The FEIE Retirement Trap: Why Your Tax Break Costs More

Claiming the FEIE can legally bar you from contributing to your Solo 401(k) or IRA. Here is what self-employed expats need to know before the 5-year lock-in bites.

Claiming the FEIE can zero out your Solo 401(k) and IRA contribution limits. Learn how the 5-year lock-in affects self-employed expats.

Here is the counterintuitive reality every self-employed expat needs to hear: the most popular US tax break for Americans abroad — the Foreign Earned Income Exclusion — legally bars you from contributing a single dollar to your Solo 401(k) or IRA the moment you use it to its full potential. In 2025, that means up to $70,000 in annual tax-advantaged retirement space simply evaporates. Most people don't discover this until their CPA delivers the news — often years into overseas life, after the damage has compounded.

This isn't an obscure edge case. The IRS estimates 5.5 to 9 million Americans live abroad, and freelancers, consultants, and digital nomads make up a fast-growing share. For anyone earning self-employment income abroad and defaulting to the FEIE, the retirement consequence is severe, invisible, and — critically — sticky to reverse.

How the FEIE Works — A Quick Refresher

The Foreign Earned Income Exclusion (Form 2555) lets qualifying US citizens and resident aliens exclude foreign earned income from US taxable income. To qualify, you must pass either the Physical Presence Test (330 full days outside the US in any 12-month period) or the Bona Fide Residence Test (established residence in a foreign country for a full tax year).

For 2025, the exclusion limit is $130,000 per qualifying person — up from $126,500 in 2024. Married couples where both qualify can exclude up to $260,000 combined. The exclusion adjusts annually for inflation and is indexed to $130,000 in 2025.

The appeal is obvious. Exclude $130,000 in earned income and you owe zero federal income tax on that amount. For expats in low-tax or zero-tax countries — UAE, Paraguay, Cayman Islands — the FEIE is the default play. But it carries a hidden cost that can dwarf any single year's tax savings when measured over a career.

The Retirement Contribution Rule Nobody Warns You About

IRC Section 415 governs contribution limits for retirement accounts. The foundational rule: contributions must be based on compensation — specifically, taxable earned income. When you claim the FEIE, the IRS treats excluded income as if it never existed for retirement purposes.

This isn't a gray area or a loophole. It's explicit IRS guidance from Publication 590-A:

"For IRA purposes, compensation does not include amounts excluded from income under the foreign earned income exclusion."

The same principle governs Solo 401(k) plans under IRC Section 415(c). Both your employee deferral limit and your employer profit-sharing contribution are tied to your compensation base. If FEIE reduces that base to zero, your contribution limit is zero. You can open a Solo 401(k). You just can't put anything in it.

For a deeper look at how this interacts with the broader self-employment tax trap for expat freelancers, the compounding problem gets worse when you see the full picture.

The Math: Three Scenarios Side by Side

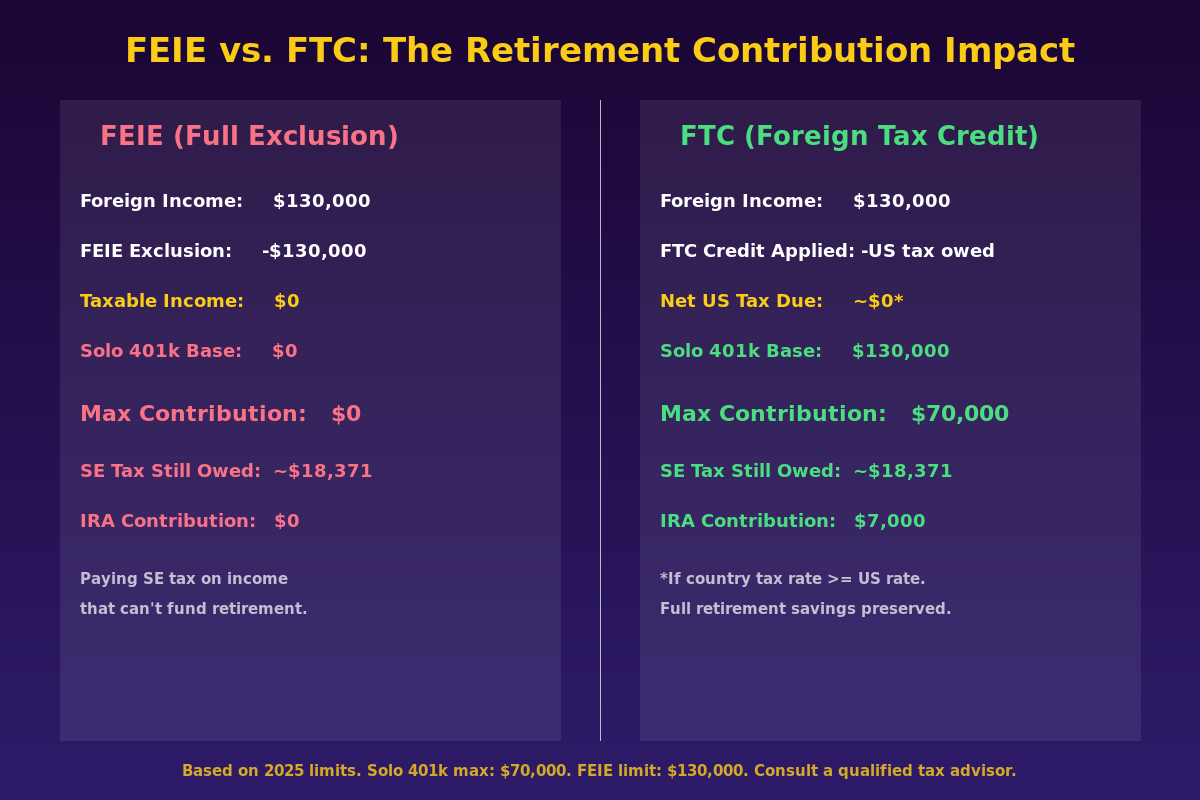

Numbers make this concrete. Assume a self-employed consultant living in Lisbon earns $130,000 in 2025.

| Scenario | Foreign Income | FEIE Claimed | Taxable Compensation | Solo 401(k) Max | IRA Contribution |

|---|---|---|---|---|---|

| Full FEIE | $130,000 | $130,000 | $0 | $0 | $0 |

| Partial FEIE | $160,000 | $130,000 | $30,000 | ~$8,500* | $7,000 |

| FTC Only (no FEIE) | $130,000 | $0 | $130,000 | $70,000 | $7,000 |

*Partial scenario: employee deferral of $23,500 + employer contribution ~20% of net self-employment income after SE deduction on $30,000 base. Actual amount depends on specific SE income calculation.

The difference between row one and row three is $70,000 per year in potential tax-advantaged retirement savings. Over a decade, at 7% annualized growth, that gap compounds to roughly $967,000 in foregone wealth. That's before accounting for the tax-deferred compounding that makes retirement accounts powerful in the first place.

The SE Tax Irony That Makes This Worse

Here's what makes the FEIE retirement trap genuinely maddening: the FEIE does not eliminate self-employment tax.

Self-employment tax — 15.3% (12.4% Social Security on income up to the $176,100 wage base in 2025, plus 2.9% Medicare) — applies to net self-employment income regardless of the FEIE election. On $130,000 of foreign self-employment income, after the 50% SE deduction that reduces the taxable SE base to approximately $120,055, you owe roughly $18,368 in SE tax.

You are paying $18,000+ in taxes on income that cannot fund retirement accounts. That's not an opportunity cost abstraction — it's real money flowing into Social Security and Medicare that many expats will never fully collect, on an income base that the retirement contribution rules treat as if it doesn't exist. The FEIE was designed to prevent double income taxation. It was never designed to fix the SE tax problem or the retirement savings lockout that it creates.

The IRA Excess Contribution Trap

The IRA version of this problem is quieter but financially dangerous. If you contribute to a Traditional or Roth IRA in a year when you excluded all earned income under the FEIE, you've made an excess contribution. The IRS charges a 6% annual excise tax — assessed on Form 5329 — on excess contributions for every year they remain in the account.

A $7,000 excess contribution left in an IRA for five years costs $2,100 in penalties alone, before any tax on the underlying income. Many expats discover this only when preparing amended returns or during an examination. The fix requires either withdrawing the excess plus earnings by the tax filing deadline, or applying the excess toward a future year when you have qualifying earned compensation.

For Roth IRA holders, excess contributions also complicate the backdoor Roth conversion strategy that many expats rely on for tax-free growth — a domino effect that can take multiple years and amended filings to clean up.

The Alternative: Foreign Tax Credit

The Foreign Tax Credit (Form 1116) is the FEIE's primary alternative. Instead of excluding foreign income from your return, you claim a dollar-for-dollar credit for income taxes paid to a foreign government against your US tax liability.

The critical difference: the FTC does not exclude income. Your foreign earnings remain "earned compensation" under IRC Section 415. The full income base is available for retirement contributions. In countries where local tax rates at or exceed US rates — most of Western Europe, Canada, Australia, Japan, Germany — the FTC typically eliminates your US federal income tax to zero, just as the FEIE does. Same after-tax result on your 1040. Entirely different retirement savings outcome.

| Factor | FEIE (Form 2555) | Foreign Tax Credit (Form 1116) |

|---|---|---|

| US income tax eliminated? | Yes, up to $130,000 | Often yes (if foreign rate ≥ US rate) |

| Solo 401(k) contribution base | Reduced or zero | Full income preserved |

| IRA eligibility | Eliminated with full FEIE | Fully preserved |

| Best jurisdiction fit | Zero/very low-tax countries | Countries with 20%+ income tax |

| Income over $130k limit | Excess taxed at US rates | All income eligible for credit |

| Self-employment tax | Still owed (no relief) | Still owed (no relief) |

The FTC is not universally superior. For expats living in genuinely zero-tax environments — UAE, Bahrain, the Cayman Islands, Paraguay — there may be no foreign tax to credit, meaning the FTC provides no offset and US income tax owed is real. In those cases, the FEIE may still win on net taxes paid even after accounting for the retirement savings cost. But that calculation needs to be made explicitly, not assumed.

The 5-Year Lock-In: Why This Decision Is Sticky

Once you revoke the FEIE election, you cannot re-elect it for five years without IRS approval. This constraint — codified in the FEIE election rules — is the reason this decision carries real stakes.

Practical scenarios where the lock-in matters:

- You switch to FTC, then relocate to a zero-tax country in year two. You're locked out of the FEIE until year six. You may owe meaningful US income tax on income that would have been fully excluded.

- Your income drops significantly after switching. In a low-income year, the FTC may provide less credit than you'd get from just excluding income under FEIE. You can't switch back for five years.

- Tax law changes. If Congress modifies the FEIE or FTC rules during your lock-in period, you're operating under whatever framework existed when you made the election.

The flip side: if you've never elected the FEIE, you can elect it for the first time at any point — the five-year restriction only applies to re-election after revocation. First-time FEIE elections are not locked in.

This is why the FTC vs. FEIE decision should be modeled in a spreadsheet with your specific income, country tax rate, planned retirement contributions, and at least a 5-year horizon — before you commit either way. See the dedicated guide on FEIE vs. Foreign Tax Credit for the full comparison framework.

What About the SEP-IRA?

The SEP-IRA is frequently mentioned as a simpler alternative to the Solo 401(k) for self-employed expats. The employer contribution limit is 25% of net self-employment income (after the SE deduction), up to $70,000 in 2025.

The same FEIE trap applies. SEP-IRA contributions are based on taxable compensation under the same IRC framework. If FEIE excludes your full earned income, your SEP-IRA contribution limit is also zero. The simpler administration doesn't change the underlying compensation requirement. For expats who want to avoid the annual Form 5500-EZ filing requirement of a Solo 401(k), the SEP-IRA is a reasonable choice — but it doesn't solve the FEIE problem.

Decision Framework: FEIE or FTC?

No single answer fits everyone. Use this as a starting point for the conversation with your CPA:

- Living in a zero or near-zero tax country (UAE, Paraguay, Cayman, Bahrain)? FEIE is likely the right call on tax savings. But calculate the retirement savings gap explicitly. If you have $50,000/year in potential retirement contributions you're forgoing, that cost needs to appear in your model.

- Living in a country with effective tax rate above 25% (Portugal, Germany, UK, Australia, Canada)? FTC typically eliminates your US liability completely while preserving the full retirement base. Switching often costs nothing on current-year taxes while unlocking six figures of annual retirement space.

- Self-employment income under $130,000, actively building retirement savings? Run the FTC numbers. In most high-tax jurisdictions, FTC wins on the complete picture.

- Income above $200,000? The FEIE covers only the first $130,000 — the excess is taxed at US rates regardless. At this income level, a hybrid approach or pure FTC strategy is worth modeling.

- Married, both spouses with self-employment income abroad? Each can claim the FEIE separately for a combined $260,000 exclusion — but both face the retirement lockout on their respective income.

The expat 401(k) and IRA retirement guide covers the mechanics of setting up and funding retirement accounts once you've resolved the FEIE vs. FTC question. The comprehensive FEIE guide covers the full mechanics of claiming the exclusion.

What to Do Now

If you're currently claiming the FEIE and haven't funded a retirement account in years, three concrete actions:

- Model the FTC switch before next tax year. Get your effective foreign tax rate for the current year. If it's at or above your marginal US rate, switching to FTC may cost nothing in additional US taxes while unlocking your full retirement contribution base. Do this analysis with a CPA who specializes in US expat taxation — not a generalist who files a handful of expat returns per year.

- Audit prior IRA contributions for excess amounts. If you contributed to a Traditional or Roth IRA in any year you fully excluded income under FEIE, you likely have excess contributions accumulating a 6% annual penalty. Address them via Form 5329. The fix is annoying but manageable if caught early; ignoring it compounds the problem and creates a larger amended-return headache later.

- Establish a Solo 401(k) in the year you switch to FTC. The plan must be established by December 31 of the tax year you want to contribute for. Employee salary deferral contributions can be made up to the tax filing deadline including extensions (October 15 for most expats who file extensions). Charles Schwab International offers a Solo 401(k) with no custodial fees, no minimum balance, and free ATM access worldwide — critical for expats who need to access accounts from abroad. tastytrade is another option if you plan to actively invest within the plan; their Solo 401(k) has no account fees and commission-free equities.

For expats maintaining a US mailing address — required for IRS correspondence, state domicile, and keeping US banking accounts open — Traveling Mailbox ($15/month) provides a real US street address in 50+ cities with mail scanning and check deposit services. The site owner uses this personally. It's essential infrastructure if you're managing US financial accounts from abroad and need a reliable address for tax documents.

Once you're funding retirement accounts, the expat investing playbook covers what to hold inside vs. outside tax-advantaged accounts — especially the PFIC (passive foreign investment company) rules that trip up expats who buy foreign mutual funds in taxable accounts.

The 30-Year Cost of a One-Year Tax Break

The FEIE is a legitimate, powerful tool — when used deliberately. For self-employed expats who default to it without modeling the retirement impact, it functions as a 30-year compounding liability disguised as a tax benefit. Paying $18,000+ in SE tax on income that cannot fund retirement accounts while domestic peers max out $70,000 Solo 401(k)s isn't bad luck — it's a planning gap with a specific, fixable cause.

The 5-year lock-in on FEIE revocation means this isn't something you can casually unwind when you realize the cost. Model it now, decide with full information, and commit before another year of contribution capacity expires permanently.

A 45% of American expats cite retirement planning as an ongoing financial challenge. For the self-employed subset, the FEIE trap explains a significant share of why.

Financial disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. US international tax law is highly fact-specific and changes frequently. The interaction between FEIE, FTC, Solo 401(k) contributions, SEP-IRA limits, and self-employment tax depends on your individual income level, country of residence, applicable tax treaties, and filing status. Consult a qualified CPA or tax attorney who specializes in US expatriate taxation before changing any tax election. Prior contribution years with errors may require amended returns and Form 5329 filings. The site owner may receive compensation for affiliate links in this post.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 16, 2026

Expat Tax & FinanceMay 16, 2026

The FEIE-Roth IRA Trap Costing Expats $500K at Retirement

The FEIE excludes income from U.S. tax — but blocks Roth IRA contributions. Learn the 5-year trap and preserve retirement savings abroad.

Expat Tax & FinanceMay 12, 2026

Expat Tax & FinanceMay 12, 2026

Solo 401(k) Abroad: Self-Employed Expats Save $72k

Self-employed expats can contribute up to $72,000/year to a Solo 401(k). But the FEIE trap can wipe out your eligibility. Here's how to navigate it.

Expat Tax & FinanceMay 6, 2026

Expat Tax & FinanceMay 6, 2026

Capital Gains Tax: The FEIE Blind Spot Expats Pay For

The FEIE shields your salary but not your stock gains. Learn how NIIT, the stacking rule, and Section 865(g) affect US expat capital gains taxes.