing

These two provisions are constantly confused and often apply simultaneously. Subpart F income — enacted in 1962 — targets passive income earned by CFCs: dividends, interest, rents, royalties, and certain sales income that could be shifted offshore easily. GILTI targets active business income from intangibles. Both provisions can apply to the same company in the same year.

| Feature | Subpart F | GILTI/NCTI |

|---|---|---|

| Income targeted | Passive (interest, dividends, rents) | Active business income from services/intangibles |

| Year introduced | 1962 | 2017 (TCJA) |

| Section 250 deduction available | No | Yes (with 962 election) |

| High-tax exclusion | Yes (different threshold) | Yes (18.9% threshold) |

| Who it hits hardest | Holding companies, passive investment structures | Consultants, SaaS founders, active service businesses |

Most solo expat business owners encounter GILTI far more than Subpart F. But if your foreign company holds investments, earns interest on cash balances, or collects rent, Subpart F can trigger in the same year — and the two calculations do not offset each other automatically.

The Forms You Cannot Skip

Owning a CFC comes with a compliance obligation that goes well beyond a standard tax return. Missing these forms does not just mean you forgot to report something — it means automatic penalties can stack up before the IRS even looks at whether you owe underlying tax.

Form 5471: Information Return of Foreign Corporation

This is the central disclosure for any US person with significant ownership in a foreign corporation. It includes income statements, balance sheets, officer and director lists, and detailed records of transactions between you and the company. The penalty for failing to file Form 5471 on time: $10,000 per form per year. Additional $10,000 penalties (up to $50,000) accumulate if filing remains delinquent after IRS notice. In severe cases, total Form 5471 penalties reach $60,000 for a single missed year.

Form 8992: GILTI/NCTI Calculation

This is where you calculate your GILTI or NCTI inclusion. It aggregates tested income and tested losses across all your CFCs, applies any applicable deductions, and flows the result to your Form 1040.

Form 8993: Section 250 Deduction

If you have made a Section 962 election, Form 8993 calculates the Section 250 deduction that reduces your effective NCTI rate to 12.6%.

Form 1118: Foreign Tax Credits

This is the corporate foreign tax credit form — required if you have made the 962 election and want to apply taxes your CFC paid abroad against your US NCTI liability.

The realistic cost of getting this right: specialized international tax preparers typically charge $2,500–$6,000 for a return involving one CFC with GILTI exposure. Add multiple CFCs, intercompany loans, or real property, and the fee climbs. This is not a task for a generalist domestic CPA. Ask directly whether your preparer has filed Form 5471 before — most have not. The expat tax service rankings can help you vet your options.

Banking Infrastructure for CFC Owners

Running a CFC means managing money in at least two jurisdictions. A few tools that simplify the US side:

Mercury provides FDIC-insured US business banking with no monthly fees and strong wire capabilities. It is well-suited for expat founders who need a US-based account for clients that insist on paying domestic accounts, while the company itself operates abroad.

Charles Schwab International is the standard for expat personal banking — no ATM fees worldwide, no foreign transaction fees, and a brokerage that does not close accounts when you move abroad. When your CFC distributes profits, you need somewhere to put them that does not penalize you for living outside the US.

Maintaining a Traveling Mailbox — a real US street address in any of 50+ cities, with mail scanning and check deposit — keeps your IRS correspondence, state filings, and banking address consistent. When the IRS sends a notice about your CFC filing, you need to actually receive it. At $15/month, it is cheap insurance. There is a full breakdown in the virtual mailbox guide for expats.

A Note on Crypto Operations Through CFCs

A growing number of expats structure crypto trading or DeFi operations through foreign companies — often in the UAE, Georgia, or El Salvador. These structures do not escape GILTI. If the company earns trading profits, yield farming returns, or staking rewards and you own 10%+ of a CFC, you are in the same NCTI framework as any other business. Crypto income held in a CFC is not tax-deferred; it flows through to your US return annually at the rate your elections and country's local taxes dictate. For the full picture on crypto across borders, see the US expat crypto tax guide.

Five Mistakes That Create Surprise GILTI Bills

- Assuming your local company is not a CFC. Solo expat founders who incorporated locally almost universally own a CFC. The structure does not have to be elaborate to qualify — a one-person consulting LLC in Tbilisi counts.

- Leaving profits in the company and assuming deferral is free. It is not. GILTI/NCTI taxes undistributed profits annually. Deferred does not mean excluded.

- Operating through a zero-tax jurisdiction without a Section 962 election. Without the election, individual income rates up to 37% apply to the full GILTI inclusion. The Section 250 deduction that drops the rate to 12.6% is only accessible after you make the election.

- Using a domestic CPA who does not know Form 5471. Many US CPAs have never filed one. The penalties for a botched or missing Form 5471 are automatic and can exceed the underlying tax.

- Ignoring prior-year exposure. If you have owned a CFC for multiple years and never filed, you have cumulative penalty exposure and unreported income. Voluntary disclosure programs exist — proactive remediation costs far less than IRS discovery.

The IRS Is Not Flying Blind

It is worth noting that the window for undiscovered non-compliance is narrowing fast. FATCA requires foreign financial institutions to report US account holders to the IRS. CARF — the Crypto-Asset Reporting Framework — extends similar reporting to crypto exchanges. The OECD's Common Reporting Standard shares financial data between 100+ countries. The IRS now receives more data on offshore accounts than it can process, which is precisely why its audit algorithms have grown more sophisticated at flagging anomalies. Operating a foreign company and filing a clean US return with no CFC disclosure is a pattern that stands out. The End of Expat Invisibility guide covers the data-sharing landscape in detail.

Conclusion

GILTI/NCTI is what happens when the US government decided it could no longer tolerate Americans building profitable foreign businesses and letting that profit accumulate tax-free offshore. The law is blunt: own 10%+ of a foreign corporation with other US shareholders, and you owe US tax on its annual profits whether you touched them or not.

For expats operating in high-tax countries — Germany, UK, Australia, France — the math often washes out via the high-tax exclusion or foreign tax credits. For expats in zero-tax or low-tax jurisdictions — UAE, Ireland, Singapore, Georgia — GILTI/NCTI is a real, annual, material liability that needs active management via the right elections, the right structure, and an accountant who actually knows what Form 5471 is.

Understand your CFC status. Know your effective tax rate. Make the right elections. File the right forms. The cost of getting this right is measured in accountant fees. The cost of getting it wrong is measured differently.

Financial Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. GILTI, NCTI, Subpart F, and CFC rules are highly fact-specific and complex. Tax laws change frequently. Consult a qualified international tax professional before making any decisions regarding your foreign business structure, CFC elections, or US tax filings. Prior results do not guarantee similar outcomes.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 13, 2026

Expat Tax & FinanceJune 13, 2026

WEP and GPO Repealed: Expats With Foreign Pensions Win

WEP and GPO ended in January 2025, giving expats with foreign pensions their full SS benefits. Average retroactive payout: $6,710. Here is the tax

Expat Tax & FinanceJune 13, 2026

Expat Tax & FinanceJune 13, 2026

Section 121 Exclusion: Selling Your US Home as an Expat

Move abroad and a 3-year clock starts on your $250K–$500K Section 121 exclusion. Learn the deadline, depreciation recapture, and how not to lose it.

Expat Tax & FinanceJune 12, 2026

Expat Tax & FinanceJune 12, 2026

FBAR: The $10,000 Rule Every US Expat Must Know

Every US expat with over $10,000 across foreign accounts must file FinCEN Form 114. Learn FBAR rules, deadlines, penalties, and how to catch up.