The Expat HSA Guide: Triple Tax-Free Medical Savings Abroad

Most expats close their HSA when they move abroad. That's a mistake. Learn how to use your HSA for tax-free medical expenses worldwide—and who can still contribute.

How US expats can use their HSA for tax-free medical expenses worldwide, who can still contribute abroad, and how FEIE interacts with HSA deductions.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most US expats do the same thing when they move abroad: they cancel their US health insurance, switch to a local or international plan, and quietly close their Health Savings Account. It feels like the responsible, logical move. It's also a mistake that costs them thousands of dollars a year—compounded, potentially, for decades.

An HSA isn't just a US-only benefit. It's a portable, triple-tax-advantaged account that can be used for qualified medical expenses anywhere in the world—from a dental clinic in Bangkok to a specialist visit in Madrid to a hospital stay in Mexico City. The account doesn't expire, it doesn't get taxed on growth, and you don't have to report it to the IRS the same way you do foreign bank accounts. And in 2026, a significant rule change expanded who qualifies to contribute.

The real nuance: the HSA question isn't binary. Whether you can contribute has strict eligibility requirements. Whether you can use existing funds abroad is nearly always allowed. Understanding that distinction is worth real money.

What Is an HSA? The Triple Tax Advantage Explained

A Health Savings Account is a tax-advantaged account available to people enrolled in a qualifying High Deductible Health Plan (HDHP). It offers three separate tax benefits that no other savings vehicle in the US tax code matches:

- Contributions reduce your taxable income — Contributions are pre-tax (through payroll) or tax-deductible (if contributed directly). A family contributing the full $8,750 in 2026 lowers their taxable income by that entire amount.

- Growth is tax-free — Once your balance exceeds a threshold (often $1,000–$2,000 depending on provider), you can invest in mutual funds, ETFs, or other assets. That investment growth is never taxed.

- Withdrawals for medical expenses are tax-free — As long as you use funds for qualified medical expenses under IRS Publication 502, you owe zero tax on the withdrawal.

After age 65, you can withdraw HSA funds for any reason—not just medical—and pay ordinary income tax but no penalty. That makes an HSA function as a stealth traditional IRA for healthcare costs, with one key bonus: if used for medical expenses, it's completely tax-free. No IRA can match that.

Can You Use Your HSA While Living Abroad?

Yes—with one important caveat about prescription drugs. The IRS defines qualified medical expenses based on the nature of the expense, not the country where it occurred. A doctor's consultation in Colombia comes out of your HSA tax-free. A hospital stay in Thailand? Tax-free. Dental work in Mexico City? Tax-free. The geography doesn't change the IRS definition under IRC § 213(d) and IRS Publication 502.

The significant exception: foreign prescription drugs. The IRS generally does not allow HSA reimbursement for drugs purchased abroad because the FDA does not want you importing medications. This rules out reimbursing your local pharmacy prescription in most overseas countries—but everything else qualifies: doctor visits, hospital care, dental, vision, mental health treatment, lab tests, imaging.

You do need documentation. Keep copies of all foreign medical bills, receipts, and doctor's letters. If you can't document an expense and you're under age 65, you'll owe income tax plus a 20% penalty on the distribution.

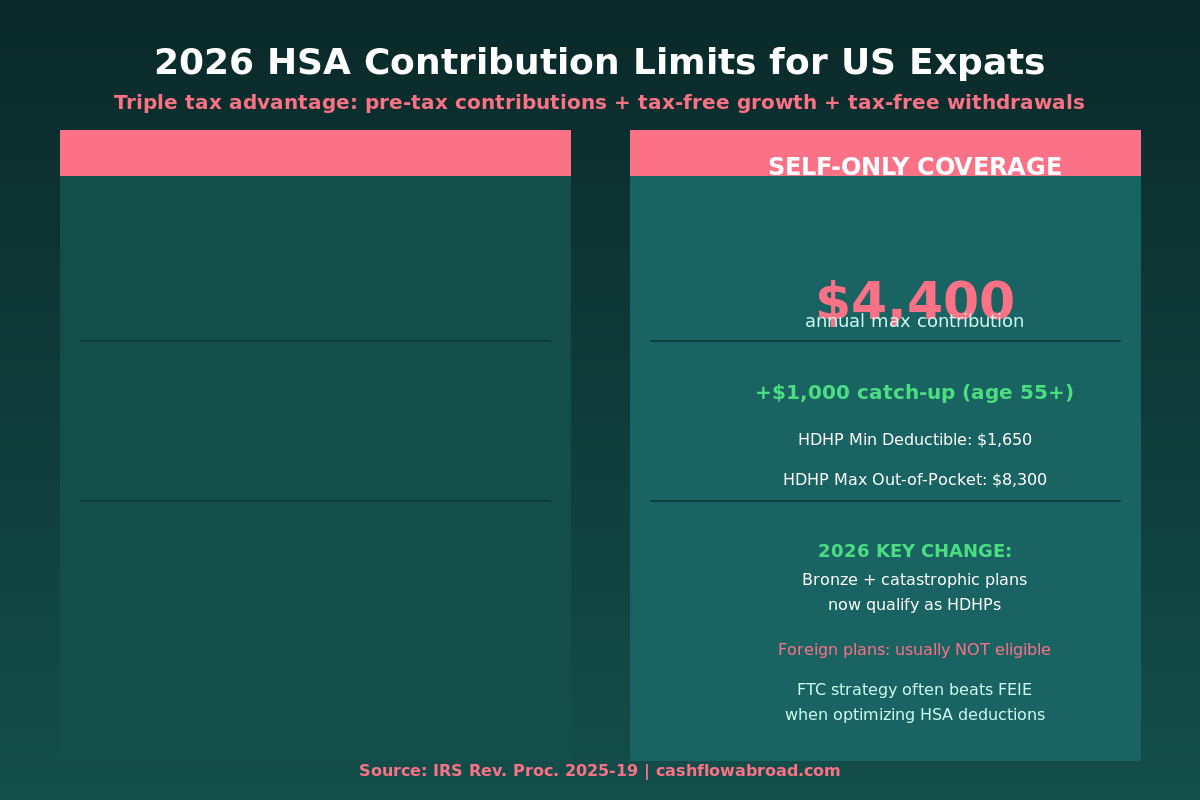

2026 HSA Contribution Limits for Expats

The IRS announced updated limits in Revenue Procedure 2025-19:

| Coverage Type | 2025 Limit | 2026 Limit | Catch-Up (Age 55+) |

|---|---|---|---|

| Self-only HDHP | $4,300 | $4,400 | +$1,000 |

| Family HDHP | $8,550 | $8,750 | +$1,000 |

HDHP minimum deductible requirements for 2026: $1,650 for self-only coverage, $3,300 for family. Maximum out-of-pocket limits are $8,300 (self-only) and $16,600 (family).

A family in the 24% federal bracket who maxes out at $8,750 saves $2,100 in federal income tax immediately—before investment growth and before tax-free withdrawals. Over a 20-year investment horizon at 7% annual returns, $8,750 invested annually compounds to roughly $380,000. All of it available for medical expenses tax-free, or for any expense after 65 with ordinary income tax.

The FEIE Problem—And How to Work Around It

This is where most expats either get tripped up or miss a planning opportunity. The Foreign Earned Income Exclusion (FEIE) lets you exclude up to $132,900 of foreign earned income from US federal income tax in 2026. If your income falls below that threshold, you may have zero US taxable income.

An HSA deduction has nothing to reduce if you have no US taxable income. You can still contribute (if eligible), and the growth and withdrawal benefits still apply. But you lose the upfront deduction—the most immediate and visible benefit for most contributors.

Three real solutions:

- Switch to the Foreign Tax Credit (FTC) instead of FEIE. If you live in a country with income taxes—Germany, France, Spain, Australia, Japan—the FTC may eliminate your US tax liability while preserving your taxable income on paper. That taxable income makes your HSA deduction valuable. This is the most overlooked planning switch in expat tax strategy.

- Earn income above the FEIE ceiling. If your foreign income exceeds $132,900, the excess is US-taxable. An HSA deduction reduces that excess dollar-for-dollar.

- Maintain some US-source income. Freelance income billed through a US entity, rental income from a US property, or interest/dividends creates taxable income your HSA deduction can offset.

The FEIE vs. FTC decision has implications far beyond the HSA—see the full breakdown in the FEIE vs. Foreign Tax Credit guide. For expats who want to maximize HSA contributions, the choice of exclusion method is directly connected to whether those contributions provide any upfront tax benefit.

Who Can Still Contribute to an HSA While Abroad?

HSA contribution eligibility depends on two things: enrollment in a qualifying HDHP, and not being enrolled in Medicare or claimed as a dependent. The country where you live is irrelevant. It's entirely about what health insurance you carry.

Maintain a US-Based HDHP

The most reliable path. If your employer offers a global HDHP, or if you purchase a US-based catastrophic plan through the ACA marketplace, you qualify. Many expats combine a low-cost US HDHP (for HSA eligibility) with a separate international plan (for actual overseas coverage). The US plan stays minimally active; the international plan handles day-to-day care abroad. This works particularly well for expats who spend some months in the US annually.

The 2026 Rule Change: Bronze and Catastrophic Plans Now Qualify

IRS Notice 2026-5 is significant for expats. Starting in 2026, bronze and catastrophic health plans purchased through ACA exchanges automatically qualify as HDHPs—even if their deductibles don't technically meet the traditional minimums. A catastrophic plan for someone under 40 costs $100–$200/month and now unlocks up to $4,400/year in HSA contributions. For expats who make annual US visits and enroll during open enrollment, this removes the main eligibility barrier.

Employer-Provided Global HDHPs

Some multinational employers offer US-compliant HDHPs covering employees internationally. If yours does, confirm with HR that the plan meets IRS HDHP requirements, then max out your HSA every year you're eligible. This is the cleanest solution when it exists.

What Qualifies as an HSA Expense Abroad

The IRS applies the same Publication 502 rules overseas as it does domestically. Here's what to expect when paying for care abroad:

| Expense Type | HSA Eligible Abroad? | Notes |

|---|---|---|

| Doctor visits / specialist consultations | Yes | Keep receipts and any diagnosis documentation |

| Hospital stays and surgery | Yes | Both inpatient and outpatient qualify |

| Dental care (fillings, crowns, extractions) | Yes | One of the best uses given cheap quality abroad |

| Vision (exams, glasses, contacts, LASIK) | Yes | Laser eye surgery qualifies |

| Mental health / therapy sessions | Yes | Licensed practitioners required |

| Lab tests, imaging, X-rays | Yes | Any diagnostic procedure |

| Prescription drugs purchased abroad | Generally No | FDA import rules block most foreign prescriptions |

| Medical marijuana (even legal locally) | No | Not FDA-approved |

| Cosmetic procedures | No | Unless medically necessary |

| Emergency medical evacuation transport | Partial | Medical transport qualifies; non-medical components don't |

Dental is where the real leverage is. Full porcelain veneers in Colombia or Mexico run $3,000–$5,000 USD. The same procedure in the US costs $20,000–$30,000. Pay with your HSA debit card—pre-tax dollars buying care that was already 80% cheaper. That combination is nearly impossible to replicate with any other tax-advantaged vehicle. For more on medical tourism costs and what's worth doing abroad, see the medical tourism expat guide.

International Health Insurance and HDHP Eligibility

Many international plans look like HDHPs on paper—high deductibles, catastrophic-style coverage, annual limits. The IRS doesn't care what a plan looks like. It only cares whether the plan meets specific statutory requirements under IRC § 223.

SafetyWing's Nomad Insurance does not qualify as an HDHP. Its subscription model with a low base deductible immediately disqualifies it, and it's not structured as a US insurance plan. For $50–$100/month, SafetyWing is excellent for travel medical coverage—but it won't make you HSA-eligible. The right structure is to pair a SafetyWing plan alongside a US-based HDHP, not use it as a replacement for one.

Cigna Global offers comprehensive international coverage from around $250/month, but their internationally-focused products are a different line from their IRS-compliant domestic HDHPs. Confirm HDHP status explicitly with any insurer before counting on HSA eligibility.

HSA Strategy by Expat Situation

| Expat Situation | HSA Contribution Eligible? | HSA Deduction Useful? | Best Strategy |

|---|---|---|---|

| Foreign income only, FEIE, fully excluded | Only if on qualifying US HDHP | No (no taxable income) | Keep existing balance invested; consider FTC switch |

| Foreign income, FTC in high-tax country | Only if on qualifying US HDHP | Yes (FTC preserves taxable income) | Max HSA if eligible; FTC + HSA deduction combo |

| Income above FEIE limit ($132,900+) | Only if on qualifying US HDHP | Yes (reduces excess above exclusion) | Max HSA contributions every year |

| Remote employee of US company, employer HDHP | Yes (if plan qualifies) | Yes | Max out employer HSA and payroll deduction |

| Low/zero-tax country, no US tax due | Only if on qualifying US HDHP | No | Focus on spending existing balance for foreign care |

| Annual US visitor, ACA enrollment during visit | Yes under 2026 rules (bronze/catastrophic) | Depends on income structure | Enroll in ACA plan during visit + max contribution |

Practical Setup: Keeping Your HSA Working Abroad

If you already have an HSA and are moving abroad—or already abroad—here's what to actually do:

- Don't close the account. Even if you can't contribute, the existing balance stays invested, grows tax-free, and can be used for any qualified foreign medical expense.

- Invest your balance. Fidelity HSA, Lively, and HealthEquity all allow investment of HSA balances into index funds. Sitting in cash at 0.01% inside a triple-tax-advantaged account wastes the most valuable part of the benefit.

- Keep a US address. HSA providers require a US address for account maintenance. A virtual mailbox ($15/month) gives you a real US street address in 50+ cities—essential for maintaining US financial accounts while abroad. See the full virtual mailbox guide for how it works.

- Document every foreign medical expense. Create a dedicated folder—physical or cloud—for every receipt, bill, and doctor's letter from foreign care. Keep records for at least 3 years beyond the tax year of each distribution.

- Run the FEIE vs. FTC analysis with a CPA. This single decision may be worth more than any other tax choice you make as an expat, especially once you factor in HSA eligibility and deductibility.

For the full picture of maintaining US financial accounts abroad—banking, brokerage, HSA—the zero-fee expat banking stack guide covers the complete setup. For overall expat investment strategy, including how to avoid PFIC traps with foreign funds, see the expat investing playbook.

Your HSA Crosses Every Border You Do

The Health Savings Account is one of the most tax-efficient tools the US tax code offers, and it doesn't stop working when you cross a border. The ability to use existing balances for qualified medical expenses worldwide is a benefit most expats leave completely untapped—either because they closed the account or because they left the balance sitting in uninvested cash.

The 2026 bronze/catastrophic plan changes open a meaningful new path for expats who visit the US annually to maintain HSA contribution eligibility. The FEIE interaction is the one area requiring active planning: if you exclude all your income under FEIE, the upfront deduction disappears, and a Foreign Tax Credit approach may unlock both lower taxes and more HSA value simultaneously.

The math is clear. A US expat family that maintains HSA eligibility, maxes the annual contribution at $8,750, invests in index funds, and uses the balance for dental and specialist care abroad—in cheap, high-quality medical markets—is stacking three separate layers of tax efficiency against some of the most competitive healthcare pricing in the world. That combination is genuinely hard to beat.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute tax, financial, or legal advice. HSA eligibility rules, contribution limits, and HDHP requirements are subject to IRS interpretation and may change. Every expat's tax situation is different—consult a licensed CPA or tax professional who specializes in US expatriate taxation before making decisions about HSA contributions, FEIE elections, or health insurance coverage.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 4, 2026

Expat Tax & FinanceMay 4, 2026

Your HSA Abroad: The Rules That Surprise Every Expat

Can you use your HSA abroad? Contribute while on FEIE? Which expat plans qualify? The complete 2026 HSA rules for US expats living overseas.

Expat Health & InsuranceJune 22, 2026

Expat Health & InsuranceJune 22, 2026

Self-Employed Expat Health Insurance Deductions

IRC 162(l) lets self-employed expats deduct 100% of premiums — but the FEIE can zero out the ceiling via Form 7206. Learn the math and when FTC wins.

Expat Health & InsuranceMay 17, 2026

Expat Health & InsuranceMay 17, 2026

Medicare Abroad: Your US Coverage Stops at the Border

Medicare covers $0 for most care outside the US. Learn the Part B penalty trap and the best international health insurance options for expat retirees.