Germany for US Expats: Taxes, Visas & the €2,000/Month Life

Germany charges income tax at rates up to 45%. That's not a loophole. Processing through a German consulate takes 4–12 weeks.

Germany charges income tax at rates up to 45%. That's not a loophole. Processing through a German consulate takes 4–12 weeks.

Germany charges income tax at rates up to 45%. Yet most American expats earning a typical European salary there pay a lower combined tax bill — German plus US — than they did filing as a single filer in New York or California. That's not a loophole. That's what the US-Germany tax treaty actually does when you use the Foreign Tax Credit correctly, and most people who move there never bother to read it.

An estimated 300,000+ US citizens live in Germany, making it the most popular EU destination for American expats. The appeal is obvious once you're on the ground: world-class public infrastructure, universal healthcare, €63/month for unlimited train travel across the entire country, and one of the most powerful passports on earth once you naturalize. The downsides are equally real — Munich rents rival London, the bureaucracy runs on fax machines and office hours that end at 4pm, and your German language ability will be tested in ways apps never prepared you for.

Here's the complete picture: visas, taxes, costs, healthcare, banking — everything you need before booking a one-way ticket.

Your Path In: Germany's Visa Menu for Americans

US citizens can enter Germany without a visa for up to 90 days under the Schengen Agreement. After that, four realistic long-term options exist depending on your situation:

The Chancenkarte (Opportunity Card / Job Seeker Visa)

Germany's revamped job seeker visa — now called the Chancenkarte — lets you live in Germany for up to six months while searching for work, with no job offer required upfront. Eligibility requirements: a recognized degree or equivalent vocational qualification, proof of financial self-sufficiency (roughly €1,027–€1,091 per month for the visa duration), and valid health insurance. Processing through a German consulate takes 4–12 weeks. Americans can apply through consulates in eight US cities: Washington DC, New York, Chicago, Los Angeles, Houston, Atlanta, Boston, and San Francisco. This is the most accessible entry path if you're job-hunting remotely or want to scope out the market before committing.

The EU Blue Card

Germany's flagship long-term work visa for skilled non-EU nationals. As of 2026, the salary thresholds are:

- General occupations: €50,700 gross/year minimum with a confirmed job offer

- Shortage occupations (IT, engineering, healthcare, science): reduced to €45,934/year

- Recent graduates (degree within last 3 years): also qualify at the €45,934 threshold

- IT specialists with 3+ years of experience in the past 7 years can qualify without a university degree

The major advantage: Blue Card holders can apply for permanent residency after just 33 months, dropping to 21 months with demonstrated B1 German language proficiency. That's one of the fastest PR pathways in the EU. Once you have German permanent residency, you can work and live across all 27 EU member states.

Freelancer / Self-Employment Visa

If you're running a US-based remote business or consulting practice, the Freiberufler visa is your route. Germany hasn't launched a formal digital nomad visa, but this fills the gap. Requirements: a viable business plan, existing clients, demonstrated income (typically €2,000+/month), and health insurance. The critical distinction to nail upfront: Germany treats Freiberufler (professionals in creative, consulting, or technical fields) differently from Gewerbetreibende (trade business operators). Getting this classification wrong creates tax headaches that take years to unwind.

Family Reunion Visa

Spouses and dependent family members of German citizens or residents with valid permits can join via family reunification. Spouses of EU Blue Card holders receive expedited processing and work authorization upon arrival.

How Germany Taxes You: The Steuerklassen System

German income tax is progressive, kicking in above the Grundfreibetrag (basic tax-free allowance). For 2026, that allowance is €12,348 per year — income below this is tax-free entirely.

| Taxable Income (Annual) | Marginal Rate |

|---|---|

| Up to €12,348 | 0% (tax-free) |

| €12,349 – €68,430 | 14% → 42% (progressive) |

| €68,431 – €277,825 | 42% (flat) |

| Above €277,826 | 45% ("Reichensteuer") |

On top of income tax, Germany historically charged a Solidaritätszuschlag (solidarity surcharge) of 5.5% of your tax bill — a holdover from German reunification financing. Since 2021, it's been abolished for roughly 90% of taxpayers. In 2026, you only hit it if your annual income tax liability exceeds €20,350 as a single filer. For most Blue Card earners around the €50,000–€65,000 mark, the Soli is effectively gone.

Every employee is assigned a Steuerklasse (tax class) by their local Finanzamt. Single expats without dependents default to Class I. The Steuerklasse determines monthly paycheck withholding, not your final annual liability — you file a return and reconcile, and most expats actually receive a refund since they can deduct moving costs, professional training, German language classes, and home office expenses.

One trip wire specific to expats: even if your US income is tax-exempt in Germany under the treaty, Germany still counts it when calculating your marginal rate — a rule called Progressionsvorbehalt (progression reservation). It won't add German tax on that income, but it can push your German salary income into a higher bracket than expected. This surprises people every year.

The US Side: FEIE, Foreign Tax Credit, and the Treaty

The IRS taxes US citizens on worldwide income regardless of residency. Germany is no exception. But with the Foreign Tax Credit and the US-Germany tax treaty, double taxation is largely solvable — if you structure correctly before you move.

Foreign Tax Credit (FTC) vs. FEIE — and why most Germany expats should choose FTC: Germany's marginal rates (up to 45%) exceed the US top rate (37%). For employees earning above roughly €65,000, the German taxes paid will often exceed the US taxes that would have been owed — generating a credit that eliminates US liability entirely, with carryforward for unused amounts. The Foreign Earned Income Exclusion for 2025 (filed in 2026) excludes up to $130,000 of earned income from US taxation, but it cuts you off from Roth IRA contributions, blocks you from claiming FTC on excluded income, and can actually increase your US tax bill on non-excluded income by eliminating the low-bracket benefit. For higher earners in Germany, FEIE is often the worse choice — and once you elect it, you're locked in for five years without IRS permission to switch. See our FEIE vs FTC breakdown before deciding.

The US-Germany Tax Treaty covers employment income, pensions, dividends, royalties, and capital gains. The practical result for most W-2-equivalent employees: you pay German tax rates, file a US return showing the Foreign Tax Credit, and owe the IRS nothing additional. But you still file. FBAR and FATCA obligations kick in the moment your German bank accounts cross $10,000 aggregate at any point during the year.

Entrepreneurs operating a German GmbH face additional complexity post-2025. The OBBBA legislation renamed GILTI to Net CFC Tested Income (NCTI) and raised the effective minimum rate to 12.6% for 2026. If you're running a business through a German entity as a US citizen, hire a CPA who handles both German Steuerberater work and US international tax — the interaction between German corporate law and US pass-through rules is genuinely complicated.

Cost of Living: The Honest City-by-City Breakdown

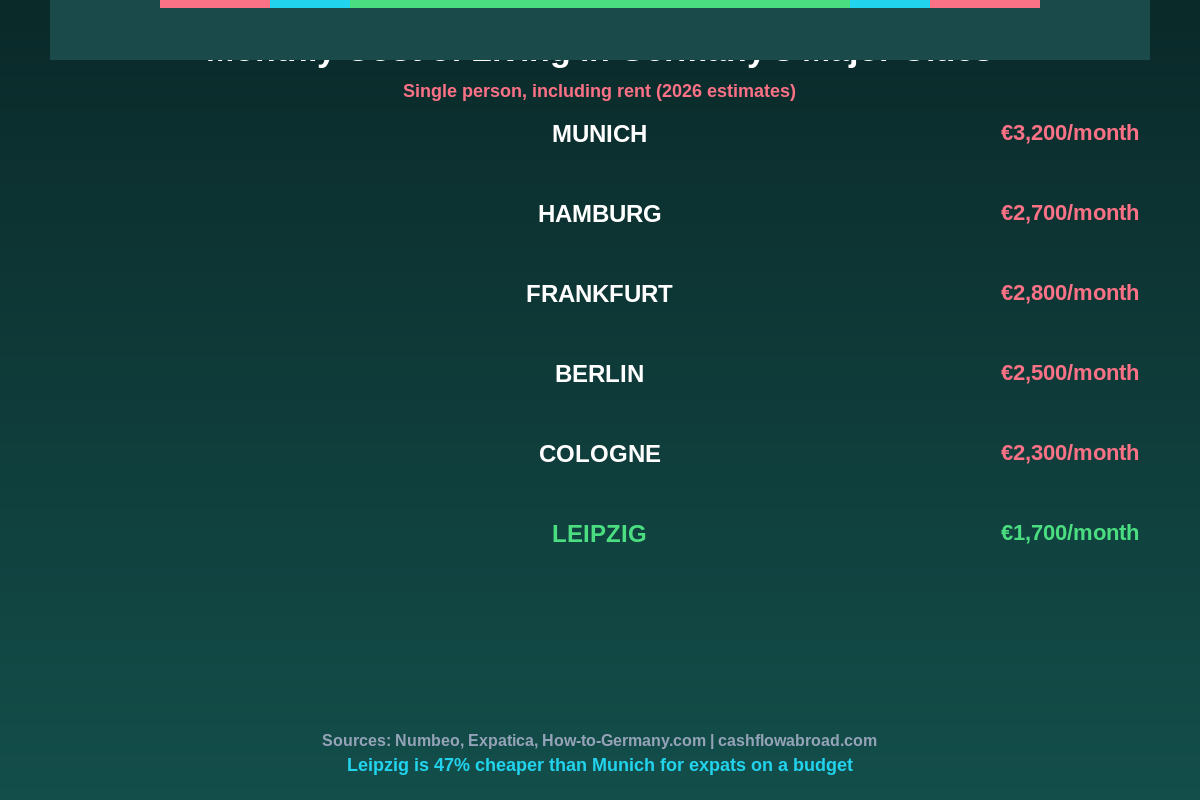

Germany's cost of living varies more dramatically than most people expect. Munich is now one of the most expensive cities in continental Europe. Leipzig and Dresden remain genuinely affordable. The €2,000/month life is real — just not in the same zip code as the Allianz Arena.

| City | 1BR Rent (City Centre) | Utilities | Transport | Groceries + Dining | Monthly Total |

|---|---|---|---|---|---|

| Munich | €1,500 | €350 | €63 | €900 | ~€3,200 |

| Frankfurt | €1,350 | €300 | €63 | €800 | ~€2,800 |

| Hamburg | €1,250 | €280 | €63 | €750 | ~€2,700 |

| Berlin | €1,200 | €280 | €63 | €700 | ~€2,500 |

| Cologne / Düsseldorf | €1,050 | €250 | €63 | €650 | ~€2,300 |

| Leipzig / Dresden | €750 | €200 | €63 | €550 | ~€1,700 |

The Deutschlandticket at €63/month deserves its own mention. It gives unlimited access to all local and regional trains, trams, buses, and metros across the entire country — any city, any day. It launched at €49 in 2023, rose to €58 in 2025, and hit €63 in January 2026. For most urban expats, it eliminates the car entirely. If you're moving from a US city where car ownership costs $700–$1,000/month, this alone is a massive lifestyle upgrade.

Housing is the main lever. Munich's vacancy rate hovers near zero — rents have risen over 40% in the past decade and show no signs of cooling. Berlin closed the gap on affordability fast; it's no longer the cheap capital. For expats whose employer doesn't require Munich or Frankfurt, Leipzig and Dresden offer comparable quality of life at roughly half the housing cost, with growing tech and creative sectors attracting serious talent.

What Daily Life Actually Looks Like

Germany rewards patience and punishes improvisation. Registering your address at the local Bürgeramt — the Anmeldung — is mandatory within two weeks of arrival and is a prerequisite for nearly everything else: bank accounts, phone contracts, tax registration, health insurance enrollment. In major cities, appointment slots fill weeks out. Book yours before you board the plane.

Stores close on Sundays. Banks close at 4pm. Bureaucracy runs on physical forms and in-person visits. These aren't generalizations — they're Tuesday. On the other side of that ledger: trains run on time, streets are clean, parks are everywhere, and Germany's 28–30 average vacation days per year aren't theoretical. People actually take them.

The language barrier is real but navigable. Most major cities have substantial English-speaking professional communities, and the tech sector in Berlin, Munich, and Hamburg operates largely in English. That said, your Anmeldung appointment, insurance documents, and tax notices will arrive in German. Learning at least functional German is not optional if you plan to stay long-term.

Healthcare: Public vs. Private Insurance

Germany's healthcare system runs two parallel tracks. Employees earning below the annual income threshold (approximately €73,800 in 2026) are enrolled in statutory health insurance (gesetzliche Krankenversicherung, GKV). The premium is 14.6% of gross salary split evenly between employee and employer — you personally pay about 7.3% of gross. That covers doctor visits, hospitalization, specialist referrals, and prescriptions with small copays. No deductibles, no network restrictions.

Employees above the threshold can opt for private health insurance (private Krankenversicherung, PKV). Private plans typically mean shorter wait times, private hospital rooms, and direct specialist access. Premiums vary substantially by age and health: a healthy 30-year-old pays roughly €300–€500/month, but costs rise sharply after 50 and are difficult to abandon once you've switched.

Arrivals on freelancer or Job Seeker visas must secure their own insurance from day one. SafetyWing works as a short-term bridge while you're establishing residency, though you'll need to transition to a German-approved plan within a few months. For a full comparison of global expat health plans, see our expat health insurance guide.

Banking and Money for American Expats in Germany

Opening a German bank account requires your Anmeldung certificate in hand. N26 and Deutsche Bank both offer English-language onboarding. Commerzbank and Sparkasse are more accessible in smaller cities but typically require German documentation.

For your US-side banking, Charles Schwab's international brokerage account reimburses all ATM fees worldwide and carries no foreign transaction fees — it's the standard recommendation for expats who want to keep a US-based account that works at any ATM in Germany or anywhere else. If you're running a US business remotely from Germany, Mercury handles USD business banking with no fees and clean API access for remote operations.

Maintaining a US mailing address is essential for your US banking relationships, IRS correspondence, and brokerage accounts. A virtual mailbox like Traveling Mailbox — real US street address in 50+ cities, mail scanning, check deposits, starting at $15/month — is the cleanest solution. Our virtual mailbox guide for expats covers what to look for in detail.

For sending money between Germany and the US, Remitly offers competitive EUR/USD exchange rates with transparent fees. For regular monthly transfers, it typically beats international wire fees.

FBAR compliance is non-negotiable: if your German accounts cross $10,000 aggregate at any point in the year, you file FinCEN 114. The deadline is April 15 with an automatic October 15 extension. Non-willful violations carry penalties up to $10,000 per account per year.

Who Should Actually Move to Germany

Germany makes the most sense for:

- Tech, engineering, and healthcare workers — the Blue Card salary threshold of €45,934 for shortage occupations is achievable at mid-level, and permanent residency in under 3 years is real

- Remote workers on dollar-denominated contracts — you can earn in USD, live on EUR, and let the exchange rate work in your favor in lower-cost German cities

- Expats who want an EU base with maximum mobility — German PR opens doors across 27 EU countries; German citizenship (achievable in as little as 5 years with strong integration) produces one of the world's most powerful passports

- Families — Kindergeld (child allowance) pays €255/month per child; state childcare is subsidized; public schools are free and academically rigorous

Germany is harder to justify if tax minimization is the primary goal. The high marginal rates, combined with ongoing US filing obligations, mean a high-earning single American can face a real aggregate burden. If you want dramatic tax reduction, lower-tax jurisdictions in Southeast Asia and Latin America deliver more. Germany is a lifestyle and career investment, not a tax play. Those who move there for quality of life and professional opportunity tend to stay. Those who move for tax optimization tend to move again quickly.

The Bottom Line

Germany is Europe's most stable economy, with infrastructure and public services that make most of the world look careless by comparison. For Americans who want the full European experience — serious career, family stability, and eventually a powerful passport — it delivers at a level few countries match. The tax picture is manageable with proper structuring: the Foreign Tax Credit eliminates most US double-taxation, and Germany's rates are high but not punitive at moderate income levels. The visa pathways — especially the revamped Chancenkarte and the Blue Card — are more accessible than most Americans realize.

Execute the basics correctly: get your Anmeldung within two weeks, lock in your FEIE vs. FTC decision before you move (it's a five-year commitment), enroll in health insurance immediately, and open a US-based banking setup that doesn't close your accounts when you relocate. After that, Germany will run itself reasonably well — on its own schedule, at its own pace, in its own language.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and vary based on individual circumstances. Consult a qualified CPA or tax attorney experienced in both US and German tax law before making decisions about residency, investment accounts, or tax strategy.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.