Expat Domicile Strategy: The $40K Decision Before You Leave

California taxes you 13.3% on income the IRS excluded. Here's how to pick the right US state domicile before moving abroad — and save up to $40K/yr.

California charges 13.3% on FEIE-excluded income. Here's how to change your US state domicile before moving abroad and legally eliminate state taxes.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

A reader emailed us last year with a story that still stings. He'd lived in Medellín for two full years, filed his taxes correctly, claimed the Foreign Earned Income Exclusion, and paid zero federal income tax on $280,000 of self-employment income. Then his California CPA sent him a bill: $37,240. California didn't care that the IRS excluded his income. California never does.

This is the domicile trap — and it costs US expats tens of thousands of dollars per year because they never dealt with it before they left. The fix isn't complicated, but the window to act closes the moment you board your flight.

Why State Taxes Chase You Across Borders

The US federal government taxes citizens worldwide, but states have no constitutional obligation to follow the same rules. Most don't. And a handful of states — led by California — have built entire enforcement machines around collecting from residents who think they've left.

The core issue: domicile. Your domicile is your "true home" — the state you intend to return to. It's not where you live right now. It's where you have the deepest ties: your property, your family, your professional licenses, your bank accounts, your voter registration. Until you formally sever those ties and establish domicile somewhere else, your old state can (and will) claim you as a resident.

California's Franchise Tax Board audits thousands of residents every year specifically for "residency misclassification." They have algorithms. They buy data. They cross-reference passport stamps, credit card transactions, and property records. The burden of proof is on you to prove you left — not on them to prove you stayed.

The FEIE Problem California Won't Tell You About

Here's what trips up smart, financially literate expats: the Foreign Earned Income Exclusion (FEIE) is a federal mechanism. For 2025, it lets you exclude up to $130,000 of foreign-earned income from federal taxable income. Use it correctly and your federal tax liability drops to near zero.

California does not recognize the FEIE.

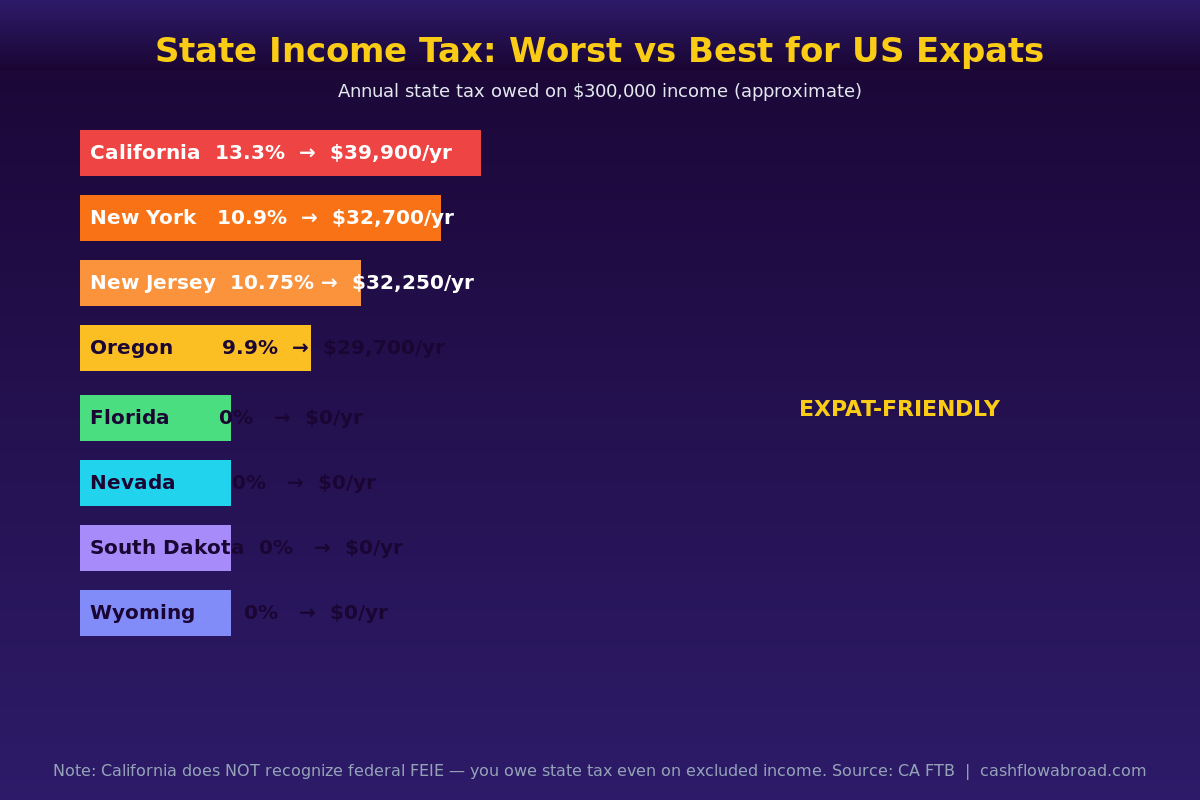

That's not an oversight — that's policy. The California FTB treats every dollar of your income as taxable California income if you're still considered a California resident, even income the IRS says you don't owe federal tax on. At 13.3% on income above $1 million and 9.3% on income above $61,214, a California-domiciled expat earning $300,000 abroad owes roughly $22,000–$28,000 in California state taxes per year on income they pay zero federal tax on.

New York and New Jersey have similar postures. New York's top rate hits 10.9% (plus NYC city tax up to 3.88%), New Jersey tops out at 10.75%, and both states pursue non-resident audits aggressively. Virginia and Oregon are also known for residency enforcement, though somewhat less aggressive than the top three.

The Numbers: Worst vs. Best States for Expats

| State | Top Income Tax Rate | Annual Tax on $300K | Recognizes FEIE? | Expat-Friendly? |

|---|---|---|---|---|

| California | 13.3% | ~$24,000–$39,900 | No | No |

| New York (+NYC) | 10.9% (+3.88% NYC) | ~$32,700+ | Partially | No |

| New Jersey | 10.75% | ~$32,250 | Partial | No |

| Oregon | 9.9% | ~$29,700 | No | No |

| Florida | 0% | $0 | N/A | Yes |

| South Dakota | 0% | $0 | N/A | Yes |

| Nevada | 0% | $0 | N/A | Yes |

| Wyoming | 0% | $0 | N/A | Yes |

| Texas | 0% | $0 | N/A | Yes |

| Washington | 0% (income) | $0 | N/A | Yes |

Eight US states have zero state income tax. For a high-earning expat, switching domicile from California to any of them before departing is the single highest-ROI financial move available — worth more per year than most investment strategies you'll spend weeks researching.

California's 546-Day Rule: The One Escape Hatch

California does offer one formal non-resident safe harbor, but it's narrow. Under the "employment-related contract" rule, you qualify as a California non-resident if:

- You leave California under an employment-related contract (including self-employment contracts with foreign clients)

- You remain outside California for at least 546 consecutive days

- You spend no more than 45 days per year in California while abroad

This sounds achievable, but the FTB interprets "employment-related contract" conservatively. If your income is from a US-based LLC or clients, or if you're running a business rather than working for a specific employer, the FTB may deny the safe harbor. Tax attorneys have documented cases where clients met the literal requirements and still faced audits. The safe harbor is real, but it's not a substitute for changing domicile if you want genuine certainty.

The cleaner path: establish domicile in a no-tax state before you leave, maintain the connections that prove it, and never worry about the 546-day countdown.

Florida vs. South Dakota: The Top Two Expat Domicile States

Most expat tax attorneys route clients toward either Florida or South Dakota. Both have zero state income tax, no estate tax, and systems built for maintaining residency while living abroad.

| Factor | Florida | South Dakota |

|---|---|---|

| State income tax | 0% | 0% |

| State estate/inheritance tax | None | None |

| Driver's license renewals while abroad | Yes (mail/online) | Yes (mail/online) |

| Ease of establishing fresh domicile | Moderate (easier with FL ties) | Very easy (1-day Sioux Falls trip) |

| Voter registration while abroad | Yes (UOCAVA) | Yes (UOCAVA) |

| Banking infrastructure | Excellent | Good |

| Best for | Expats with existing FL family/ties | Those establishing fresh domicile from scratch |

South Dakota is the dark horse most people overlook. You don't need to have ever lived there. The state's DMV allows new residents to get a driver's license after a brief in-person visit — most people handle everything in a single day in Sioux Falls. Vehicle registration is straightforward, and the state's residency requirements are simple enough that attorneys specializing in expat domicile specifically route clients through South Dakota to establish a clean slate.

Florida is better if you already have family there, own or rent property, or have existing financial ties. The homestead exemption can also reduce property taxes for Florida residents, which matters if you maintain a Florida property as your US base.

Step-by-Step: Establishing New Domicile Before You Leave

The key word in domicile law is intent. You need to show genuine intent to make the new state your home. One forwarded piece of mail doesn't cut it. Here's what actually builds a defensible domicile record:

1. Get a Physical Address

You need a real street address in your target state — not a PO box. A virtual mailbox service like Traveling Mailbox gives you a real street address in 50+ US cities, mail scanning, and check deposit capabilities for around $15/month. This is the foundation of maintaining a US domicile while living abroad. It gives you a legitimate address for your bank accounts, driver's license, IRS filings, voter registration, and brokerage accounts — all the things that build a domicile paper trail.

2. Transfer Your Driver's License

Your driver's license is the single biggest domicile indicator courts and tax authorities look at. Get a license in your new state. Surrender your old one or let it lapse. Do this at least 6 months before departure — the longer the record, the better.

3. Register to Vote in the New State

Voter registration is public record and carries significant weight in domicile disputes. Register in your new state immediately. If you're coming from California, deregister there at the same time — leaving a California registration active is a gift to a future FTB auditor.

4. Move Your Financial Accounts

Update the address on every financial account to your new domicile state: brokerage, retirement accounts, credit cards, banking. Charles Schwab's investor checking account is the standard for expats — zero foreign transaction fees, unlimited worldwide ATM fee reimbursements, no minimum balance, and it works seamlessly with any US address regardless of where you physically live. Setting up Schwab with your new domicile address adds another anchor point to your domicile record.

5. Update Professional Licenses and Insurance

Any state-issued professional license (CPA, attorney, real estate, contractor) should be transferred or allowed to lapse. Insurance policies — auto, life, umbrella — should list your new state address. These are secondary indicators, but they matter when an auditor is building a case.

6. File a Part-Year Resident Return in Your Old State

File a "part-year resident" return in your old state for the year of departure, explicitly declaring your move date and new domicile. This creates a formal record that you left. Don't skip this step — silent departure is exactly what triggers audit flags in California's residency tracking systems.

The Timeline: How Long Does This Actually Take?

Tax attorneys recommend allowing 6–12 months to fully establish a new domicile before departing. Here's a practical timeline:

- Month 1–2: Set up a virtual mailbox in your target state. Update billing address on key accounts to begin building the paper trail.

- Month 2–3: Travel to your target state. Get your driver's license in person. Register your vehicle if applicable.

- Month 3–4: Register to vote. Open a bank account. Update brokerage accounts and retirement accounts.

- Month 4–6: Transfer professional licenses or let old-state licenses lapse. Update insurance. File Form 8822 with the IRS to update your address.

- Month 6–12: Live your new domicile. Use the new address consistently. Build a paper trail through use.

- Departure year: File part-year resident return in old state. File as resident of new state going forward.

The deeper you go into this process before you leave, the harder it is for a former state to claim you back.

Five Things That Blow Up a Domicile Claim

California's FTB auditors look for specific "ties" that suggest continued California residency. Leaving any of these in place undercuts everything else you've done:

- A California home you own and can use — even a rental property where you sometimes stay. If you return there during US visits, the FTB counts it as your California "abode."

- A California driver's license — the #1 audit red flag. Transfer or surrender it before you leave.

- California-registered vehicles — register them in your new state or sell them.

- Active California business entities — an active California LLC or corporation maintains a business nexus. Talk to a tax attorney about restructuring before departure.

- Spending more than 45 days per year in California — track your days meticulously. Calendar entries and credit card receipts from outside California are your evidence.

Banking, Mailbox, and Keeping US Infrastructure Alive

One underappreciated benefit of a clean domicile change: it keeps your US banking intact. Many expat banking problems stem from having a foreign address on file with a US bank or broker. Maintaining a legitimate US address through your new domicile and a virtual mailbox prevents account closures and FATCA complications.

The workflow that works: Traveling Mailbox for a real US street address (not a PO box — banks and brokerages specifically reject PO boxes) plus Charles Schwab for banking and brokerage. At $15/month for Traveling Mailbox, it's one of the cheapest and most valuable tools in the expat stack — read our full guide on the virtual mailbox for expats for setup details.

For a deeper look at state-level enforcement and what happens during an audit, see our companion guide on how state taxes follow US expats abroad. For the federal side, the FEIE vs. Foreign Tax Credit decision is the other major tax lever to optimize before you leave.

Is It Worth the Effort?

Run the math for your situation. A $150,000 earner currently domiciled in California owes approximately $10,000–$14,000 per year in avoidable state taxes. Over a 10-year expat career: $100,000–$140,000 that could have been invested. At a 7% annual return, that's over $200,000 in lost future wealth.

The paperwork takes maybe 10–15 hours spread over 6 months. There is almost no financial task with a better return on time invested for a high-earning US expat.

If you're leaving from a no-tax state already — Texas, Florida, Nevada, Washington — your job is simpler: maintain those ties while abroad, not sever them. Keep the driver's license current, keep a banking address, vote. The work is in preservation, not establishment.

Bottom Line

Domicile strategy is the most overlooked lever in expat financial planning. The federal tax picture gets all the attention — FEIE, Foreign Tax Credit, PFIC rules, FBAR deadlines — but state taxes can silently exceed your entire federal bill if you leave without handling them first. A $300,000 earner leaving California without changing domicile is leaving $24,000–$40,000 per year on the table, legally and unnecessarily.

The move takes months of intentional setup. The savings last as long as you live abroad.

Financial disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Tax laws vary by state and individual circumstances change. Consult a licensed US tax attorney or CPA with expat domicile experience before making changes to your state of domicile. Rates and rules referenced are based on information available as of publication and may have changed.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceMay 25, 2026

Expat Tax & FinanceMay 25, 2026

State Domicile for Expats: Avoid the States That Chase You Abroad

California can tax your foreign income at 13.3% even after you leave. Learn how to change state domicile and save 5,000+ per year as a US expat.

Expat Tax & FinanceJune 18, 2026

Expat Tax & FinanceJune 18, 2026

Section 199A QBI Deduction: Do Expats Qualify?

The 20% QBI deduction is available to US expats on income above the FEIE limit. Learn 2026 thresholds, the SSTB trap for consultants, and how to claim