You earn your income overseas, owe nothing to the IRS after the Foreign Earned Income Exclusion, and haven't set foot in the US in three years. The government couldn't possibly care about your bank account in Thailand — right?

Wrong. The IRS handed one American expat a $2.7 million FBAR penalty for accounts he thought were below the radar. Another couple received a $450,000 bill for a retirement account they inherited and didn't know had to be reported. Neither owed a single dollar of US income tax on those accounts.

FBAR and FATCA are the two parallel foreign-account reporting systems that operate completely independently of whether you owe tax. Understanding both — and how they interact — is the difference between a clean filing and a penalty that can literally wipe out your overseas savings.

What Is FBAR?

FBAR stands for Report of Foreign Bank and Financial Accounts. It's filed on FinCEN Form 114 — not with your tax return, but through a separate system run by the Financial Crimes Enforcement Network (FinCEN), a bureau of the US Treasury.

The filing trigger is deceptively simple: if the aggregate value of all your foreign financial accounts exceeded $10,000 at any single moment during the calendar year, you must file. Not $10,000 in each account — $10,000 combined, across all foreign accounts, for even one day.

Have $6,000 in a Thai savings account and $5,000 in a UK investment account? You crossed $10,000 on the day both balances existed simultaneously, and you owe an FBAR. This catches people constantly.

What counts as a "foreign financial account" for FBAR purposes:

- Bank accounts (checking, savings, time deposits)

- Securities accounts and brokerage accounts

- Mutual fund accounts held at a foreign institution

- Futures or options accounts at a foreign exchange

- Life insurance or annuity contracts with a cash surrender value held abroad

- Foreign pension accounts (including employer-sponsored)

- Crypto exchanges based outside the US (rules evolving — see below)

The FBAR deadline is April 15, with an automatic extension to October 15 — no form needed to request the extension. You file FinCEN 114 online at the BSA E-Filing System, separate from your tax return. It's free. And critically: you must check the box on Schedule B of Form 1040 disclosing foreign accounts — even if that account is below $10,000.

What Is FATCA?

FATCA — the Foreign Account Tax Compliance Act — is the IRS's version of foreign account reporting, and it has a completely different architecture. Passed in 2010, FATCA requires two things simultaneously: US taxpayers must report their foreign assets on Form 8938, and foreign financial institutions must report accounts held by US persons directly to the IRS.

That second piece is what gives FATCA its teeth. More than 110 countries have signed FATCA intergovernmental agreements. Your bank in Singapore, your brokerage in Germany, your savings account in Mexico — they are contractually required to identify US account holders and report balances, income, and transactions to the US government. They don't wait for you to volunteer the information.

The Form 8938 thresholds are significantly higher than FBAR and differ based on where you live:

| Filing Status | Living Abroad — Year-End Value | Living Abroad — Any Time During Year |

|---|---|---|

| Single / Married Filing Separately | $200,000 | $300,000 |

| Married Filing Jointly | $400,000 | $600,000 |

For US residents, the thresholds drop to $50,000 (year-end) / $75,000 (any time) for single filers and $100,000 / $150,000 for joint filers. Moving abroad more than doubles the threshold before Form 8938 kicks in.

Unlike FBAR, Form 8938 is attached to your federal tax return (Form 1040) and administered by the IRS — not FinCEN. It also covers a broader category of assets. Foreign real estate itself isn't reportable on either form, but a foreign entity that holds real estate absolutely is.

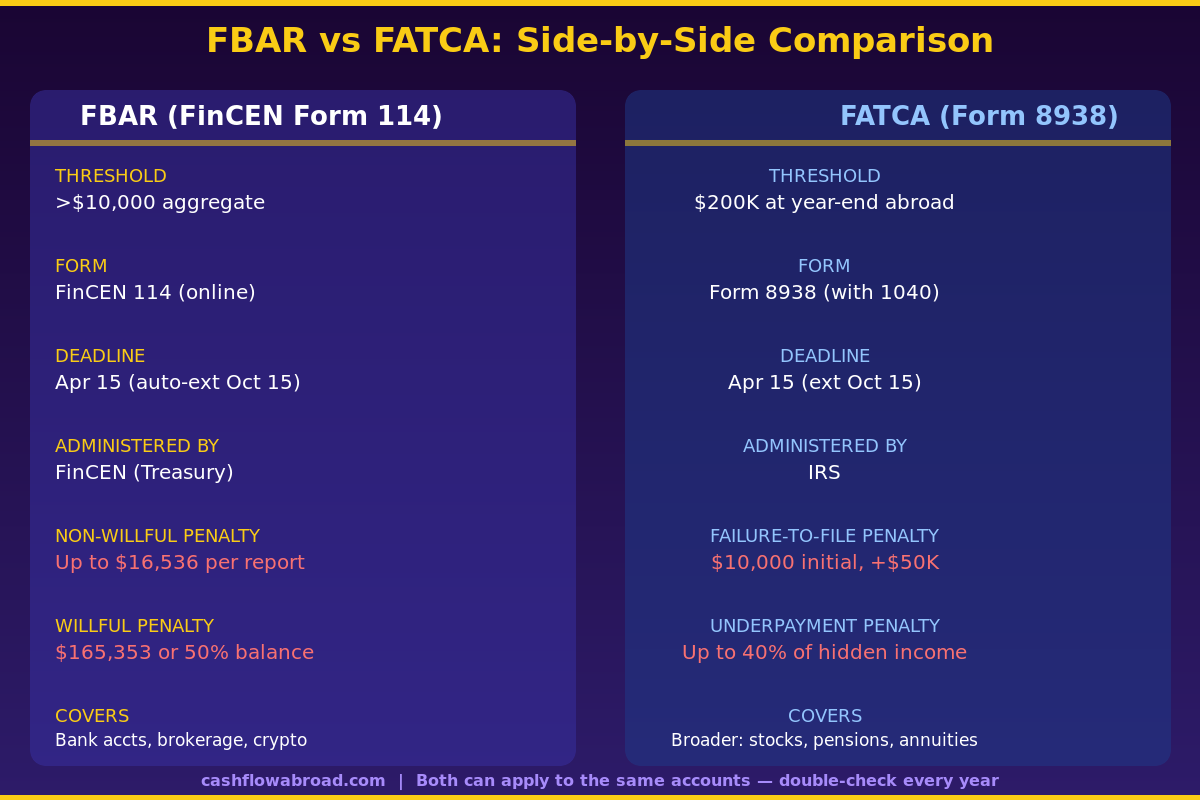

FBAR vs FATCA: The Critical Differences

| Feature | FBAR (FinCEN 114) | FATCA (Form 8938) |

|---|---|---|

| Filing threshold | $10,000 aggregate (any day during year) | $200,000 year-end / $300,000 any time (single abroad) |

| Form | FinCEN Form 114 (BSA E-Filing — separate from tax return) | Form 8938 (attached to Form 1040) |

| Administered by | FinCEN (Treasury Department) | IRS |

| Deadline | April 15 (auto-extension to October 15) | April 15 (extended with 1040 extension) |

| Non-willful penalty | Up to $16,536 per report | $10,000 initial + up to $50,000 continuing |

| Willful penalty | $165,353 or 50% of account balance (per account, per year) | Tax fraud penalties apply (no separate FATCA "willful" tier) |

| Criminal exposure | Up to 10 years and $500,000 | Tax evasion charges under IRC §7201 |

| Asset scope | Financial accounts at foreign institutions | Broader: includes foreign stocks, bonds, interests in foreign entities |

| Foreign institution reporting | No (only US-person self-reporting) | Yes — banks report you directly to the IRS under FATCA IGAs |

The most important thing to internalize: these are not alternatives — they're cumulative. If you have $250,000 in a foreign brokerage account, you need to file both. Missing one while filing the other is still a violation.

The FBAR Penalty: How Bad Can It Actually Get?

Here's the scenario that keeps expat tax attorneys busy: someone moves abroad, opens a local bank account, accumulates savings over a decade, and genuinely doesn't know FBAR exists. They've been filing US taxes every year, paying whatever they owe. They never told their accountant about the foreign accounts because nobody asked.

Then they get a letter.

The FBAR penalty structure has two tiers:

Non-willful violations: Up to $16,536 per report (2026 inflation-adjusted figure). Following the 2023 Supreme Court decision in Bittner v. United States, this applies per form filed — not per account. This matters enormously if you have multiple foreign accounts. Before Bittner, the government argued each account represented a separate violation. The Court rejected that interpretation. One form = one potential penalty, regardless of whether it reports 1 account or 20.

Willful violations: The greater of $165,353 or 50% of the highest account balance — applied per account, per year. This is where the math becomes catastrophic. A $200,000 account you "willfully" failed to report for five years? The IRS can theoretically assess penalties totaling hundreds of thousands of dollars, or more than the account's entire value. In practice, the IRS often settles for significantly less, but the statutory exposure is real.

"Willful" doesn't require proof of intent to defraud. Courts have found willfulness in cases where someone checked "no" on Schedule B when asked about foreign accounts, or where someone simply "should have known" about the requirement. Ignorance can support a non-willful defense — but it requires documentation: a written certification, and a credible explanation for why you didn't know.

What Accounts Trigger Both FBAR and FATCA?

Most foreign bank accounts that clear the FATCA threshold will also require FBAR. But the reverse isn't true: a $15,000 foreign savings account triggers FBAR but not FATCA (below the $200K threshold). Some assets require FATCA but not FBAR — for example, stock held directly in a foreign corporation doesn't sit in an account at a foreign financial institution, so it may be FATCA-reportable without triggering FBAR.

Particular gray areas that catch people off guard:

- Foreign pension plans: Both forms may apply. An employer-sponsored foreign pension with a balance over $10,000 triggers FBAR. If the total value exceeds FATCA thresholds, Form 8938 too. The pension may also have treaty implications for US tax treatment.

- Foreign mutual funds: Widely reportable under both, and often also classified as Passive Foreign Investment Companies (PFICs) — triggering a third reporting requirement under Form 8621. The triple-layer reporting on a routine index fund held at a foreign broker is one reason many expats use US-based brokerages like Charles Schwab International instead — which also offers free ATM rebates worldwide, making it a practical solution for expat daily banking. The full case for US-domiciled investing is laid out in the PFIC guide.

- Cryptocurrency on foreign exchanges: FinCEN has signaled that foreign crypto exchange accounts will be subject to FBAR. The IRS already includes crypto at foreign custodians as "specified foreign financial assets" under FATCA. If your exchange is domiciled outside the US and holds more than $10,000 in aggregate, treat it as reportable now.

- Joint and signature-authority accounts: If you have signature authority over a foreign business account — even if the money isn't yours — you may need to file FBAR for that account. The account doesn't need to be in your name.

How the IRS Actually Catches Non-Filers

The old assumption — "my foreign bank won't tell the IRS" — died in 2014 when FATCA went live. Here's the enforcement architecture as of 2026:

Foreign financial institutions report directly to the IRS (or to their local tax authority, which shares with the IRS under FATCA intergovernmental agreements). The IRS's Compliance Data Warehouse matches those reports against US tax returns. If a foreign bank reports $180,000 in your account to the IRS, and you didn't attach Form 8938 or check the Schedule B box, that mismatch generates a computer flag.

In 2025, the IRS rolled out AI-enhanced pattern analysis that cross-references wire transfer data, passport records, foreign employment income, and FATCA bank reports. The framework described in detail in our analysis of CARF and global data sharing has materially raised the detection probability for non-filers. Add to this the OECD's Common Reporting Standard (CRS), which covers dozens of non-FATCA countries and feeds data into the same intelligence picture. The era of offshore accounts being truly invisible to the IRS is over.

One practical note on access: when logging into US financial accounts from abroad, some institutions use geo-blocking or trigger fraud alerts for foreign IP addresses. A reliable VPN like NordVPN lets you route through a US server so your banking sessions don't get flagged or locked — a legitimate use case that every expat using US banking will eventually encounter.

Already Behind? The Streamlined Filing Lifeline

If you've been a non-filer and haven't been contacted by the IRS yet, you have a path to come clean through the Streamlined Filing Compliance Procedures. Two tracks exist:

Streamlined Foreign Offshore Procedures (SFOP) — for US persons who have lived outside the US for at least one of the last three years and spent no more than 35 days per year in the US:

- File 3 years of amended/delinquent tax returns

- File 6 years of delinquent FBARs

- Submit a signed certification that your failure was non-willful

- Miscellaneous offshore penalty: 0%

Streamlined Domestic Offshore Procedures (SDOP) — for US-based filers who don't qualify for SFOP:

- Same 3-year / 6-year filing requirement

- Miscellaneous offshore penalty: 5% of the highest aggregate foreign account balance across the 6-year period

The critical warning: streamlined procedures are only available to non-willful violators who haven't already been contacted by the IRS about those accounts. If you're currently under examination, you need Voluntary Disclosure Practice (VDP) — a different, more expensive route that provides criminal protection but comes with higher penalties.

A reliable US mailing address is essential throughout this process — IRS correspondence, amended return confirmations, and any audit notices all go to your address of record. Many expats maintain their US address through Traveling Mailbox (from $15/month), which provides a real US street address in 50+ cities, scans incoming mail, and forwards documents digitally. Nothing from FinCEN or the IRS slips past an abandoned address while you're living abroad. Read the full guide on virtual mailboxes for expats for the full setup walkthrough.

How to Actually File These Forms

Filing FBAR (FinCEN 114)

- Go to the BSA E-Filing System (bsaefiling.fincen.treas.gov)

- Create an account (separate from IRS.gov)

- Select FinCEN Report 114

- Enter each foreign account: institution name, country, account number, type of account, highest balance during the year, and whether you held financial interest or signature authority only

- Submit — you'll receive a confirmation number to keep for your records

No tax owed. No fee. Roughly 20 minutes for a simple case.

Filing Form 8938

Attach it to your Form 1040 when filing your federal return. Most expat tax software includes Form 8938. If you're using a CPA, confirm they're explicitly asking about all foreign accounts and assets — not just the ones generating reportable income.

For expats who want to minimize the number of foreign accounts in their FBAR, keeping primary banking at a US institution helps significantly. Mercury works well for expat freelancers and business owners. Charles Schwab International offers fee-free checking with worldwide ATM reimbursements, which many expats use as their primary account to reduce reliance on foreign retail banks entirely. See the complete US expat banking guide for the full stack.

Five FBAR/FATCA Mistakes That Cost Expats the Most

- Counting only year-end balances. FBAR triggers on the highest value during the year, not December 31. A savings account that peaked at $12,000 in March and held $4,000 on December 31 still required filing. Most people check their year-end balance and incorrectly conclude they're below threshold.

- Forgetting signature-authority accounts. If you're an authorized signatory on a foreign business account — even a corporate account where you personally own nothing — you may need to include it in your FBAR. This is a very common oversight for expats running foreign businesses.

- Treating FBAR and FATCA as interchangeable. Filing one doesn't satisfy the other. Missing FATCA while filing FBAR is still a $10,000 penalty exposure for the year.

- Ignoring foreign pensions. A UK pension, a Canadian RRSP, or a local superannuation in Australia — these are reportable. If the balance ever crossed $10,000, FBAR applies. The intersection with PFIC rules makes these accounts particularly complicated; get a specialist to review them. The PFIC guide covers the mechanics.

- Leaving dormant accounts open. An account with $15 in it that you forgot to close still triggers FBAR if the aggregate crosses $10,000 (because your other accounts push the total over). Close accounts you don't use.

The Crypto Question

FinCEN has proposed rules explicitly subjecting foreign crypto exchange accounts to FBAR. The IRS already treats crypto at foreign custodians as "specified foreign financial assets" under FATCA. As of 2026, enforcement is still catching up with the rule-making, but the direction is unambiguous.

If you use exchanges domiciled outside the US — Binance (Cayman Islands), Bybit (Dubai), Bitget (Seychelles) — and the aggregate value of all your foreign accounts including those exchanges has ever exceeded $10,000, you should be filing FBAR. The full analysis of how crypto interacts with US expat tax obligations is in the crypto taxes guide for US expats.

You Can Owe Zero US Tax and Still Owe These Reports

This is the psychological trap. FBAR and FATCA are information reporting requirements — not tax assessments. Using the Foreign Earned Income Exclusion to zero out your US tax bill has absolutely no bearing on whether you must file these forms. The FEIE excuses you from tax, not from disclosure.

Many expats who have optimized their tax position to zero conclude they have "nothing to report." The IRS sees it differently. The foreign account reporting regime was built precisely for people with significant foreign assets — many of whom are fully compliant taxpayers who simply hold wealth abroad.

The Bottom Line

FBAR and FATCA are not obscure technicalities — they are the IRS's primary surveillance infrastructure for foreign wealth. The enforcement environment in 2026, with FATCA bank-level reporting, AI-enhanced cross-referencing, and expanding CARF data-sharing agreements, means the probability of detection for non-filers has never been higher.

The compliance cost is low: both forms are free to file, take less than an hour for a straightforward situation, and there's a legitimate amnesty path for anyone who has fallen behind non-willfully. The cost of non-compliance is measured in five to six figures. File both. File every year. And if you've been skipping them, use Streamlined Procedures before the IRS finds you first.

Financial Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. FBAR and FATCA compliance involves complex rules that vary based on your specific circumstances, account types, and filing history. Consult a qualified expat tax attorney or CPA — particularly one familiar with FinCEN 114 and Form 8938 — before making any compliance decisions. Penalties described reflect 2026 inflation-adjusted figures and are subject to annual adjustment by Treasury.