FATCA vs. GDPR: Why US Expats Lose European Banks

Belgium ordered FATCA data transfers to stop. European banks face a legal catch-22. Here is what US expats in Europe need to know and do now.

Belgium declared FATCA illegal under GDPR. Now EU banks face a catch-22. Here is what US expats need to know about European banking in 2026.

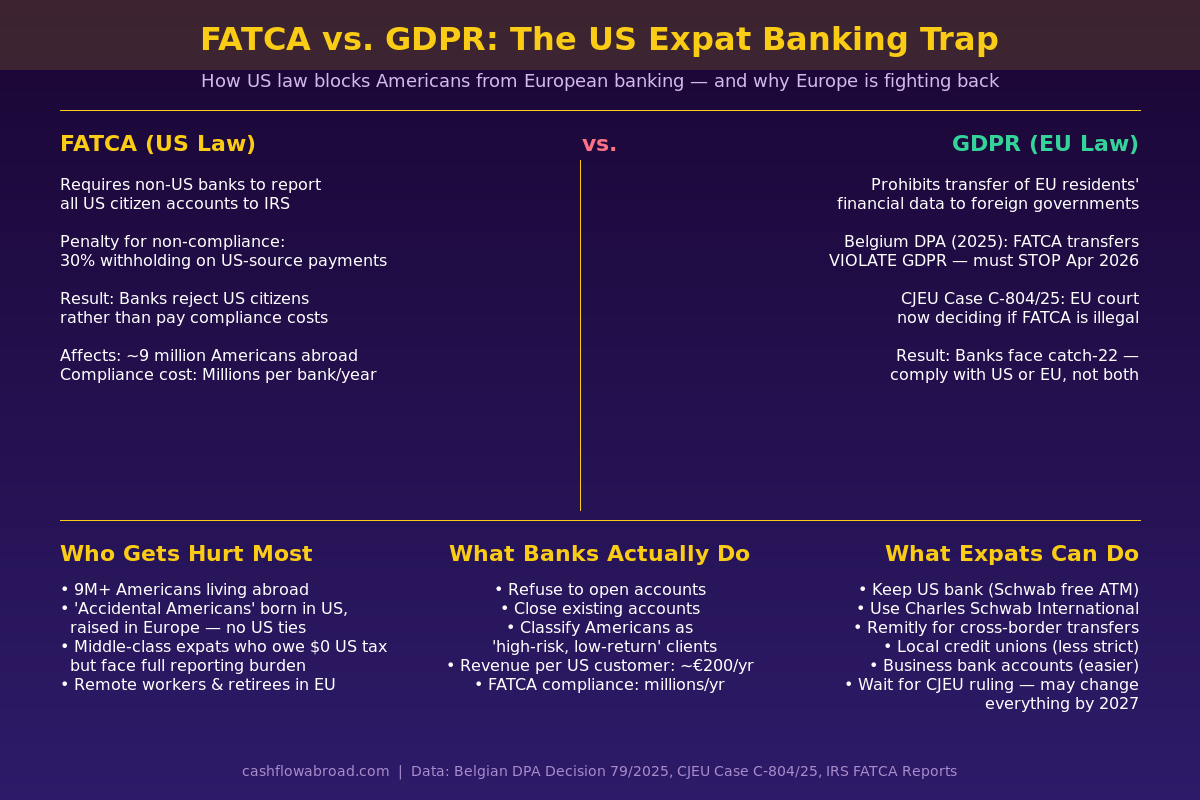

On April 24, 2026, European banks were legally ordered to stop transferring US citizens' financial data to the IRS — by Belgium's own data protection authority. The catch: if they actually comply, the US government can hit them with a 30% withholding penalty on all their US-source payments. That's not a regulatory gray area. That's a legal trap, and roughly 9 million Americans living abroad are caught in the middle of it.

FATCA — the Foreign Account Tax Compliance Act — has been quietly reshaping the financial lives of US expats since 2014. But a series of rulings in Europe from 2025 into 2026 have turned a slow-burning problem into an acute crisis. If you hold a US passport and live in Europe, you need to understand what's happening, why European banks are increasingly refusing to serve you, and what your practical options are right now.

What FATCA Actually Requires

FATCA was signed into law in 2010 as part of the HIRE Act, sold to Congress as a weapon against offshore tax evasion by wealthy Americans hiding money in Swiss accounts. The mechanism: every foreign financial institution (FFI) worldwide must identify US account holders, collect their social security numbers, and report account balances and income to the IRS annually. Non-compliant institutions face a 30% withholding penalty on all US-source payments they receive — effectively severing them from dollar-denominated markets.

The law covers essentially every bank, brokerage, pension fund, and insurance company on earth. Over 110 countries have signed Intergovernmental Agreements (IGAs) to implement FATCA reporting, often making compliance a domestic legal obligation for their local banks.

The compliance cost is staggering. A mid-sized European bank spends several million euros per year on FATCA infrastructure — legal teams, reporting systems, KYC processes, and IRS liaison work. A typical American retail banking customer generates perhaps €200-400 in annual revenue. The math makes refusal the rational choice. Banks don't hate Americans; they just don't want to spend €3,000 in compliance overhead to earn €300 in revenue per customer.

The GDPR Collision: When Two Laws Can't Both Be Right

This is where the story gets genuinely novel. In 2025, Belgium's Data Protection Authority (DPA) issued Decision 79/2025, ruling that transfers of Belgian residents' banking data to the IRS under FATCA violate the EU's General Data Protection Regulation. Specifically:

- Purpose limitation: GDPR requires that personal data only be used for the purpose for which it was collected. Retail banking data was collected for banking services — not bulk transfer to foreign governments.

- Necessity and proportionality: The mass transfer of data on all US citizens, including those who owe zero US tax, fails the proportionality test.

- Chapter V transfer rules: GDPR imposes strict conditions on transferring EU residents' data outside the EU. The Belgium-US FATCA IGA predates GDPR and was never assessed for compliance with it.

Belgium's federal tax authority was ordered to stop FATCA transfers by April 24, 2026. Then on December 10, 2025, the case was escalated to the EU Court of Justice (CJEU) as Case C-804/25. Thirteen preliminary questions are now before Europe's highest court, with a ruling potentially 18-24 months away. The central question: can a country's legal obligation under a US intergovernmental agreement override GDPR, or does GDPR win?

European banks are now in a genuine legal catch-22. Comply with FATCA, and risk GDPR enforcement. Comply with GDPR, and face 30% US withholding. Neither choice is clean, and regulators in multiple EU member states are watching the Belgian case to decide their own positions.

Who Actually Gets Hurt: It's Not the Billionaires

FATCA was sold as a tool to catch billionaires hiding fortunes in Switzerland. The irony is brutal: the ultra-wealthy can afford expensive private banking relationships, compliance lawyers, and offshore structures that absorb the overhead. The people actually getting hurt are middle-class Americans abroad.

The Association of Accidental Americans drove much of the Belgian litigation. "Accidental Americans" are people born in the US who moved abroad as infants or children, have lived their entire adult lives in Europe, hold European citizenship, and have zero practical connection to the United States — but are still subject to US citizenship-based taxation and FATCA reporting because the US never revoked their citizenship.

Consider a 45-year-old French national, born in New York to French parents who moved back when he was two years old. He has never worked in the US, has no US assets, and owes no US tax. But his French bank is legally required to report his account to the IRS. If he refuses to provide his Social Security number — which he may never have had — his bank may simply close his account. He is effectively unbanked in his own country because of a law he had no political representation to oppose.

The Actual Scale of the Problem

| Country | Estimated US Citizens | Known Banking Issues |

|---|---|---|

| Germany | ~350,000 | Deutsche Bank, Commerzbank both restrict US accounts |

| France | ~150,000 | BNP Paribas, Société Générale account closures reported |

| Netherlands | ~50,000 | ING and ABN AMRO refuse new US citizen accounts |

| Belgium | ~35,000 | KBC and Belfius restrict US citizen accounts — sparked the DPA case |

| Switzerland | ~40,000 | UBS historically problematic; FATCA triggered nationwide account reviews |

| UK | ~250,000 | Barclays, NatWest restrictions; UK applies FATCA independently of EU |

Total Americans abroad: approximately 9 million, with an estimated 4-5 million in countries that actively enforce FATCA. Surveys suggest 30-40% have faced at least one banking refusal or account closure.

The Hypocrisy the US Won't Acknowledge

Here's the fact almost no mainstream coverage of FATCA includes: the United States is not a participant in the OECD's Common Reporting Standard (CRS) — the global equivalent of FATCA that over 100 countries use to share financial information with each other.

FATCA was built on a premise of reciprocity. The US would receive data on its citizens abroad, and in exchange, share data on foreign nationals holding US accounts. In practice, US reciprocity under FATCA IGAs is severely limited. The US collects financial data on Americans worldwide. It shares almost nothing in return.

This asymmetry has not gone unnoticed. EU finance ministers have raised it repeatedly in diplomatic channels. The CJEU case may partially turn on it — if the US-EU information exchange is not genuinely reciprocal, the legal basis for the IGAs weakens considerably under GDPR's data transfer rules.

The US is one of only two countries on earth with citizenship-based taxation (the other is Eritrea). An American who moves to France and earns all income in France still owes US tax filings, FBAR reports on any foreign account over $10,000, and potentially US tax — though the Foreign Earned Income Exclusion and foreign tax credits usually reduce the actual US bill to zero. The compliance burden remains regardless. For a broader view of how global financial data sharing is closing in on expats, our piece on AI audits and the CARF data-sharing regime covers what's coming next.

What a CJEU Ruling Could Mean

If the Court of Justice of the European Union rules that FATCA-based data transfers violate GDPR — which is legally plausible though uncertain — the consequences cascade:

- EU banks would be legally prohibited from FATCA reporting for EU-resident clients

- The US would face a choice: renegotiate FATCA IGAs with all 27 EU member states, or impose the 30% withholding penalty on European banks — effectively declaring financial war on its largest trading partner

- Other GDPR jurisdictions (EEA, UK post-Brexit, countries with adequacy decisions) would likely follow the EU's lead

- A legislative fix would require Congress to act, which moves slowly even without partisan gridlock

More likely than a clean ruling: a pragmatic political settlement that modifies the FATCA framework — perhaps raising the reporting threshold from $50,000, limiting reporting to accounts with genuine US-source income, or building in stronger reciprocity. None of that helps today. But the legal architecture is shifting.

Practical Banking Options for US Expats in Europe Right Now

The legal situation is in flux. You still need a bank account today. Here's what actually works in 2026:

1. Keep a Strong US Bank as Your Core Account

Charles Schwab's international account remains the gold standard for US expats worldwide. Zero foreign transaction fees, unlimited ATM fee reimbursements globally, and no minimum balance — it functions as a de facto international debit card anywhere with an ATM. For expats who primarily spend locally and don't need a European IBAN for salary deposits, Schwab's checking account handles 90% of daily financial life. The critical move: open it before you leave the US. Schwab's online application requires a US address.

For business banking, Mercury is a US-based fintech bank built for remote companies and entrepreneurs. Opens online in minutes, no fees, supports international wire transfers — essential if your income comes from international clients. Our full US expat banking guide covers the complete comparison.

2. Cross-Border Payments Without a European IBAN

If you need to pay European rent, utility bills, or local expenses but can't get a local account, Remitly transfers to bank accounts across Europe from your US account at competitive rates — useful when your landlord requires a local IBAN but you're banking in dollars. See the full fee comparison in our international transfer guide.

3. Protect Your US Banking Relationships With a US Address

Most US banks will quietly close accounts if they discover you've permanently relocated abroad without a US address. A Traveling Mailbox — a real US street address in 50+ cities with mail scanning and check deposit — keeps your US banking relationships intact, preserves your IRS correspondence address, and maintains state domicile for licensing and residency purposes. At $15/month, it's the single most cost-effective tool in an expat's banking setup. See our detailed virtual mailbox guide for full setup instructions.

4. Local European Accounts: Where to Actually Try

Not all European banks apply FATCA restrictions equally. Smaller credit unions and regional cooperative banks — Germany's Volksbanken and Raiffeisenbanken, France's Crédit Mutuel, Dutch cooperative banks — sometimes accept US citizens, especially with a residence permit and local employment contract. Business accounts (Geschäftskonto, compte professionnel) often have fewer restrictions than personal accounts because the revenue-to-compliance ratio is better.

Eastern European banks — particularly in the Czech Republic, Poland, and Romania — are generally less aggressive about retail FATCA enforcement. Some Baltic banks also remain accessible. These aren't permanent solutions given regulatory direction of travel, but they're workable now.

| Option | EU IBAN | Accessible to US Citizens | Best Use Case |

|---|---|---|---|

| Charles Schwab International | No | Yes — open before leaving US | Daily ATM, travel spending |

| Mercury (US business banking) | No | Yes | Business income, international wires |

| Local EU credit union | Yes | Sometimes — needs residency proof | Salary deposit, local rent payments |

| Eastern EU bank | Yes | More often accessible | EU IBAN with fewer restrictions |

| EU neobank | Yes | Usually yes | Supplementary account, day-to-day |

| US bank + Remitly | No | Yes | Cross-border rent/bill payments |

Your Banking Action Plan

- Open Schwab International before you relocate. Seriously — this is the one you can't fix after the fact. It's the best expat debit card in existence and requires a US address to open.

- Activate a virtual US mailbox to preserve your US address and all associated banking relationships.

- Try regional and cooperative banks first when you need a local IBAN in Europe — not the large national institutions with blanket US exclusion policies.

- Consider a business account if you have any self-employment income — business banking compliance is assessed differently from retail accounts.

- Document any banking refusals. The Association of Accidental Americans, American Citizens Abroad, and Democrats Abroad collect these cases for legal and legislative advocacy. Your documentation matters.

- Monitor CJEU Case C-804/25. A ruling against FATCA data transfers would be the biggest shift in expat banking rules in a decade.

The Bigger Picture

FATCA was written to catch tax cheats. What it created is a two-tier financial system: one for Americans who stay home, and one for Americans abroad who are increasingly treated as compliance liabilities by the world's banks. The Belgian DPA ruling and CJEU case are the first serious legal challenges to this architecture from a jurisdiction powerful enough to force a response.

Whether the outcome is a court ruling that upends FATCA, a diplomatic renegotiation that fixes the worst of its excesses, or a prolonged standoff with no near-term resolution, one thing is clear: the assumption that US citizenship is universally compatible with normal financial life in Europe no longer holds. The expats who navigate this best are the ones who built a resilient banking stack before the problem hit them — not after.

Financial disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. FATCA, GDPR, and international banking regulations are complex, jurisdiction-specific, and subject to change. Consult a qualified US tax attorney or international financial advisor for guidance specific to your situation. Some links in this article are affiliate links — we may earn a commission at no cost to you.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 8, 2026

Expat Tax & FinanceMay 8, 2026

Why Foreign Banks Refuse American Expats (And What to Do)

FATCA costs banks $16,600 per American account. Learn why foreign banks refuse US expats and which banking solutions actually work abroad.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.

Expat Tax & FinanceMay 7, 2026

Expat Tax & FinanceMay 7, 2026

Charles Schwab for Expats: Bank Free in Any Country

Stop losing $2,400/year to hidden banking fees. Charles Schwab reimburses all ATM fees worldwide with zero foreign transaction fees for expats.