Dollar Savings for Expats: The Currency-Proof Money Stack

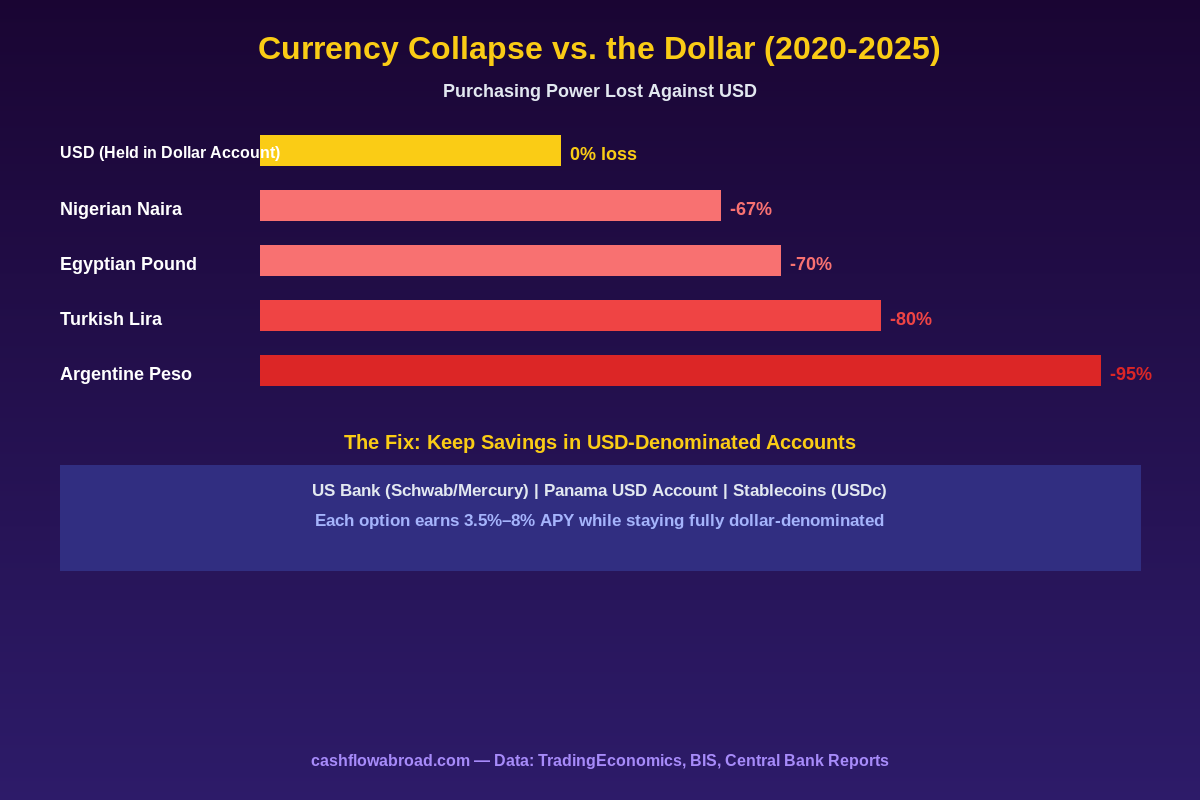

The Turkish lira lost 80% of its value against the dollar between 2019 and 2024. The Argentine peso shed 95% over the same window.

The Turkish lira lost 80% of its value against the dollar between 2019 and 2024. The Argentine peso shed 95% over the same window.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The Turkish lira lost 80% of its value against the dollar between 2019 and 2024. The Argentine peso shed 95% over the same window. The Nigerian naira? Down 67%. If you're an expat earning or saving in a volatile local currency, you're not just dealing with inconvenience — you're watching your net worth quietly drain.

The fix isn't complicated, but it requires deliberately building what I call a dollar stack: a layered system of USD-denominated accounts that sit outside volatile local banking systems while remaining fully accessible, compliant, and — critically — earning real yield. Most expats think about this too late. This guide breaks it down so you don't.

Why Currency Risk Is the Expat's Blind Spot

Expats obsess over tax strategy, visa status, and cost-of-living math. Currency risk rarely gets the same attention — until it does. When the Turkish lira drops 20% in a calendar year (as it did in 2024) or the Argentine peso gets devalued overnight, anyone holding local savings takes a proportional haircut on their wealth.

The problem compounds across multiple vectors:

- Local salary income — if you're paid in TRY, ARS, or NGN, you're accumulating depreciating assets by default

- Emergency fund — a 6-month cushion denominated in a volatile currency isn't a cushion, it's a liability

- Savings rate illusion — you might be saving 20% of your income, but if the currency falls 25% that year, you're actually losing ground

- Cross-border transfers — every time you convert to send home or invest, you crystallize the loss

The solution isn't to avoid countries with weak currencies. Many of them — Turkey, Colombia, Vietnam, Egypt — offer extraordinary cost-of-living advantages precisely because of their weak currencies. The strategy is to earn and spend in the local currency for day-to-day life while keeping your savings, emergency fund, and investment capital in dollars.

The FBAR Reality: Every Foreign Dollar Account Triggers Reporting

Before building your dollar stack, understand the compliance baseline. US citizens must file an FBAR (FinCEN Form 114) if the aggregate balance across all foreign financial accounts exceeds $10,000 at any point during the calendar year. That threshold is aggregate — three accounts with $4,000 each still require filing.

The 2026 FBAR deadline for the 2025 tax year was April 15, 2026, with an automatic extension to October 15. Non-willful violations carry penalties up to $10,000 per account per year. Willful violations can reach the greater of $100,000 or 50% of the account balance — per violation, per year.

In January 2026, the Second Circuit Court ruled that "reckless disregard" of FBAR requirements is enough to trigger the maximum willful penalty, joining six other circuit courts adopting the same standard. The days of arguing ignorance as a defense are essentially over.

What this means practically: foreign USD accounts do not escape FBAR. A dollar account at a Panamanian bank is still a foreign financial account. But reporting is not the same as taxation. Holding money in a foreign dollar account doesn't create additional US tax liability on the principal — only on the interest earned, which you'd owe anyway. For a full breakdown of the compliance landscape, see our US Expat Banking & Taxes guide.

Stablecoins sit in a newer gray area. The IRS and FinCEN haven't issued final guidance on whether USDC or USDT held on foreign exchanges definitively triggers FBAR reporting, but the conservative position — and the one most tax attorneys recommend — is to report if the balance exceeds $10,000 at a foreign-regulated platform.

Layer 1: Your US Home Base Accounts

The foundation of every expat dollar stack is a US-based banking relationship that doesn't close your account when you move abroad, doesn't charge foreign transaction fees, and gives you unfettered ATM access worldwide.

Charles Schwab Bank

Charles Schwab International offers the best pure-banking setup for US expats. The Schwab Bank Investor Checking Account provides unlimited worldwide ATM fee rebates — Schwab refunds whatever the ATM charged, anywhere on earth. No foreign transaction fees on debit purchases. No monthly maintenance fee. No minimum balance requirement (the previous $25,000 minimum was waived in 2025).

The catch: you need a US address to open the account. Once open, however, you can update to a foreign address and the account stays active. Pairing it with a virtual US mailbox solves this permanently.

Mercury Business Banking

For expats with a US-registered business, Mercury is the cleanest USD business account available. No fees, no minimum balance, API access, virtual cards, and a team-permission structure that works well for remote operations. Mercury can receive ACH, wire, and check payments — ideal for US-based clients paying a foreign-based contractor.

Mercury doesn't offer ATM debit access, so it pairs best with Schwab rather than replacing it.

| Account | Type | ATM Rebates | Foreign TX Fee | Min Balance | Best For |

|---|---|---|---|---|---|

| Schwab Investor Checking | Personal | Unlimited worldwide | None | $0 | Day-to-day spending abroad |

| Mercury | Business | None | None | $0 | Receiving US client payments |

| Schwab One Brokerage | Investment | N/A | None | $0 | US stock/ETF investing, PFIC-free |

Why does Layer 1 matter for currency protection? Your primary savings and investment capital stay in USD, inside FDIC-insured US institutions, earning market rates, without ever touching the local banking system. Even if the country you live in experiences a banking crisis or another currency collapse, your capital is untouched.

Maintaining Layer 1 requires a US address. The clean solution is a virtual mailbox like Traveling Mailbox — a real US street address in 50+ cities, with mail scanning, check deposits, and package forwarding. At $15/month it's the cheapest insurance you can buy for maintaining US banking access and IRS correspondence. See our full virtual mailbox guide for expats.

Layer 2: Offshore USD Accounts for Regional Liquidity

Layer 1 handles your long-term savings and investment capital. Layer 2 is your medium-term operating reserve — the 3-12 months of liquidity you don't want bouncing through international wires every week, but also can't leave sitting in a depreciating local currency.

The best jurisdictions for offshore USD accounts in 2026 share three traits: dollar-denominated accounts, reasonable access for US nationals, and manageable FBAR compliance.

Panama: The Dollar Country

Panama uses the US dollar as its official currency and has a well-developed offshore banking sector. USD savings accounts currently yield approximately 3.5% APY on liquid savings, with CDs running 4.5–5.5% for 12-24 month terms. Some banks advertise up to 8% on longer-term deposits.

Important caveat: Panamanian accounts are FBAR-reportable and carry no FDIC insurance — Panama's domestic deposit guarantee covers far less. Many major banks now require proof of income, residency documentation, and reference letters before onboarding US nationals. The compliance paperwork is real, but manageable.

Singapore

Singapore's major banks — DBS, OCBC, Standard Chartered — accept US clients with USD savings at 2.5–3.5% and minimal FX risk. Singapore's Monetary Authority manages the SGD in a de-facto currency board model, meaning the SGD itself has been a stable store of value for decades. Opening minimums run $1,000–$5,000 depending on account type, but access for Americans remains notably easier than most of Europe.

Georgia and Armenia

Two outliers for expats in that region: Georgia and Armenia both offer USD-denominated accounts at local banks with rates occasionally exceeding 5% on dollar deposits — higher than comparable US liquid savings products. Georgia's TBC Bank and Bank of Georgia are most commonly used by expats; Armenia's Ameriabank and HSBC Armenia have longer track records with foreign clients. Both countries are FBAR-reportable like any foreign account.

Layer 3: Stablecoins and On-Chain Dollar Yield

For expats comfortable with crypto infrastructure, stablecoins offer dollar denomination with yield rates that match or beat traditional offshore banking — without requiring a physical banking relationship anywhere.

The stablecoin yield landscape in 2026 breaks into several categories:

| Strategy | Typical APY | Risk Level | Liquidity |

|---|---|---|---|

| Tokenized T-bills (BUIDL, OUSG) | 4.5–5.2% | Low | Daily |

| Protocol savings (Aave, Sky/MakerDAO DSR) | 4–7% | Low-Medium | Instant |

| CEX yield (Kraken Earn) | 3–6% | Medium | Daily |

| Basis/funding trades | 8–15% | Medium-High | Variable |

| DEX liquidity provision | 5–25%+ | High | Variable |

For capital preservation with yield, tokenized T-bills and protocol savings modules are the practical entry point. You're earning essentially the US federal funds rate equivalent — just on-chain, without a bank account.

For expats in Latin America specifically, ARQ Finance bridges the traditional and on-chain gap cleanly. Available in Mexico, Colombia, Argentina, and Brazil, ARQ lets you hold balances in USDc and EURc, earn up to 4% on dollar balances, swap instantly to local currencies (MXN, COP, ARS, BRL), deposit USDC/USDT from external wallets, and spend via a Mastercard with cashback. For expats in LatAm who need local spending ability without local currency exposure, it's a solution to a very specific problem.

For direct crypto access from most jurisdictions where Coinbase is restricted, Kraken remains one of the most accessible regulated exchanges for US citizens abroad.

Stablecoin Tax Treatment

Stablecoin interest income is ordinary income for US tax purposes, reportable in the year received — regardless of whether you converted to fiat. Stablecoin-to-stablecoin swaps may be taxable events depending on price differences, though the spread between major USD stablecoins is usually negligible.

Keep clean records. CoinTracking handles this automatically — it imports transactions from major exchanges and wallets, calculates cost basis across methods, and generates the tax forms your CPA needs. For US expats running any stablecoin yield strategy, this is not optional overhead. See our crypto tax guide for US expats for full details.

Building Your Stack: The Allocation Framework

How you divide capital across layers depends on your location risk, tax situation, and liquidity needs. A practical starting framework:

| Capital Category | Recommended Layer | Example Accounts | Target Yield |

|---|---|---|---|

| Emergency fund (3-6 months) | Layer 1 (US) | Schwab Checking / money market | 4–5% |

| Operating reserve (1-3 months local) | Layer 2 or 3 | Panama USD account / ARQ Finance | 3.5–5.5% |

| Long-term investment capital | Layer 1 (US brokerage) | Schwab One Brokerage | Market returns |

| Stablecoin yield (optional) | Layer 3 | Kraken Earn / tokenized T-bills | 4–8% |

The cardinal rule: never keep more than 1-2 months of expenses in the local banking system in a high-currency-volatility country. More than that and you're volunteering to eat FX risk with zero compensation.

In dollarized economies — Panama, Ecuador, El Salvador — Layer 2 carries no currency risk by definition. The concern shifts to counterparty risk (bank stability) rather than FX. Dollarized doesn't mean financially stable.

Transferring Money Between Layers

A dollar stack is only as useful as your ability to move money efficiently. Key pathways:

US → Offshore USD account: International wires from Schwab or Mercury to a foreign USD account cost $15–$25 per transfer at Schwab. For regular monthly moves to specific corridors (US to Colombia, Philippines, Mexico), Remitly often offers more competitive rates. For USD-to-USD transfers within dollarized banking systems, a direct wire is usually simpler.

Local cash spending: Use the Schwab debit card everywhere and let Schwab refund the ATM fees. In cash-heavy economies, withdraw local currency at the ATM rate, spend locally, keep the dollar accounts intact. This is essentially free currency conversion at interbank rates.

On-chain flows: USDC moves between wallets and exchanges via Solana, Base, or Arbitrum for under $0.01 per transaction. For expats already using crypto rails, cross-border stablecoin transfers are nearly instantaneous.

A compliance note: moving $10,000+ between US and foreign accounts will trigger bank scrutiny and potentially Suspicious Activity Report filings. This is standard and creates no problem if you have documented source of funds. Keep statements. Our expat money transfer guide covers large cross-border transfers in detail.

The US Address Requirement

Layer 1 depends on maintaining a US address — for account opening, KYC/AML compliance, IRS correspondence, and Social Security administration. The cleanest solution is a virtual mailbox. Traveling Mailbox provides a real US street address (not a P.O. box) in 50+ cities, scans incoming mail within hours, allows remote check deposits, and forwards packages. At $15/month, it costs less than one international wire transfer fee.

Choosing the right state matters. South Dakota, Wyoming, Nevada, and Texas have no state income tax and no estate tax — ideal for establishing domicile. If you're using the FEIE to exclude foreign earned income while avoiding state tax liability, you need to be domiciled in a zero-income-tax state. More on that in our FEIE guide.

Annual Compliance Checklist

Running multiple USD accounts across jurisdictions requires disciplined annual compliance:

- FBAR (FinCEN 114): File if any foreign account exceeded $10,000 aggregate at any point. Due April 15, auto-extended to October 15.

- FATCA Form 8938: Required if foreign financial assets exceeded $200,000 at year-end or $300,000 at any point (for single filers abroad). Penalties for non-compliance exceed FBAR.

- Foreign interest income: Report on Schedule B. Interest from foreign banks is ordinary income regardless of where it was earned or held.

- Stablecoin yield: Report as ordinary income in the year received, whether converted to fiat or not.

- Account records: Keep statements for at least 6 years — the civil FBAR statute of limitations runs 6 years from the filing due date.

The Bottom Line

Dollar denomination is a strategy, not a destination. You don't need to move to a dollarized economy or abandon the country giving you a geographic arbitrage advantage. You just need to be intentional about where your money sits between paychecks.

The core stack works for most expats: Schwab for ATM access and emergency funds, Mercury if you have a US business, one offshore USD account or stablecoin option for regional liquidity, and a virtual mailbox to hold it all together. That combination keeps your net worth denominated in dollars while you spend local currency at the advantageous exchange rate.

The Turkish lira will probably keep depreciating. The Argentine peso will have more crises. That doesn't mean you can't build real wealth while living in Istanbul or Buenos Aires — it means you need to be smarter than the expat who just opened a local savings account and hoped for the best.

Disclaimer: This content is for informational purposes only and does not constitute financial, tax, or legal advice. Tax laws change frequently and vary by individual situation. Consult a qualified tax professional or financial advisor before making decisions about offshore accounts, foreign currencies, stablecoins, or cryptocurrency strategies. Stablecoin and cryptocurrency investments carry significant risks including total loss of principal.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Investing & Wealth BuildingJuly 23, 2026

Investing & Wealth BuildingJuly 23, 2026

International Bond ETF Withholding for Expats

Track foreign tax paid, Form 1116 limits, fund domicile, and broker reports before holding international bond ETFs abroad.

Investing & Wealth BuildingJuly 15, 2026

Investing & Wealth BuildingJuly 15, 2026

Self-Directed IRA for US Expats: What Can You Actually Hold?

Self-directed IRAs let US expats hold real estate, gold, and crypto — but UBIT, PFIC traps, and prohibited transactions can kill the account. 2026

Investing & Wealth BuildingJuly 7, 2026

Investing & Wealth BuildingJuly 7, 2026

Wash Sale Rules: Cross-Account Guide for US Expats

Multi-account US expats face hidden wash sale risks. Learn cross-account tracking, the IRA penalty that permanently destroys losses, and safe ETF