Expat RSUs: The Double Tax Trap Tech Workers Don't See Coming

A software engineer at a major tech company moves to Portugal in January. In November, 200 RSUs vest — worth $180,000 at market price.

A software engineer at a major tech company moves to Portugal in January. In November, 200 RSUs vest — worth $180,000 at market price.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

A software engineer at a major tech company moves to Portugal in January. In November, 200 RSUs vest — worth $180,000 at market price. She gets a W-2 in the spring showing $180,000 in ordinary income, with US federal tax withheld on the full amount. Portugal also taxes a portion. She owes tax in two countries on income that hit her account once. Nobody at HR warned her. Her tax bill is $47,000 more than she expected.

This is not a rare edge case. Every American expat who carries unvested equity across a border faces some version of this problem, and most don't find out until the W-2 lands. The IRS has specific rules for how it sources RSU income across countries — rules that interact badly with FEIE, foreign tax credits, and employer withholding. Here's exactly how it works.

How RSUs and Stock Options Work (Briefly)

A restricted stock unit (RSU) is a promise from your employer to deliver shares once you've hit a vesting milestone — usually time-based, sometimes performance-based. When RSUs vest, the fair market value of those shares is treated as ordinary income, reported on your W-2, and subject to federal income tax plus FICA at ordinary income rates. You don't choose when to recognize the income — vesting is the trigger.

Stock options come in two flavors:

- Non-qualified stock options (NSOs/NQSOs): Taxed as ordinary income at exercise — the spread between exercise price and current FMV goes on your W-2.

- Incentive stock options (ISOs): No regular income tax at exercise. You can trigger alternative minimum tax (AMT) at exercise, and you only pay capital gains rates if you hold the shares long enough. ISOs have a different (and worse) international problem.

Restricted stock awards (RSAs) work differently — the 83(b) election is available and income is recognized at grant, not vesting. Most tech companies use RSUs, not RSAs, so the rest of this guide focuses there.

The IRS Grant-to-Vest Rule: Where the Double Tax Comes From

When you cross a border mid-vesting-period, the IRS uses the grant-to-vest allocation method to divide your RSU income between US-source and foreign-source. The formula: for each RSU batch, calculate what percentage of the vesting period you spent working in the United States versus abroad. That percentage determines how much income the IRS treats as US-source.

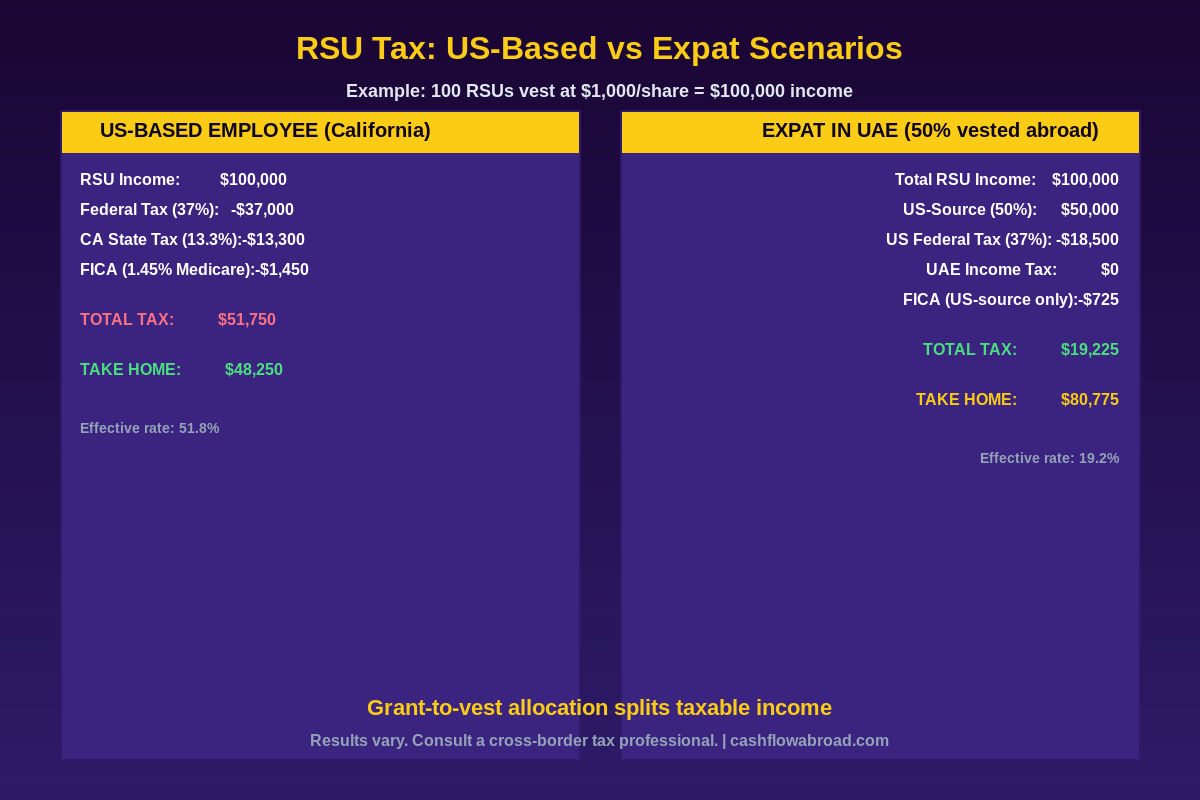

Example: You receive an RSU grant in January 2023 with a 4-year cliff vest (vests January 2027). You move abroad in January 2025 — exactly halfway through the vesting period. When the RSUs vest, 50% of the income is US-source and 50% is foreign-source under IRS rules.

If those 500 RSUs vest at $200/share ($100,000 total):

| Income Category | Amount | US Tax Treatment |

|---|---|---|

| US-source portion (50%) | $50,000 | Ordinary income — always taxable by US |

| Foreign-source portion (50%) | $50,000 | May qualify for FEIE or FTC (see below) |

| FICA (Social Security + Medicare) | Applies to US-source only | $50,000 x 7.65% = $3,825 |

Here's the critical trap: your employer's payroll system doesn't automatically apply this split. Most payroll departments withhold US federal income tax on the full $100,000, as if all income is US-source. You'll get a W-2 showing $100,000 in box 1, and you'll need Form 1116 or Form 2555 to address the foreign-source portion on your tax return. If you miss this, you overpay US taxes and potentially miss foreign tax credits that could offset your host-country liability.

FEIE and RSUs: It's Not as Clean as You Think

The Foreign Earned Income Exclusion lets qualifying expats exclude up to $132,900 (2026) in foreign earned income from US taxation. RSUs that vest while you're working abroad look like they should qualify — you're a US citizen working in a foreign country, and the income is compensation for services rendered abroad.

The problem is that only the foreign-source portion of RSU income can potentially be excluded under FEIE. The US-source portion (determined by the grant-to-vest calculation) is always US-taxable, period. FEIE doesn't touch it.

Second problem: RSU income at vesting is classified as compensation income — earned income for FEIE purposes — but only the foreign-source slice. If you have a 4-year vest and spent 2 years in the US and 2 years abroad before vesting, only half qualifies for FEIE at all. Stack that against your regular salary (also claiming FEIE) and you may hit the exclusion limit before RSU income even enters the picture.

Third problem: if you elect FEIE and it covers the foreign-source RSU income, you cannot then take a Foreign Tax Credit on the same income. If your host country also taxes that portion, you've used FEIE to exclude income that would have generated a usable credit — and now you have foreign tax with no offset mechanism. For expats in high-tax countries (Germany, France, Netherlands), FTC often beats FEIE specifically because it preserves credits on RSU income. See the full breakdown on FEIE vs FTC strategy here.

The Foreign Tax Credit Strategy for RSU Income

The Foreign Tax Credit (Form 1116) lets you offset US taxes dollar-for-dollar with foreign taxes paid on the same income. For RSU-heavy expats in high-tax countries, this can eliminate most or all US liability on the foreign-source portion.

| Country | RSU Income | US Tax (Pre-FTC) | Foreign Tax Paid | Net US Tax |

|---|---|---|---|---|

| Germany (50% abroad) | $100,000 | $37,000 (37% on full amount) | ~$47,500 (Germany's ~47.5% top rate) | ~$0 (FTC wipes US liability) |

| UAE (50% abroad) | $100,000 | $18,500 (37% on $50K US-source) | $0 (no UAE income tax) | $18,500 (US-source always taxable) |

| Portugal (50% abroad) | $100,000 | $37,000 | ~$28,000 (Portugal 48% marginal) | ~$9,000-$14,000 after FTC |

| Singapore (50% abroad) | $100,000 | $37,000 | ~$11,000 (Singapore 22% max) | ~$26,000 (partial FTC offset) |

One more wrinkle: FTC carryovers. If your foreign taxes exceed US liability in a given year (common in high-tax countries), unused credits carry forward 10 years. Expats who repatriate and vest remaining shares on US soil can potentially use those accumulated credits to offset US tax. It requires tracking Form 1116 carryforward balances — most tax software handles it, but cross-border CPA oversight is essential.

ISOs Abroad: The AMT Trap Gets Worse

Incentive Stock Options are designed as a tax-advantaged vehicle — no ordinary income at exercise, long-term capital gains rates if you hold. But for expats, they behave strangely.

When you exercise ISOs abroad, the bargain element (FMV minus exercise price) triggers AMT even though it doesn't trigger regular income tax. If you're in a country that also taxes option income at exercise, you may owe foreign tax plus US AMT on the same spread — with no clean FTC mechanism because AMT calculations work differently from regular tax.

Equally dangerous: ISOs have a 90-day post-termination exercise window. Leave the company while abroad and fail to exercise within 90 days, and your unexercised ISOs automatically convert to NSOs — losing the preferential tax treatment entirely. Many expats miss this window during the chaos of an international move or job change.

For NSOs, the tax picture is simpler: the spread at exercise is ordinary income, subject to the grant-to-exercise allocation. The sourcing mechanics are identical to RSUs — your employer will likely withhold on the full spread regardless of where you worked.

The State Tax Ghost: California and New York Don't Let Go

California's Franchise Tax Board sources equity compensation income based on where you worked during the vesting period, including years you spent as a California resident before leaving. Live in California for two of your four vesting years, then leave — California can still claim 50% of your RSU income at vest, even if you haven't been there in years.

New York operates similarly, allocating stock option and RSU income based on workdays spent in the state during the relevant period. Both states audit aggressively and have the authority to garnish equity proceeds through broker cooperation.

The implication: leaving California or New York before RSUs vest doesn't release those states' claims on equity accrued while you lived there. You need to have been physically absent during the accrual period — and you need documentation to back it up. The guide on state domicile strategy covers how to make a clean break that holds up to audit.

The Employer Withholding Mess

Your company's payroll system is configured for US employees. When you move abroad and RSUs vest, payroll typically:

- Withholds US federal income tax on the full vest value — not just the US-source portion

- Withholds full FICA including Social Security, even though Social Security only applies to US-source income (or may be exempt under a totalization agreement)

- Does not apply the grant-to-vest allocation at the withholding stage

- Reports the full amount on a W-2 without documenting the sourcing split

This overwithholding generates a US refund when you file correctly — but you've floated a large interest-free loan to the IRS, and your host country may not credit the overwithholding against local liability. Correcting this requires proactive communication with your company's global mobility or equity team before any grants vest. Large tech companies sometimes have cross-border equity specialists; most don't.

Also: when shares are sold, the 1099-B from the brokerage typically shows the wrong cost basis. If your employer withheld taxes on the ordinary income at vest, your tax basis is the FMV on vest date — not zero. Using the default basis creates phantom capital gains. Verify the cost basis on every equity sale. For more on how expat brokerages handle reporting, see the expat investor playbook.

Strategic Timing: How to Reduce Your Exposure

The grant-to-vest allocation is locked by history — you can't retroactively change where you worked. But you can optimize around it:

Move early in the vesting period. The longer you work abroad relative to the grant date, the more income shifts to foreign-source. Move in year one of a four-year vest: 75% of income becomes foreign-source. Move in year three: only 25% does. Timing your relocation early in a new grant cycle dramatically changes the tax profile.

Choose FTC over FEIE for equity-heavy years. Switching requires a formal opt-out and a 5-year waiting period before you can switch back. But if a large vest falls in a high-tax country year, FTC can eliminate US liability while FEIE simply excludes income without generating usable credits. Model both scenarios before making the election.

Time NSO/ISO exercises strategically. Option exercises are discretionary — RSU vests are not. If moving to a low-tax country, exercising before you leave may produce less total tax than waiting for higher FMV abroad. If moving to a high-tax country with strong FTC, waiting may be more efficient.

Document your work location by day. The grant-to-vest calculation is based on workdays, not just calendar residency. US business travel during your foreign residency increases the US-source fraction. Keep payslips, travel records, and employer documentation confirming your primary work location across every vesting period.

For managing proceeds across borders, Charles Schwab International (free global ATMs, no foreign transaction fees) handles expat equity accounts cleanly, and Mercury works for US business banking if you're running an entity alongside employment. Keep a Traveling Mailbox US address — Traveling Mailbox ($15/month) maintains a real US street address for brokerage accounts, IRS notices, and equity plan correspondence.

Tax Treaties: They Help, But Not as Much as You'd Think

The US has income tax treaties with about 68 countries. Most include provisions for employment income — and RSU income is generally treated as employment income under treaties. The savings clause (Article 15 or equivalent) determines which country has primary taxing rights based on where services were performed.

Catch: most US tax treaties don't address equity compensation explicitly. Countries interpret "where services were performed" differently for vested stock. Germany follows a strict day-count approach similar to the IRS grant-to-vest method. The UK uses HMRC's own sourcing methodology. France has separate rules for qualified versus non-qualified equity plans. You cannot assume the US treaty definition maps cleanly to your host country's calculation.

In practice, both countries may claim overlapping portions of RSU income even with a treaty. FTC is your safety valve — but the credits are limited to taxes on the same income in the same category, and proper documentation is mandatory. The OECD issued updated commentary on equity compensation sourcing in recent years, but countries are still implementing it inconsistently.

Which Countries Are Most RSU-Friendly for Expats

| Country | RSU/Equity Tax Treatment | Notes for US Expats |

|---|---|---|

| UAE | No income tax on employment income | Foreign-source RSU portion: zero local tax; US-source still taxed by IRS |

| Singapore | No capital gains tax; RSU income at vest taxed as employment income | 22% effective maximum; FTC works well; clear equity sourcing rules |

| Cyprus | Non-dom: dividends exempt; equity income taxed at standard rate | No CGT on share sales; FTC eliminates US liability for high earners |

| Ireland | RTSO (Relevant Tax on Share Options) paid within 30 days of exercise | Strict deadlines; Ireland-US treaty is strong; credit mechanism works |

| Germany | Full marginal income tax at vest (up to 47.5%) | High foreign taxes generate large FTC — often eliminates all US liability |

| UK | Income tax at vest; capital gains on subsequent appreciation | Strong treaty; HMRC sourcing methodology differs from IRS — reconciliation needed |

Low-tax jurisdictions like the UAE benefit expats with large unvested equity and significant US-source fractions. The foreign-source slice bears zero local tax, and if you have accumulated FTC carryforwards from prior high-tax years, they can reduce the US-source obligation too.

When You Work for a Foreign Company

If you're an American employed by a non-US company that grants you equity — RSUs, options, phantom shares, or SAR awards — the treatment differs again. Foreign company equity typically doesn't qualify as ISOs (those are IRS-defined for US companies only). It's usually treated as NSO-equivalent: ordinary income at exercise or vest, reported on your foreign payslip, potentially absent from a W-2 entirely.

If the foreign company's shares settle into a foreign brokerage account, that account may trigger FBAR and FATCA reporting even before you sell. Accounts exceeding $10,000 aggregate require FinCEN Form 114 (FBAR). Accounts exceeding $200,000 (living-abroad threshold) require Form 8938 with your tax return. Penalties for missing either start at $10,000 per form per year. Review the complete FBAR/FATCA guide for thresholds and mechanics.

Before Your Next Vest: A Working Checklist

- Calculate grant-to-vest ratio for each grant batch: days worked in US divided by total vesting days.

- Contact your company's equity or global mobility team and document your work-location allocation in writing.

- Determine whether payroll will apply the sourcing split at withholding — if not, build the overpayment into your cash flow plan and recover it via your tax return.

- Model FEIE vs FTC for vest years using your host country's effective rate and treaty status. Do not assume one is always better.

- Check your prior home state (especially California and New York) for equity sourcing claims on RSUs that accrued while you were a resident.

- Calendar any ISO exercise windows — especially 90-day post-termination deadlines — before changing jobs or employers while abroad.

- Verify cost basis on every equity sale. FMV at vest is your basis for shares sold after vesting; accept no defaults from the brokerage's auto-populated 1099-B.

- Engage a CPA who specializes in cross-border equity compensation — not just a general expat preparer. The allocation mechanics are specific enough that generalists miss them.

Bottom Line

RSUs and stock options are the highest-leverage financial event in most tech workers' careers — and one of the most mishandled items on an expat's tax return. The grant-to-vest rule means your past follows your equity across borders. Employer payroll defaults assume you never left the US. State tax authorities have long memories and specific sourcing authority over income accrued while you were a resident.

Expats who calculate this correctly, choose the right exclusion or credit election, time their moves strategically, and keep meticulous location records can pay a fraction of what their US-based colleagues pay on the same income. Expats who ignore it pay twice — sometimes three times, counting state tax.

The IRS will never tell you about the grant-to-vest rule. Your employer probably won't either. That asymmetry is expensive.

This article is for educational purposes only and does not constitute tax, legal, or financial advice. International tax rules are complex, jurisdiction-specific, and subject to change. Consult a qualified cross-border tax professional before making decisions about equity compensation, foreign tax elections, or residency changes.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 29, 2026

Expat Tax & FinanceJuly 29, 2026

Form 4868 vs 2350 for Expats

Compare Form 4868 and Form 2350 for expats, choose the right extension, and protect cash flow before claiming Form 2555.

Expat Tax & FinanceJuly 28, 2026

Expat Tax & FinanceJuly 28, 2026

US Mortgage as an Expat: Document Checklist

Prepare the income, asset, credit, translation, and closing documents lenders ask for when expats apply for a U.S. mortgage.

Expat Tax & FinanceJuly 27, 2026

Expat Tax & FinanceJuly 27, 2026

EU VAT for US Ecommerce Sellers

Learn when U.S. ecommerce sellers need EU VAT, OSS, or IOSS, and fix checkout rules before taxes erase profit margins overseas.