There are roughly 9 million US citizens living outside the United States. The IRS estimates only about 1.5 million of them file taxes from abroad each year. The other 7.5 million are somewhere on a spectrum between genuinely not required to file and one IRS notice away from a very bad week.

The forms that catch the most people off guard aren't even tax returns. They're informational reports — FBAR and FATCA — and missing them can trigger penalties starting at $10,000 per violation even if you owe zero in actual taxes. You don't have to be hiding money. You just have to have a foreign bank account and not know this form exists.

This guide covers everything you actually need to know: what each form covers, exact thresholds, what the penalties look like in practice, and what to do if you've been non-compliant for years.

What Is FBAR (FinCEN 114)?

FBAR stands for Foreign Bank Account Report. The form is officially called FinCEN 114, named after the Financial Crimes Enforcement Network — the Treasury Department bureau that collects it. It has nothing to do with the IRS. You don't file it with your tax return. You file it separately, electronically, through the FinCEN BSA E-Filing System.

The trigger is simple: if the aggregate balance of all your foreign financial accounts exceeded $10,000 at any point during the calendar year, you must file. That's not $10,000 per account — it's a combined total across every account. If you have three accounts that each hold $4,000, that's $12,000 combined and you must file, even though no single account broke the threshold.

"Foreign financial accounts" is broad. It includes:

- Foreign checking and savings accounts

- Foreign brokerage and securities accounts

- Foreign mutual funds and retirement accounts (UK ISAs, Canadian RRSPs, Australian Superannuation)

- Foreign life insurance policies with cash surrender value

- Any account where you have signature authority — even accounts you don't own, such as an employer's account you're authorized to access

That last point trips up a lot of expats working for foreign companies. You may be required to file an FBAR for accounts you don't own a single dollar of.

What Is FATCA (Form 8938)?

FATCA — the Foreign Account Tax Compliance Act — is a law passed in 2010 that created Form 8938. Unlike FBAR, Form 8938 is filed directly with your federal tax return (Form 1040) and is administered by the IRS. It covers a broader category of assets, but at much higher thresholds.

Filing thresholds for US expats living outside the US:

| Filing Status | Year-End Value | At Any Point During Year |

|---|---|---|

| Single / Married Filing Separately | Over $200,000 | Over $300,000 |

| Married Filing Jointly | Over $400,000 | Over $600,000 |

These are significantly higher than the thresholds for US residents ($50,000 / $75,000 for single filers), which means many expats with modest foreign savings won't need to file Form 8938 — but almost certainly will need to file FBAR.

Form 8938 covers more than just bank accounts. It captures:

- Foreign stocks and securities held directly (not just through an account)

- Foreign partnership interests and trust holdings

- Foreign pensions and deferred compensation plans

- Foreign-issued annuities and life insurance contracts

- Interests in foreign corporations

- Cryptocurrency held at foreign exchanges

The key distinction: FBAR catches accounts you control or have authority over. Form 8938 catches assets you have a financial interest in — a wider net of asset types but limited to what you actually own.

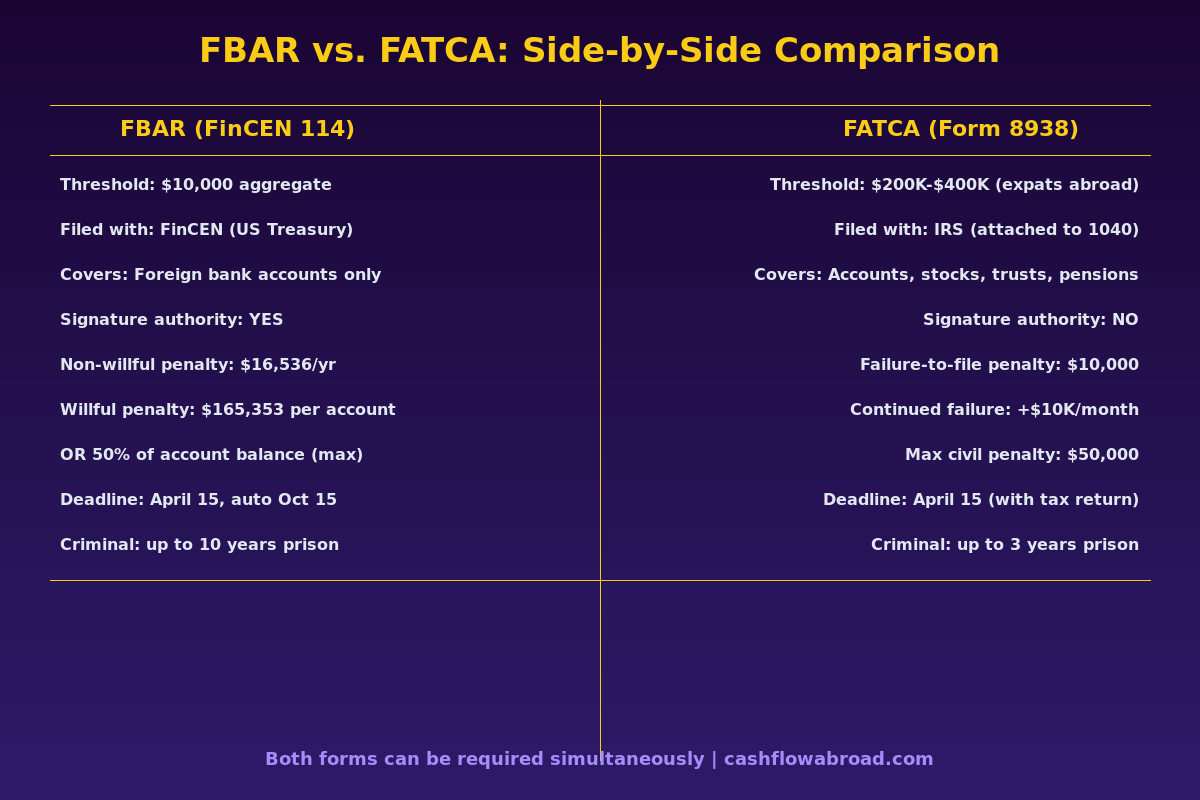

FBAR vs. FATCA: The Full Comparison

| Feature | FBAR (FinCEN 114) | FATCA (Form 8938) |

|---|---|---|

| Governing law | Bank Secrecy Act | Foreign Account Tax Compliance Act |

| Filed with | FinCEN (Treasury) — separately | IRS — with Form 1040 |

| Threshold | $10,000 aggregate (all filers) | $200K–$400K+ (expats abroad) |

| Asset types | Foreign bank/financial accounts | Accounts + stocks, trusts, pensions, partnerships |

| Signature authority | Yes — report accounts you control | No — only what you own |

| Non-willful penalty | Up to $16,536 per violation | $10,000 flat |

| Willful penalty | $165,353 or 50% of balance (whichever is greater) | Up to $50,000 (continued failure) |

| Criminal exposure | Up to 10 years prison | Up to 3 years prison |

| Primary deadline | April 15 (auto extension to Oct 15) | April 15 (with tax return) |

The critical thing to understand: you can be required to file both. A foreign bank account above $10,000 triggers FBAR. If your total foreign asset value also crosses the Form 8938 threshold, you file that too. Two separate forms, two separate systems, two separate penalty regimes.

For more on US expat tax obligations broadly, see our complete US expat banking and taxes guide.

The Penalties: What They Actually Look Like

The word "penalty" in an IRS context can mean anything from a slap on the wrist to a financial catastrophe. With FBAR, it leans toward catastrophe if the IRS decides your failure was willful.

Non-Willful FBAR Penalties

Non-willful means you didn't know you had to file — you weren't hiding anything, you just weren't aware of the requirement. The penalty is up to $16,536 per violation (inflation-adjusted for 2025). "Per violation" typically means per account, per year.

If you had two foreign accounts for three years and didn't file, that's potentially six violations — up to $99,216 in penalties, on accounts where you may owe zero in additional taxes. The IRS has discretion to assess less, but has not historically been generous with that discretion.

Willful FBAR Penalties

For willful violations, the penalty is the greater of $165,353 or 50% of the account balance at the time of the violation. Per account. Per year. The math can get surreal quickly: a $500,000 account held for three years where you "willfully" didn't file FBAR could theoretically generate penalties exceeding the account value itself.

In January 2026, the US Court of Appeals for the Second Circuit ruled that "reckless disregard" of FBAR requirements qualifies as a willful violation — now applicable in nearly every US jurisdiction. This ruling matters because it closes the "I didn't know it existed" defense for taxpayers who should have known. If you're a US citizen abroad with foreign accounts and a tax professional, reckless disregard is a real legal risk.

FATCA Penalties

FATCA penalties are more predictable. Failure to file Form 8938 when required starts at a flat $10,000. After the IRS notifies you of the failure, it escalates by another $10,000 per month, up to a maximum civil penalty of $50,000. Additionally, any tax underpayment attributable to undisclosed foreign assets carries a 40% accuracy penalty, versus the standard 20%.

The Amnesty Program You Should Know About

If you're reading this and realizing you should have been filing FBARs for years, there's a legitimate path back into compliance without facing the full penalty regime. It's called the Streamlined Foreign Offshore Procedure (SFOP).

Here's how it works: if you were genuinely non-willful — you didn't know about the requirement, not that you knew and chose not to file — you can come into compliance by filing 3 years of delinquent tax returns and 6 years of delinquent FBARs, paying any back taxes owed plus interest. The offshore version (for expats who were physically outside the US for at least 330 days in at least one of those three years) carries a 0% offshore penalty.

That's not a typo. Zero. You pay what you owe in taxes, plus interest, and get current on your FBARs — and the IRS waives all the penalties. Compare that to the willful penalty regime and the value of this program is enormous.

The catch: you must certify under penalty of perjury that your failure was non-willful. If the IRS disagrees — or if you were actually hiding the accounts and certify otherwise — you've just added a perjury exposure to your problems. The January 2026 "reckless disregard" ruling also means the bar for what constitutes non-willful behavior is narrowing.

Eligibility requires that the IRS has not already opened an examination of your returns. Once they've started looking, the streamlined program is closed to you.

The Accounts That Catch People Off Guard

Foreign Retirement Accounts

A British ISA, a Canadian RRSP, an Australian Superannuation fund — these typically require FBAR reporting once they cross the $10,000 aggregate threshold. They may also trigger Form 8938 and, in some cases, additional forms (Form 3520 for foreign trusts, Form 8621 for PFICs). The PFIC rules alone deserve a full post — see our expat investing playbook for details on why buying foreign mutual funds through a foreign account can create a serious tax headache.

Employer Accounts with Signature Authority

If you're an employee of a foreign company and have authority to transact on company accounts, those accounts count toward your FBAR aggregate threshold even though you don't own the money. If those accounts collectively hold more than $10,000 at any point, you're supposed to file — even though the funds belong to your employer. Many expat employees at foreign firms have no idea this applies to them.

Crypto on Foreign Exchanges

As of 2024, cryptocurrency held on foreign exchanges isn't explicitly covered by current FBAR form instructions, but Form 8938 specifically includes "any financial account maintained by a foreign financial institution" — and foreign crypto exchanges increasingly qualify. FinCEN has proposed expanding FBAR to include crypto and enforcement is tightening. If you're holding crypto on a foreign exchange, assume both reporting obligations apply or will apply soon. A tool like CoinTracking can help you maintain accurate records across exchanges for exactly this purpose.

How to Actually File Each Form

Filing FBAR (FinCEN 114)

- Go to the BSA E-Filing System at bsaefiling.fincen.treas.gov

- File FinCEN Form 114 electronically — there is no paper option

- Deadline is April 15, with an automatic extension to October 15 (no separate request needed)

- Report each foreign account: account number, institution name, country, maximum value during the year

No payment accompanies the FBAR. It's purely informational. If you're late, filing voluntarily and explaining your circumstances is far better than waiting to be discovered.

Filing Form 8938 (FATCA)

- Complete Form 8938 and attach it to your Form 1040

- Report accounts and foreign assets above the applicable threshold

- For each asset: value at year-end, maximum value during the year, income generated, and whether it's already reported elsewhere

- Same deadline as your tax return: April 15, or June 15 for expats abroad, with extensions available to October 15

Staying Compliant: Four Practical Moves

Track your high-water marks quarterly. You need the maximum value of each account during the year — not just the year-end balance. Most banking apps show historical balances, but building a simple quarterly snapshot saves a headache at tax time. A spreadsheet with four snapshots per year per account is sufficient.

Maintain a US address. The IRS, FinCEN, and your US financial institutions all need a current domestic address. Expats who lose their US address often lose access to US banking and investment accounts. A service like Traveling Mailbox gives you a real US street address in 50+ cities with mail scanning and check deposit capability for around $15/month. It's one of the lowest-friction ways to maintain IRS compliance and US banking access while abroad — the site owner uses it personally. For more on this topic, see our complete virtual mailbox guide for expats.

Use a US bank that doesn't close expat accounts. Many US banks quietly close accounts held by customers with foreign addresses. Mercury is built for remote and global businesses and doesn't penalize you for operating abroad. For individual expats, Charles Schwab's international checking account remains the standard — no foreign transaction fees, free ATM withdrawals worldwide, and no minimum balance.

File FBAR even if you don't owe taxes. Your FBAR obligation is completely separate from your income tax obligation. If your income is low enough that you owe nothing, you might think you're off the hook — but if your foreign account balances crossed $10,000 at any point, FBAR is still required. The two forms operate on parallel tracks. For a full picture of how to legally reduce your actual tax bill as an expat, see our breakdown of the Foreign Earned Income Exclusion.

Why FATCA Changed Everything for Enforcement

Before FATCA, the IRS had essentially zero visibility into foreign bank accounts. FATCA fixed this by requiring foreign financial institutions to report US account holders directly to the IRS — or face a 30% withholding penalty on US-sourced income. Foreign banks chose to comply rather than lose access to US markets.

The result: as of 2023, foreign financial institutions have reported over 30 million accounts held by US persons to the IRS. The IRS now cross-references this database against filed FBARs and 8938s. The era of invisible offshore accounts is over. The broader data-sharing expansion — including the Common Reporting Standard and AI-driven audit tools — is detailed in our post on why expat invisibility is ending.

The Bottom Line

FBAR and FATCA aren't complicated, but they're easy to miss if nobody told you they existed. The $10,000 FBAR threshold means most expats with any meaningful foreign savings have to file it. The Streamlined Foreign Offshore Procedure means there's a real amnesty path if you've fallen behind — but that window is narrowing as the IRS's data-matching gets better and courts expand the definition of willful non-compliance.

File the forms, maintain a US address, keep a US bank account, and log your account balances quarterly. That's the whole job.

Financial Disclaimer: This article is for general informational purposes only and does not constitute tax, legal, or financial advice. FBAR and FATCA rules are complex and fact-specific; penalties and thresholds are subject to change and inflation adjustment. Consult a qualified US expat tax professional — such as a CPA or tax attorney with international experience — before making decisions about your compliance obligations or filing strategy. Streamlined procedure eligibility and outcomes vary based on individual circumstances.