The IRS assessed roughly $606 million in FBAR penalties in a single fiscal year. Most of those taxpayers weren't criminals. They were ordinary Americans living abroad who either didn't know about these reporting requirements or assumed their zero-dollar tax bill meant they had nothing to file. They were wrong — and so are millions of US expats right now.

FBAR and FATCA are two entirely separate reporting obligations that have nothing to do with how much tax you owe. They exist to tell the US government what foreign financial accounts and assets you hold. Miss either one, and the penalties start at $10,000 — even if you owe $0 in taxes. Understanding exactly who must file, what must be reported, and how the thresholds actually work is non-negotiable for every American living outside the United States.

What Is FBAR — and Why Most Expats Misunderstand It

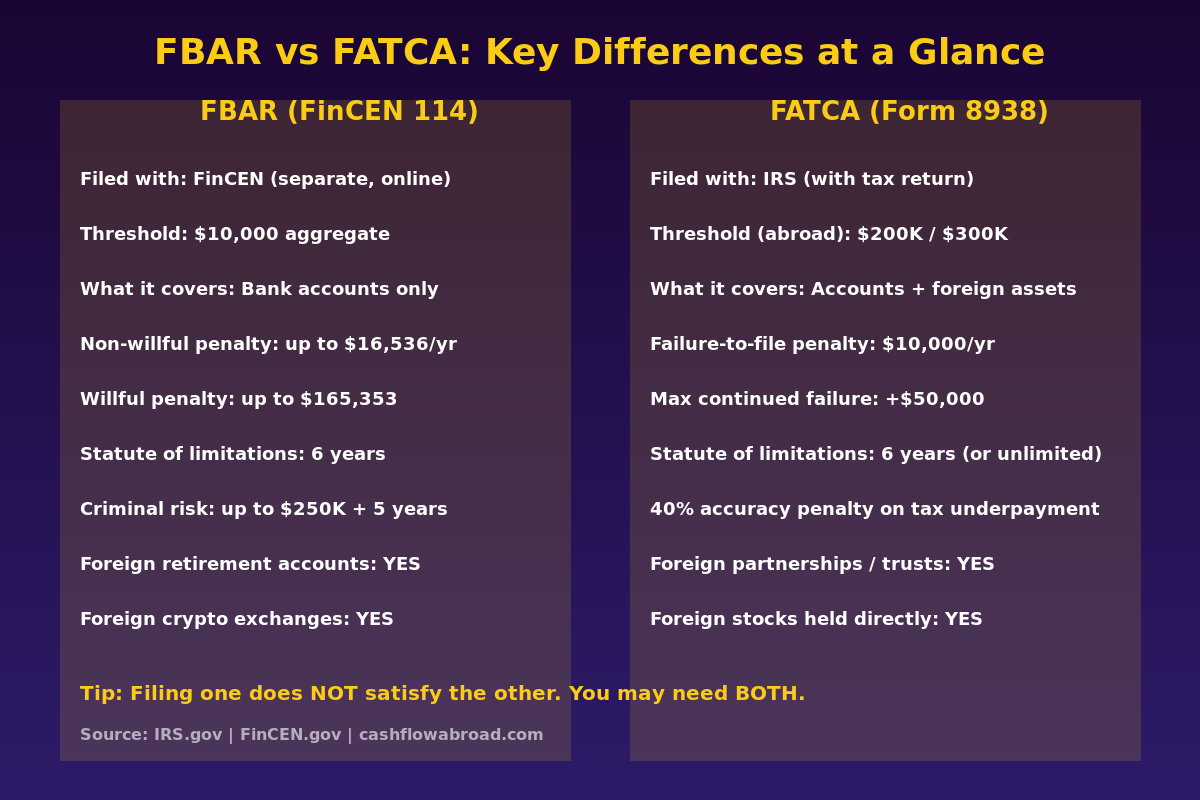

FBAR stands for Report of Foreign Bank and Financial Accounts. The actual form is FinCEN Form 114, filed with the Financial Crimes Enforcement Network — a bureau of the US Treasury. Not the IRS. That distinction matters: many expats who think they filed their FBAR by attaching something to their tax return did not file it at all.

The filing threshold is $10,000 aggregate across all foreign financial accounts at any single point during the calendar year. That phrase "aggregate" is where most people get tripped up. If you have three foreign accounts — one with €2,000, one with S$3,500, and one with £2,000 — and their combined value in USD ever exceeded $10,000 simultaneously, you have an FBAR obligation. The threshold is not per account. It is not an annual average. It is a snapshot: one day above $10,000 combined creates a filing requirement for the entire year.

FBAR is filed electronically through FinCEN's BSA E-Filing System at bsaefiling.fincen.treas.gov. Paper FBARs are not accepted with very limited exceptions. The deadline is April 15, with an automatic extension to October 15 that requires no action on your part — no form, no request, no acknowledgment. It mirrors your tax return extension window but is entirely separate from it.

What Accounts Must Be Reported on FBAR

FBAR covers foreign financial accounts. The scope is narrower than FATCA but still catches more than most people expect:

- Foreign bank checking and savings accounts

- Foreign brokerage and investment accounts

- Foreign mutual funds held in accounts

- Foreign-issued life insurance policies with a cash surrender value

- Foreign annuity contracts

- Foreign pension accounts structured as individual accounts you control

- Any account over which you have signature authority — even if you have no ownership interest (e.g., a company bank account you're authorized to sign on)

What FBAR does not require: foreign stocks or securities held directly outside an account, real estate held directly, and precious metals held directly. As of 2025, cryptocurrency is also not currently reportable on FBAR — FinCEN has proposed rules but they are not final.

What Is FATCA — and How It Differs From FBAR

FATCA stands for the Foreign Account Tax Compliance Act, enacted in 2010. The individual reporting obligation is Form 8938, filed directly with the IRS as an attachment to your Form 1040. Unlike FBAR, it goes to the IRS and it is part of your tax return package.

The threshold is significantly higher for Americans abroad — and it has a dual trigger that most people miss:

| Filing Status | US-Based Threshold | Living Abroad Threshold |

|---|---|---|

| Single / MFS | $50,000 (year-end) or $75,000 (any point) | $200,000 (year-end) or $300,000 (any point) |

| Married Filing Jointly | $100,000 (year-end) or $150,000 (any point) | $400,000 (year-end) or $600,000 (any point) |

The dual-test structure is critical: exceeding either the year-end balance OR the "any point during the year" balance triggers the filing requirement. A large mid-year account balance can force a Form 8938 filing even if your December 31 balance is below the threshold. This catches investors who received a lump sum, sold assets, or moved money mid-year.

One important carve-out: taxpayers who don't meet the US income filing threshold and don't file a Form 1040 at all are not required to file Form 8938, even if they hold qualifying foreign assets exceeding these amounts.

What Assets Must Be Reported on Form 8938

FATCA covers a broader category than FBAR: "specified foreign financial assets." This includes everything FBAR covers, plus:

- Foreign stock or securities held directly (not inside a brokerage account) — the major expansion vs. FBAR

- Foreign partnership interests

- Foreign hedge funds and private equity funds

- Foreign-issued annuities and life insurance with cash value (broader than FBAR)

- Financial instruments or contracts with a foreign counterparty

- Interests in a foreign estate

- Foreign pension plans and deferred compensation plans (broader coverage than FBAR)

One nuance: if a foreign financial account is reportable on FBAR, its value counts toward the Form 8938 threshold. You report the account on FBAR and reference it on 8938 by checking the relevant box — you don't need to describe each individual account twice.

For more on how these reporting obligations interact with your broader US tax picture, see our complete US expat banking and taxes guide.

The Penalties: Where Things Get Serious

The asymmetry between FBAR and FATCA penalties is jarring. FBAR carries dramatically higher potential exposure.

FBAR Penalties (2025 Inflation-Adjusted)

| Violation Type | Maximum Penalty |

|---|---|

| Non-willful | Up to $16,536 per violation |

| Willful | Greater of $165,353 per violation or 50% of account balance |

| Willful (criminal) | Up to $250,000 fine and/or 5 years imprisonment |

| Willful + other crime | Up to $500,000 fine and/or 10 years imprisonment |

"Per violation" historically meant "per account per year" — so three unreported foreign accounts over five years equaled 15 separate violations at up to $16,536 each. That math produces $247,000 in penalties for someone who might owe $0 in taxes.

The Supreme Court addressed this in Bittner v. United States (2023): for non-willful violations, penalties are now assessed per FBAR report (once per year), not per account. This was a landmark ruling that dramatically reduced potential non-willful liability. The willful penalty structure was not affected.

The IRS's definition of "willful" is broader than most people assume. It includes deliberate non-disclosure, but also "willful blindness" — ignoring rules you reasonably should have known about. Claiming you "didn't know" is not automatically a defense if the IRS can demonstrate you had access to information that should have prompted investigation.

Form 8938 / FATCA Penalties

| Violation Type | Penalty |

|---|---|

| Failure to file / incomplete | $10,000 initial penalty |

| Continued failure (after IRS notice) | +$10,000 per 30-day period, up to $50,000 |

| Underpayment from undisclosed foreign assets | Additional 40% penalty on underpayment |

| Fraud | 75% penalty on underpayment |

There is a compounding statute of limitations consequence: if you fail to file Form 8938, the statute of limitations on your entire federal tax return stays open indefinitely — giving the IRS unlimited time to assess taxes for that year.

Why the IRS Already Knows About Your Accounts

FATCA is not just an individual reporting obligation — it is a global data-sharing infrastructure. As of 2025, the US has signed or reached Intergovernmental Agreements (IGAs) with 113+ countries and jurisdictions, requiring foreign financial institutions to report US account holders' names, balances, and income to tax authorities, which then share the data with the IRS.

Major expat destinations covered include the UK, Canada, Australia, Germany, France, Japan, Singapore, UAE, Mexico, Brazil, Spain, Colombia, Panama, Ireland, India, South Korea, and Switzerland. The IRS receives this data and cross-references it against individual filings — meaning the government often has your foreign account information before you decide whether or not to file.

The enforcement trajectory is clear. The UBS case in 2009 — UBS paid $780 million and disclosed 4,450 account names — triggered the FATCA era. The Swiss bank program from 2013 to 2016 resulted in over 80 Swiss banks paying a combined $1.36 billion in penalties and surrendering account holder data. The assumption that a foreign bank account is invisible to US authorities has been empirically false for over a decade.

10 Mistakes That Get US Expats Into Trouble

- Assuming the $10,000 threshold is per account. It's aggregate across all accounts simultaneously. Three accounts at $4,000 each = FBAR required.

- Filing FBAR with the IRS. FBAR goes to FinCEN via bsaefiling.fincen.treas.gov. Sending it to the IRS does not count.

- Assuming a zero tax bill means no filing. FBAR and Form 8938 are independent of tax liability. You can owe $0 and still face penalties.

- Not reporting accounts where you have signature authority. A company bank account you're authorized to sign on must appear on your personal FBAR if aggregate values exceed $10,000.

- Confusing FBAR's $10,000 with FATCA's thresholds. The $200,000/$400,000 thresholds are for Form 8938 only. FBAR stays at $10,000 regardless of where you live.

- Missing the dual-test trigger on Form 8938. Both year-end balance AND "any point during the year" can independently trigger filing. Mid-year spikes count.

- Assuming foreign pensions don't count. Many employer and private pension accounts abroad qualify for both FBAR and Form 8938.

- Believing the bank handles it. Your bank's FATCA reporting to its government does not satisfy your personal filing obligation.

- Making a quiet disclosure. Simply filing amended returns without entering a formal program is not protected and may be viewed negatively by the IRS.

- Trying to file FBAR by paper. FBAR must be filed electronically via FinCEN's BSA system. Paper is not accepted except in rare circumstances.

These same compliance principles extend to your investment accounts abroad. Foreign investment vehicles carry their own reporting complexity — see our expat investing and PFIC guide for how Passive Foreign Investment Company rules intersect with your broader offshore holdings.

Getting Caught Up Without Penalties: The Streamlined Foreign Offshore Procedure

If you've been living abroad and didn't know about FBAR or Form 8938, there is a formal IRS amnesty program built exactly for this. The Streamlined Foreign Offshore Procedure (SFOP) lets non-willful non-filers get fully current with zero penalties. You still owe back taxes and interest, but all failure-to-file, failure-to-pay, accuracy-related, and FBAR penalties are waived.

Who Qualifies

- Physically outside the US for at least 330 full days in at least one of the three most recent tax years

- Non-compliance must be non-willful — not intentional, reckless, or a product of willful blindness

- No open IRS civil examination of your returns

- Not under criminal investigation

- No prior "quiet disclosure"

- US Green Card holders and dual nationals living abroad can qualify

What You Submit

- 3 years of federal tax returns — with "Streamlined Foreign Offshore" written in red at the top of each

- All required information returns (Forms 5471, 3520, 8938, etc.) for those years

- 6 years of FBARs via FinCEN's BSA E-Filing System — select "Other" and note "Streamlined Filing Compliance Procedures"

- Form 14653 — your signed non-willfulness certification. The most legally critical document. Specificity matters; vague language is a red flag

- Full payment of all taxes owed plus IRS statutory interest (currently 7–8%)

Preparation costs typically run $2,000–$10,000+ depending on complexity and number of years. Submissions are paper-only, mailed to the IRS Austin office. The previous Offshore Voluntary Disclosure Program (OVDP) closed in September 2018 after collecting over $11.1 billion from approximately 56,000 taxpayers. SFOP is the current path — and it is meaningfully more lenient than anything that came before it.

One practical detail that SFOP filers often overlook: you'll need a current US mailing address for IRS correspondence. A Traveling Mailbox provides a real US street address in 50+ cities with mail scanning and forwarding for around $15/month — critical for maintaining IRS correspondence, banking relationships, and state domicile while living abroad. The site owner personally uses this service.

Annual Filing Checklist for US Expats

Every year, before April 15, run through this:

| Obligation | Form | Filed With | Key Threshold | Deadline |

|---|---|---|---|---|

| FBAR | FinCEN 114 | FinCEN BSA E-Filing | $10,000 aggregate | Apr 15 / Oct 15 auto |

| FATCA | Form 8938 | IRS (with 1040) | $200K/$400K abroad | Same as tax return |

| Foreign Corp | Form 5471 | IRS | 10%+ in foreign corp | Same as tax return |

| Foreign Trust/Gift | Form 3520 | IRS | >$100K from foreign person | April 15 |

| Foreign Partnership | Form 8865 | IRS | 10%+ in foreign partnership | Same as tax return |

For US banking that survives the expat move, Charles Schwab International remains one of the few US brokerages that actively serves Americans abroad — and their checking account reimburses all ATM fees worldwide, which is useful when you're managing international paperwork from multiple time zones.

How FBAR and FATCA Interact With the FEIE

Using the Foreign Earned Income Exclusion to reduce your US tax bill to zero does not eliminate FBAR or FATCA obligations. These are independent reporting systems. Even if your FEIE exclusion means you owe $0 in income tax, if your foreign accounts exceeded $10,000 aggregate at any point during the year, you still file FBAR. If your foreign assets exceeded $200,000 at year-end, you still file Form 8938.

The FEIE also has no impact on whether your foreign bank reports your account to the IRS under FATCA. That reporting happens regardless of your individual tax position. For a full breakdown of how to structure your taxes abroad, see how US expats legally eliminate federal income tax using the FEIE.

The Bottom Line

FBAR and FATCA are not optional. They are mandatory legal obligations that exist entirely independent of your tax liability. The penalty regime — particularly for FBAR willful violations — is severe enough to wipe out an account. The Streamlined Foreign Offshore Procedure provides a legitimate, penalty-free path for non-willful non-filers, and the mechanics of both filings are genuinely manageable once you understand who files what, where, and by when.

If you've been living abroad and haven't filed FBAR or Form 8938, fix it before the IRS contacts you. The SFOP window is open, the process is defined, and the cost of proactive compliance is a fraction of the cost of being discovered.

Disclaimer: This post is for general informational and educational purposes only and does not constitute legal, tax, or financial advice. Tax law is complex and fact-specific. Consult a qualified US tax professional or international tax attorney regarding your individual situation. IRS penalty amounts and thresholds are subject to change; verify current figures at irs.gov and fincen.gov before filing.