Here's the part nobody tells you when you open a bank account in your new country: the moment your foreign account balances cross $10,000 combined — even for a single day — you're legally required to report them to the US Treasury. Miss it, and the fine starts at $16,536. Get flagged as willful? The penalty is the greater of $165,353 or 50% of your account balance. Per account.

This isn't hypothetical. In 2021, a federal court ordered a Florida man to pay $2.72 million in FBAR penalties for non-willfully failing to report 272 foreign accounts. A 2023 Supreme Court decision reduced that — but only for non-willful cases, and only down to about $50,000. Willful violators still face penalties that can exceed the account balance itself.

Most expats stumble into this completely unaware. You moved abroad, you opened a local checking account, maybe a savings account at a foreign brokerage, and you're doing fine on taxes with the Foreign Earned Income Exclusion. The FBAR is an entirely different obligation — separate from your tax return, filed with a different federal agency, and carrying its own savage penalty structure.

What FBAR Actually Is (And Why It Exists)

FBAR stands for Report of Foreign Bank and Financial Accounts. It's technically FinCEN Form 114 — filed with the Financial Crimes Enforcement Network, not the IRS. Congress created it under the Bank Secrecy Act to track money flowing through foreign accounts, primarily targeting tax evasion, drug money, and offshore wealth hiding.

It caught on with financial criminals. But it also caught on with every expat who opened a checking account in Medellín, a trading account in Singapore, or a pension fund in the UK.

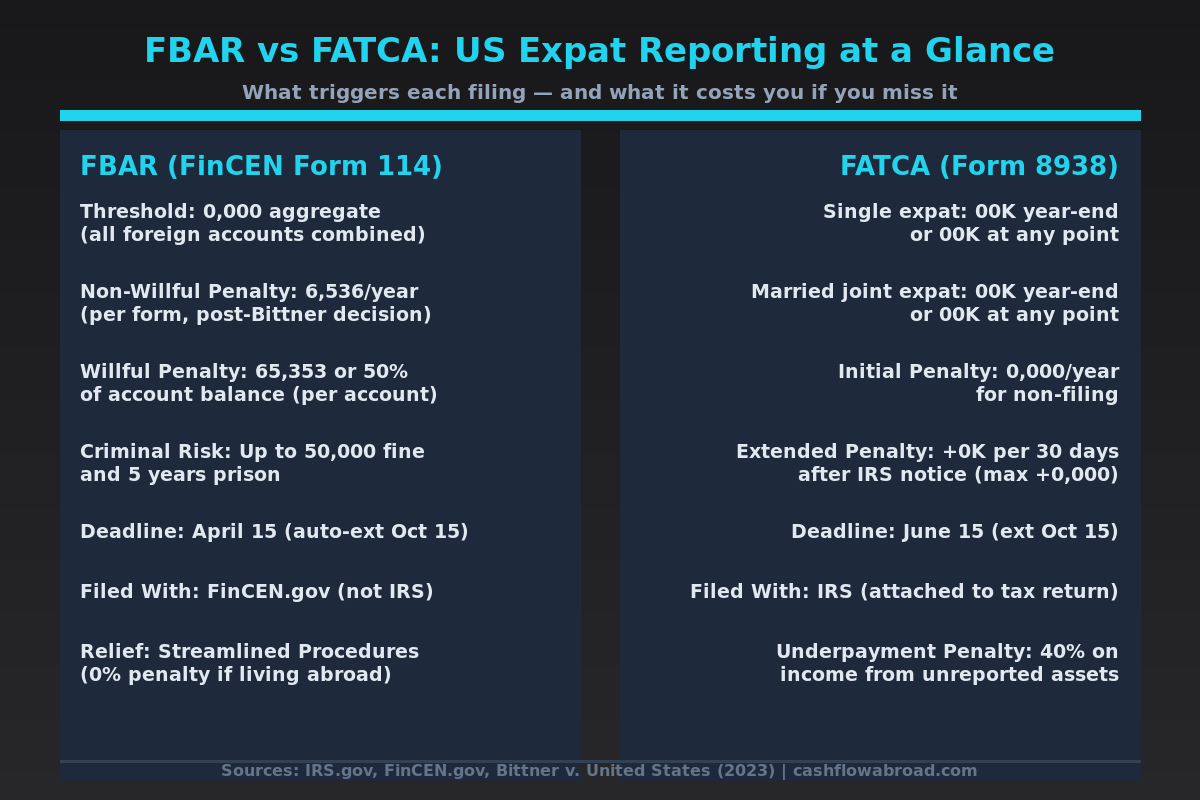

Who must file: Any US person (citizen, green card holder, certain resident aliens) who has a financial interest in or signature authority over foreign financial accounts with a combined maximum value exceeding $10,000 at any point during the calendar year. That $10,000 threshold is aggregate — across all accounts, in any currency, converted to USD at the year-end exchange rate.

Five accounts with $2,500 each? That's $12,500 aggregate. You must file. One account that briefly hit $10,001 in April but dropped to $3,000 by December? You must still file. The triggering event is the peak value during the year, not the year-end balance.

FBAR Deadlines and How to File

The annual FBAR deadline is April 15, with an automatic extension to October 15 — no request needed. You file electronically through FinCEN's BSA E-Filing System at bsaefiling.fincen.treas.gov, not through the IRS. There's no paper form option. There's no fee to file.

You report the account name, account number, bank name and address, maximum value during the year, and account type. You can have an authorized third party (tax preparer, attorney) file on your behalf with a completed Form 114a.

If you're behind on FBAR filings and your failure was non-willful, the Streamlined Foreign Offshore Procedures let you catch up by filing the last 6 years of FBARs, certifying non-willful behavior, and paying zero penalties. This is the most important escape hatch in expat tax compliance — more on this below.

FATCA and Form 8938: The Other Filing Nobody Mentions

FATCA — the Foreign Account Tax Compliance Act — is a separate law that created Form 8938, which is filed with the IRS as part of your tax return. Different threshold. Different form. Different consequences. And you may be required to file both.

The thresholds for expats living abroad are meaningfully higher than for US residents:

| Filing Status | Year-End Balance Threshold | Any-Point-During-Year Threshold |

|---|---|---|

| Single (living abroad) | $200,000 | $300,000 |

| Married Filing Jointly (living abroad) | $400,000 | $600,000 |

| Single (US resident) | $50,000 | $75,000 |

| Married Filing Jointly (US resident) | $100,000 | $150,000 |

Form 8938 covers a broader range of assets than FBAR — not just bank accounts but foreign stocks, foreign partnerships, foreign trusts, and certain foreign insurance contracts. The penalties for non-compliance start at $10,000 per year and escalate by $10,000 per 30 days after IRS notification (capped at an additional $50,000). An unreported foreign asset also carries a 40% understatement penalty on any underpaid tax tied to that asset.

FBAR vs FATCA: The Key Differences

| FBAR (FinCEN Form 114) | FATCA (Form 8938) | |

|---|---|---|

| Filed with | FinCEN (Treasury Dept) | IRS (attached to Form 1040) |

| Threshold (expats) | $10,000 aggregate | $200K–$300K (single) |

| Assets covered | Foreign bank/financial accounts | Broader — stocks, partnerships, trusts |

| Base penalty | $16,536/year (non-willful) | $10,000/year |

| Max civil penalty | $165,353+ or 50% balance (willful) | $60,000 (escalating) |

| Criminal exposure | Yes — up to 5–10 years prison | Typically civil only |

| Deadline | April 15 (auto-ext Oct 15) | June 15 (ext Oct 15) |

| Overlap required | Often required alongside Form 8938 | Often required alongside FBAR |

Filing one does not satisfy the other. If you have $250,000 in foreign accounts as a single expat, you likely need to file both. The IRS has confirmed this explicitly.

The Penalty Ladder: From Annoying to Devastating

FBAR penalties operate on a spectrum based on intent.

Non-Willful: The Most Common Case

Non-willful violations are failures to file due to negligence, oversight, or not knowing the rule existed. Thanks to the 2023 Supreme Court decision in Bittner v. United States, non-willful FBAR penalties are now capped at $16,536 per form per year — not per account. This was a significant taxpayer win.

The case involved Alexandru Bittner, a Romanian-American businessman who failed to report 272 foreign accounts over five years. The IRS originally assessed $2.72 million using a per-account calculation. The Supreme Court ruled 5-4 that the penalty applies per annual form, not per account. His liability dropped to approximately $50,000–$60,000.

This matters enormously for expats with multiple accounts. Before Bittner, having 10 accounts in one year could theoretically mean $165,360 in non-willful penalties for a single missed filing year. Now, it's a maximum of $16,536 regardless of how many accounts were unreported.

Willful: The Devastating Tier

If the IRS determines you knew about the FBAR requirement and still didn't file — or were "willfully blind" to it — you're in willful territory. The penalty: the greater of $165,353 or 50% of the highest account balance during the year. Per account. Per year.

Run the math. A $400,000 balance in a single account: $200,000 penalty for one year of willful non-filing. Repeat that over five years of auditable history and you're looking at a seven-figure liability the government can pursue with liens and levies — even after you've paid any underlying tax.

Courts have found willful violations where taxpayers checked "no" on Schedule B's foreign account question, moved money specifically to avoid crossing reporting thresholds, or ignored explicit advice from a tax professional that they needed to report.

Criminal: The Rare but Real Ceiling

Willful failure to file FBAR can be prosecuted as a federal crime carrying up to $250,000 in fines and 5 years in prison. If tied to other criminal activity — fraud, money laundering — that escalates to $500,000 and 10 years. The DOJ doesn't pursue this often. It pursues it when the numbers are large enough to warrant the attention.

The Escape Hatch: Streamlined Foreign Offshore Procedures

If you're behind on FBARs and it's genuinely non-willful, the IRS offers a way out. The Streamlined Foreign Offshore Procedures (SFOP) are available to US taxpayers living outside the US for at least 330 days in one of the last three tax years.

Under SFOP you file:

- The last 3 years of amended or delinquent tax returns

- The last 6 years of FBARs

- A certification statement confirming non-willful conduct

The penalty: zero. No accuracy penalty, no delinquency penalty, no FBAR penalty. This is the most favorable compliance program the IRS offers to anyone. The catch: you must genuinely qualify as non-willful, and certifying otherwise is a federal crime. An expat-specialized CPA can help you assess whether your situation qualifies before you submit anything.

For US residents (not living abroad), the Streamlined Domestic Offshore Procedures carry a 5% miscellaneous penalty — still dramatically better than standard FBAR penalties, but not free.

Crypto, Foreign Exchanges, and FBAR

Whether cryptocurrency held on a foreign exchange triggers FBAR filing is still an evolving area. As of the 2025 tax year, FinCEN has not formally required crypto held directly on blockchain addresses to be reported on FBAR. However, cryptocurrency held on foreign exchanges — Binance, OKX, foreign-entity Kraken accounts — is increasingly treated by practitioners as a reportable foreign financial account.

The safest approach: report foreign exchange-held crypto on your FBAR and Form 8938 if the aggregate value crosses the relevant threshold. The cost of voluntary disclosure is zero. The cost of getting it wrong is not. If you're tracking crypto across exchanges, tools like CoinTracking can generate the records you need to calculate peak balances across foreign platforms for accurate FBAR reporting.

For a deeper dive into crypto-specific reporting, see the US expat crypto tax guide.

FBAR-Smart Banking Setup for Expats

The goal isn't to avoid having foreign accounts — that's impractical when you live abroad. The goal is to have them, know you have them, and report them correctly.

Keep your US banking infrastructure intact. Charles Schwab International is the go-to for expats: no foreign transaction fees, free ATM withdrawals worldwide, and a clean US account that doesn't trigger FBAR reporting. Maintain a US address using a service like Traveling Mailbox — a real US street address (50+ cities) with mail scanning and check deposits for $15/month. Without a legitimate US address, many US banks will close your account when they discover you're living abroad, and the IRS needs a US address for all correspondence.

For US business banking, Mercury is a US bank account — it doesn't trigger FBAR at all. Foreign accounts used for business payments should be tracked carefully and reported. They're exactly what auditors look for.

More on structuring this correctly in the US expat banking guide and the virtual mailbox expat guide.

Five Mistakes That Get Expats into FBAR Trouble

- Assuming "I owe no tax, so I don't need to report." FBAR is a reporting requirement, not a tax. You can have zero US tax liability under the FEIE and still be required to file an FBAR. These are completely separate obligations enforced by different agencies.

- Counting the threshold per account. The $10,000 trigger is aggregate. $5,000 in each of three accounts = $15,000 aggregate = FBAR required. There's no minimum per-account floor.

- Forgetting signature-authority accounts. If your employer's foreign subsidiary has a bank account you have authority to move money in — even if you own nothing — you likely have FBAR exposure. Corporate treasurers working abroad get hit by this constantly.

- Missing the foreign pension. UK NEST, Australian Superannuation, Canadian RRSP — employer-sponsored foreign pension plans frequently trigger FBAR. Whether they require a simplified $1 valuation or detailed disclosure depends on plan structure. This is a common gap even among expats with US tax preparers who lack international specialization.

- Thinking the IRS doesn't know. Under FATCA, foreign financial institutions report US account holders to the IRS automatically. The global data-sharing infrastructure is now comprehensive enough that the IRS likely knows about your accounts before you file. Voluntary disclosure always produces better outcomes than being caught.

FBAR Is One Piece of a Bigger Disclosure Picture

FBAR and Form 8938 are the most commonly required foreign asset disclosures, but not the only ones. Owning 10%+ of a foreign corporation adds Form 5471. Receiving a foreign gift above $100,000 requires Form 3520. Benefiting from a foreign trust requires Form 3520-A. Owning a foreign partnership triggers Form 8865.

The system was designed to make offshore wealth hiding maximally difficult. The side effect: expats living completely normal financial lives in their adopted countries face a paperwork burden that their local-resident neighbors never encounter. The PFIC rules are another notorious example — owning a foreign mutual fund creates a tax reporting nightmare most expats don't discover until they try to sell.

Navigating this well requires a CPA who specializes in expat taxation, not just any US preparer. The cost differential between a general preparer and an expat specialist is typically $500–$1,500 per year. The cost of getting it wrong starts at $10,000 and climbs from there.

Bottom Line

FBAR is arguably the most dangerous compliance gap for US expats — not because the rules are hidden, but because most people assume it's an extension of their tax return. It isn't. It's a separate filing, with a different agency, a different deadline, and a penalty schedule that survives a zero-tax bill entirely intact.

If you're current: file annually through FinCEN's BSA E-Filing portal, track your foreign account peak values during the year, and keep records. If you're behind: the Streamlined Foreign Offshore Procedures exist precisely for you — and they carry zero penalty if you qualify. The window to act before the IRS finds you first is open now. It won't be indefinitely.

This post is for informational purposes only and does not constitute tax, legal, or financial advice. FBAR and FATCA rules are complex and fact-specific. Penalty amounts are adjusted annually for inflation. Consult a qualified expat tax professional for guidance on your individual situation.