France for US Expats: Taxes, Visas & the €1,800/Month Life

Most Americans who dream of living in Europe fixate on Portugal or Spain. That's less than a shared apartment in a mid-tier US city.

Most Americans who dream of living in Europe fixate on Portugal or Spain. That's less than a shared apartment in a mid-tier US city.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most Americans who dream of living in Europe fixate on Portugal or Spain. France is the obvious choice they dismiss as "too expensive" — and that assumption is costing them a lifestyle upgrade they could actually afford. Outside Paris, a single American can live comfortably in France for €1,500–€1,800 per month. That's less than a shared apartment in a mid-tier US city.

There are roughly 150,000 registered American citizens living in France, making it one of the largest US expat communities in Europe. The actual number, including those who never registered with the embassy, is likely double that. They're not all hedge fund managers. Many are remote workers, retirees, freelancers, and online entrepreneurs who ran the numbers and moved.

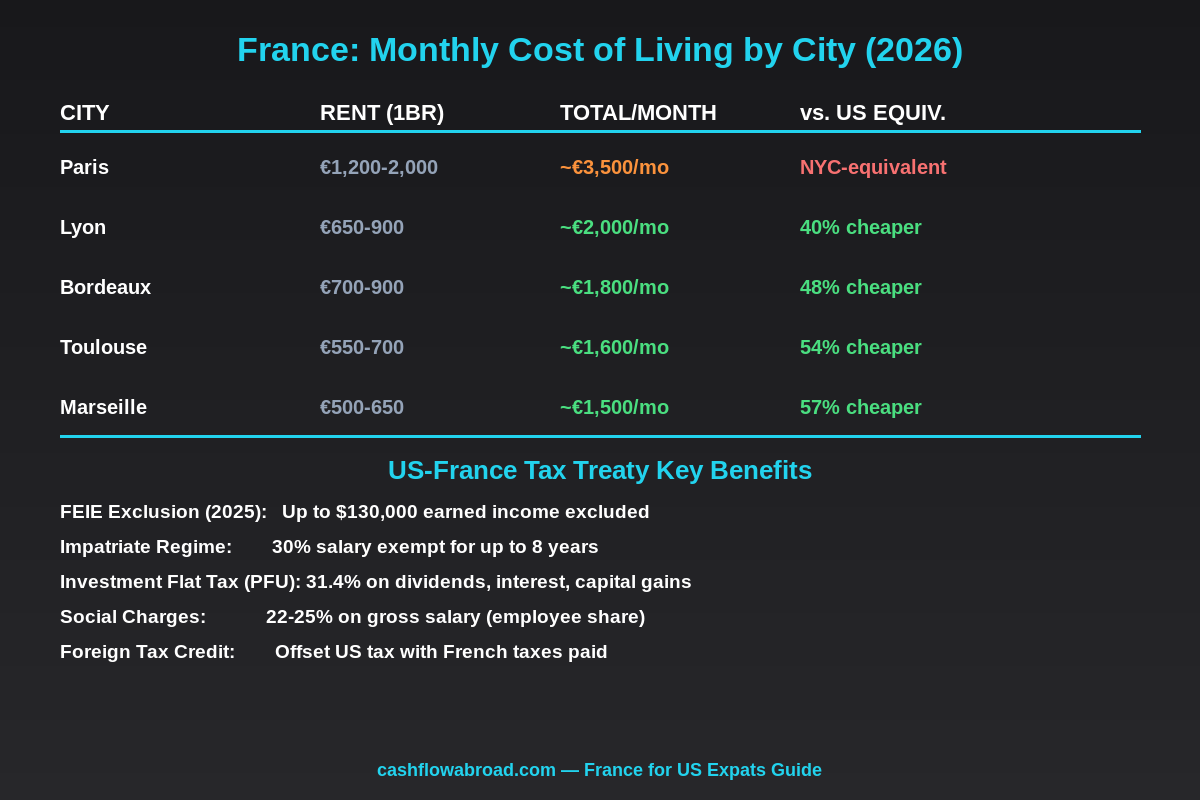

France has its complexities — the tax system is layered, the visa options are limited for remote workers, and the bureaucracy is legendarily slow. But the US-France tax treaty is one of the most comprehensive bilateral tax agreements the US has ever signed, and France's "Impatriate Regime" offers a tax break that few Americans even know exists.

Here's what it actually costs and what the IRS expects from you.

Visa Options for Americans in 2026

France does not have a dedicated digital nomad visa. That gap matters. Since June 2025, France has explicitly prohibited remote work on a visitor visa — meaning you can't live there for 90 days and work on your laptop for a US employer without legal exposure.

Your real options as an American:

Profession Libérale Visa

This is the primary route for freelancers and self-employed Americans. It's valid for one year, renewable up to four years, and eventually leads to a 10-year carte de résident. Requirements: you must prove annual income of at least €21,876 (the French minimum wage equivalent), have valid health insurance, and submit a business plan or client contracts. Processing takes 6–10 weeks through a French consulate in the US.

The downside: you become a French tax resident, which means France taxes your worldwide income. But if your income is over ~€50,000, the Foreign Tax Credit usually wipes out most US tax liability — you end up paying French rates, not double taxes.

Talent Passport (Passeport Talent)

France's version of a high-skilled worker visa. Requires a gross annual salary of at least €34,650 and employment by a French company or qualifying research institution. Valid up to 4 years. This is the path if you're relocating for a French employer — and critically, if your employer recruited you from abroad, you qualify for the Impatriate Regime (more on that below).

Long-Stay Visitor Visa (Visa de Long Séjour — Visiteur)

For retirees or people with passive income. Requires proof of sufficient funds (roughly €2,000+/month), no employment or remote work in France, and private health insurance. Since June 2025, this visa explicitly bans professional activity of any kind — including remote work for foreign clients. If you're a passive income investor, retiree, or living off savings or investments, this is your option.

Starting in 2026, visitor visa holders must pay a €300–€600 annual contribution fee before accessing the public healthcare system (PUMA). This is a new requirement passed by the French National Assembly in December 2025.

The French Tax System: What You Actually Pay

France's income tax is progressive and applied to household income, not individual income — a concept called the quotient familial. A married couple with two children divides their joint income by a household divisor before applying tax brackets, which meaningfully reduces the effective rate for families.

2026 Income Tax Brackets

| Income Band | Tax Rate |

|---|---|

| Up to €11,497 | 0% |

| €11,497 – €29,315 | 11% |

| €29,315 – €83,823 | 30% |

| €83,823 – €180,294 | 41% |

| Above €180,294 | 45% |

| Above €250K (single) / €500K (couple) | +3% surtax |

The headline rates look alarming — 45% at the top. But those brackets don't tell the full story. The real burden includes social charges stacked on top.

Social Charges (Cotisations Sociales)

Employee social charges in France typically run 22–25% of gross salary. The two main contributions most expats encounter are the CSG (Contribution Sociale Généralisée) at 9.2% and the CRDS at 0.5%, applied to 98.25% of gross. The good news: 6.8% of the 9.2% CSG is tax-deductible, reducing your income tax base slightly.

If you're self-employed under the auto-entrepreneur regime, social charges run 22–24% of revenue depending on activity type. These fund French healthcare, pensions, and unemployment — so you're buying into a system that pays out in services, not just sending money to a black hole.

Investment Income: The Flat Tax (PFU)

Dividends, interest, and capital gains on securities face the Prélèvement Forfaitaire Unique — raised to 31.4% in 2026. Applied at source for most French financial institutions. As a US citizen, you can claim the Foreign Tax Credit for PFU payments against your US liability.

US Tax Obligations: What the IRS Still Wants

Living in France doesn't end your US filing obligations. US citizens owe tax on worldwide income regardless of where they live. Two tools reduce — and often eliminate — what you actually pay:

Foreign Earned Income Exclusion (FEIE)

For the 2025 tax year, the FEIE lets you exclude up to $130,000 of foreign earned income if you meet the bona fide residence or physical presence test. Most Americans legally resident in France qualify. Critical limitations: FEIE only covers earned income (wages, freelance). Passive income, dividends, and capital gains don't qualify. And if you claim FEIE, you cannot contribute to a Roth IRA unless your earned income exceeds the exclusion amount.

Foreign Tax Credit (FTC)

For most Americans in France earning above $130K, or with meaningful investment income, the FTC is more powerful. Since France's effective tax rates generally exceed US rates, the FTC can offset your entire US liability on French-source income. Excess credits carry forward three years.

Most US expats in France use the FTC rather than FEIE — France taxes high enough that there's typically nothing left to pay the US on top of it.

FBAR (FinCEN 114) is still required if foreign accounts exceed $10,000 at any point. Form 8938 kicks in at $200,000 in foreign financial assets for those living abroad. These are reporting obligations — not taxes — but the penalties for missing them start at $10,000 per violation. Full breakdown in the US Expat Banking & Taxes guide.

The Impatriate Regime: France's Best-Kept Expat Secret

If you're hired by a French employer or transferred to a French subsidiary from abroad, you may qualify for France's Impatriate Regime — a tax exemption almost nobody outside of multinational finance talks about.

Under this regime, 30% of your gross salary is exempt from French income tax for up to 8 years. To qualify: you must have been recruited from outside France, not been a French tax resident in the prior 5 years, and be working for a French entity. The impatriate bonus (any additional compensation tied to your relocation) is also fully exempt.

The math: on a €90,000 gross salary, only €63,000 is subject to French income tax. That cuts your French tax bill by roughly €8,100 per year at the 30% bracket — €64,800 saved over the full 8-year term. Stack the Foreign Tax Credit on top, and many impatriates end up paying less in total tax than they would have back in the US.

France aggressively promoted this regime post-Brexit to attract financial services and tech talent from London, and Americans transferring into French roles are fully eligible.

Healthcare in France as an American

France's public healthcare (PUMA) covers everyone legally residing in France for more than 3 months. After enrollment, you receive a Carte Vitale — a health card used at every doctor's office, hospital, and pharmacy. The public system reimburses 70% of standard medical costs.

To cover the remaining 30%, most residents carry a mutuelle (supplemental insurance) — roughly €50–€150/month for an individual. Total healthcare out-of-pocket for a healthy adult: €100–€200/month including the mutuelle. A GP visit costs €26.50. Specialist consultations €50–€120. No surprise billing, no network restrictions, no pre-authorization theater.

Starting in 2026, visitor visa holders must pay an annual PUMA contribution of €300–€600 before receiving their Carte Vitale. Workers and self-employed residents on professional visas fund PUMA through their social charges and are not subject to this additional fee.

Before your 3-month waiting period clears, bridge the gap with SafetyWing's Nomad Insurance — around $150–$200/month for solid global coverage with a low deductible.

Cost of Living: Paris vs. The Rest of France

The standard mistake Americans make: they price France using Paris numbers, then conclude it's unaffordable. Paris is expensive. But the Île-de-France region represents roughly 7% of France's land area and has housing costs 40% higher than the rest of the country.

| City | 1BR Rent (Centre) | Monthly Budget (Single) | Character |

|---|---|---|---|

| Paris | €1,200–€2,000 | €3,000–€4,000 | World capital, crowded, electric |

| Lyon | €700–€900 | €1,800–€2,500 | France's food capital, great transport |

| Bordeaux | €700–€900 | €1,700–€2,200 | Wine country, beach access, Atlantic vibe |

| Toulouse | €550–€700 | €1,500–€2,000 | University town, warm, tech hub |

| Marseille | €500–€650 | €1,400–€1,900 | Mediterranean port, rough edges, cheap |

| Montpellier | €600–€800 | €1,500–€2,000 | Young, sunny, beach 10km away |

Groceries at French supermarkets run €250–€350/month for a single person shopping well. Utilities for an 85m² apartment average €183/month. Monthly transit passes: €90.80 in Paris, €65 in Lyon, €45 in Toulouse. The TGV makes it possible to live in Bordeaux and take meetings in Paris in 2 hours — one-way tickets start at €35 booked in advance.

Banking as an American in France

Opening a French bank account requires patience. Traditional French banks (BNP Paribas, Crédit Agricole, Société Générale) want proof of address, a residence permit, and several months of documentation. Expect 4–8 weeks to get a fully functional account.

Faster alternatives: Boursorama for an online account with minimal friction, N26 as a pan-EU neobank, or Revolut as a stopgap. These work for day-to-day spending but may not satisfy landlords who want prélèvements automatiques (automatic bank drafts) from a French account.

Keep your US banking infrastructure alive regardless. Charles Schwab's international brokerage account includes fee-free banking with unlimited ATM rebates worldwide — the default expat banking setup for good reason.

For USD-to-EUR transfers, Remitly offers competitive rates with same-day delivery on most USD-to-EUR transfers, typically beating bank rates by 1–2%.

Don't overlook the virtual mailbox problem. To keep US banks, brokerages, and IRS correspondence working while you live in France, you need a real US street address. Traveling Mailbox ($15/month) provides a physical US address in 50+ cities with digital mail scanning — the site owner uses this personally. Full guide at the virtual mailbox explainer.

Investor Watch: French Accounts to Avoid

The PFIC rules apply in France just as painfully as anywhere else. French mutual funds and UCITS ETFs purchased through a French brokerage are PFICs — subject to a 37%+ punitive IRS tax rate on gains. Keep investment accounts at a US-domiciled brokerage like Schwab or tastytrade. Full breakdown in the PFIC guide for expat investors.

France's Plan d'Épargne en Actions (PEA), a tax-advantaged French investment account, is effectively off-limits for US citizens. The IRS treats it as a foreign trust requiring Form 3520 filings — the administrative cost far outweighs the tax benefit. Most US expat tax advisors say: don't touch it.

Who Should Move to France (And Who Shouldn't)

France makes strong financial sense for:

- Employees of French companies qualifying for the Impatriate Regime — the 8-year 30% exemption combined with PUMA healthcare is a genuinely compelling package.

- Retirees with passive income — visitor visa, excellent healthcare, dramatically lower cost than the US or UK, and a quality of life per dollar that's hard to match in Western Europe.

- Families — subsidized crèche from €0–€600/month based on income, free and high-quality public schools, low-cost family healthcare. For families paying $2,000+/month in US childcare, the math inverts quickly.

France is harder to justify if you're a solo freelancer earning under €40,000. The Profession Libérale visa has administrative overhead, social charges take 22–25% off the top, and you'll need a French accountant. At that income tier, countries with simpler setups — Georgia's 1% flat tax on foreign revenue, Paraguay's territorial system — offer more straightforward structures. See the geographic arbitrage playbook for the full spectrum of options.

The Bottom Line

France charges real taxes. Nobody is pretending otherwise. But the US-France tax treaty is robust, the Foreign Tax Credit works effectively, and the Impatriate Regime hands a meaningful 8-year break to anyone recruited from abroad. Meanwhile, provincial France — Lyon, Toulouse, Bordeaux, Marseille — delivers a quality of life that costs €1,500–€1,800/month for a single person, less than most US mid-tier cities.

The people who struggle with France are those who approach it like a tax optimization play alone. It's not Paraguay. It's not Georgia. It's France — with everything that means: beautiful infrastructure, world-class food, universal healthcare, glacial bureaucracy, and a culture that operates on its own schedule and isn't particularly apologetic about it.

If you can work inside that system — or hire someone to navigate it — the combination of low provincial cost of living, treaty protection from double taxation, and French healthcare is one of the better deals available to American expats in Western Europe.

Financial disclaimer: This post is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws in both the US and France change regularly. Consult a qualified US expat tax attorney and a French-licensed accountant (expert-comptable) before making any decisions about residency, tax elections, or investment accounts in France.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.