Czech Republic for US Expats: Taxes, Visas & the $1,800/Month Life

Most Americans associate European living with Paris rents and Scandinavian tax rates. That's not a travel perk — it's a business advantage.

Most Americans associate European living with Paris rents and Scandinavian tax rates. That's not a travel perk — it's a business advantage.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most Americans associate European living with Paris rents and Scandinavian tax rates. So when I tell you that a single person can live comfortably in the Czech Republic — in the heart of Central Europe, with full EU access — for around $1,800 a month, the instinct is to push back. Then you look at the numbers and realize Prague has been hiding in plain sight. It consistently ranks among the cheapest EU capitals, with a 15% income tax rate lower than most American states, a working tax treaty with the US, and a brand-new digital nomad visa designed specifically for remote workers. More than 100,000 Americans already call Europe home, and a growing share are skipping the obvious choices for Czechia.

Here's what that actually looks like on paper — taxes, visas, costs, and the parts the relocation blogs usually skip.

Why the Czech Republic Beats the Hype

The Czech Republic (officially Czechia since 2016) sits at the geographic center of Europe, giving it something few countries can claim: you're within two hours of Vienna, Berlin, Warsaw, and Budapest. That's not a travel perk — it's a business advantage. You can attend client meetings in four major European cities and sleep in your Prague apartment the same night.

The country has been in the EU since 2004, which means freedom of movement throughout the Schengen zone, access to EU professional licensing frameworks, and the ability to open a Czech company that trades freely with 26 other member states. Unlike Portugal or Spain — which have become so popular that digital nomads have driven up local rents by 40%+ since 2020 — Prague's housing market, while tighter than it was five years ago, remains dramatically cheaper than Western Europe.

The average monthly salary in the Czech Republic was around CZK 46,000 ($2,090) in early 2026. An American earning $5,000/month working remotely from Prague is effectively living on 2.4x the local average wage — a very different experience than earning $5,000 while renting in Lisbon at Western prices.

Czech Taxes for US Expats — The 15% Flat-ish Rate

The Czech Republic uses a two-bracket income tax system:

| Annual Income (CZK) | Annual Income (USD approx.) | Tax Rate |

|---|---|---|

| Up to 1,676,052 CZK | Up to ~$76,000 | 15% |

| Above 1,676,052 CZK | Above ~$76,000 | 23% |

In practice, most expats earning moderate remote incomes land entirely in the 15% bracket. That's a rate lower than California (top bracket: 13.3% state alone), New York (10.9%), or New Jersey (10.75%) — and comparable to flat-tax US states, except you're also getting access to EU healthcare and one of the most beautiful city centers on the continent.

Czech social security contributions add another 6.5% for employees or 29.2% for self-employed (on a capped contribution base). Factor that in when running total numbers. For a freelancer earning CZK 600,000 ($27,270)/year, the all-in Czech tax burden is still well under what many Americans pay stateside when you include state taxes and payroll taxes.

The FEIE Play: Zero US Tax on Czech-Earned Income

The Foreign Earned Income Exclusion (FEIE) for 2026 lets qualifying US expats exclude up to $132,900 in foreign-earned income from US federal taxes. If you meet the bona fide residence test (established legal residence in Czechia) or the physical presence test (330+ days outside the US in a 12-month period), you can potentially owe the IRS nothing on your Czech earnings.

Combine that with the Czech 15% rate and you're looking at a total tax burden that beats most US states — especially if you've escaped California or New York. The detailed mechanics of the FEIE strategy are documented here: structure your income correctly and your combined federal rate drops to what you owe Czechia and nothing more.

For passive income — dividends, capital gains, rental income — the FEIE doesn't apply. Use the Foreign Tax Credit instead, taking a dollar-for-dollar credit for Czech taxes paid against your US liability. This prevents double-taxation on investment income without requiring you to choose one mechanism over the other for earned income.

US-Czech Tax Treaty: What the Fine Print Says

The United States and the Czech Republic have a bilateral income tax treaty in force. Key provisions that matter to expats:

- Dividends: Maximum 15% Czech withholding on dividends paid to US residents (5% if you own 10%+ of the Czech company)

- Interest income: 0% withholding on interest paid between the two countries

- Pensions: Generally taxed only in the country of residence — relevant if you're drawing a US pension while living in Czechia

- Government pensions: Taxed only in the country that paid them (Social Security = US-taxable even abroad)

The treaty's standard savings clause means the US reserves the right to tax citizens as if the treaty didn't exist — so don't expect it to eliminate your 1040 obligation. You still file every year. But the treaty paired with the FEIE and Foreign Tax Credit makes actual double-taxation largely avoidable with proper planning. The complete expat tax guide covers FBAR, FATCA, and the full filing picture.

Social Security: Totalization Agreement Explained

The US and Czech Republic have a Totalization Agreement that prevents dual Social Security taxation. If you're employed by a Czech employer, you pay into the Czech system only. If you're working remotely for a US company or as a US self-employed contractor, you typically continue paying US Social Security and Medicare and are exempt from Czech social contributions. The specific assignment rule depends on your employment structure and duration — get a certificate of coverage from the SSA if you're in an ambiguous situation.

Visa Paths for Americans in the Czech Republic

US citizens enter Czechia visa-free for up to 90 days per 180-day Schengen period. Staying longer requires one of the following legal pathways:

Czech Digital Nomad Visa

Launched in 2023 and expanded in early 2025, the Czech Digital Nomad Program is a fast-tracked long-term visa for remote professionals in tech-adjacent fields. It's not as heavily marketed as Portugal's D8 or Estonia's Digital Nomad Visa — which is exactly why the application queue is still manageable.

Who qualifies:

- Remote work for a company or clients based outside the Czech Republic

- 3+ years of professional experience in IT — or a university degree in STEM. Marketing specialists were added to the eligible categories in February 2025.

- Minimum income: 69,836 CZK/month (~$3,175) — 1.5x the Czech average gross salary, recalibrated annually

- Comprehensive health insurance valid across the Schengen zone

- Clean criminal record from the US and any country you've lived in recently

Application specifics:

- Fee: 5,000 CZK (~$220)

- Processing: 45–90 days

- Duration: 1 year initial, renewable as a residence permit for 2 additional years — 3 years total

- Apply at the Czech embassy or consulate in your country of current legal residence

The income requirement is the real filter. At $3,175/month, this is designed for established remote earners, not people just launching a freelance career. If you're a software developer, product manager, UX researcher, or digital marketing professional clearing $5,000–$12,000/month remotely, you qualify comfortably.

Trade License (Živnostenský List)

The Živnostenský List is a Czech freelance business license — the equivalent of registering as a sole trader. It's the path most self-employed expats take who don't meet the IT background requirement for the Digital Nomad Visa. Once registered, you apply for a Long-Term Residency permit based on self-employment. Your foreign clients count — you don't need Czech customers.

Registration costs around 1,000 CZK ($45) at a local administrative office (živnostenský úřad) and usually takes under a week for straightforward trades. You'll file Czech tax returns on business income and pay Czech social (29.2%) and health insurance (13.5%) contributions on a calculated base. A Czech accountant runs CZK 2,000–3,000/month ($90–$135) — worth it in year one for navigating the bureaucracy in a language you don't speak yet.

Long-Term Work Visa and EU Blue Card

If you have a job offer from a Czech company, the standard long-term work visa or EU Blue Card applies. Blue Card requirements: a job paying at least 1.5x the Czech average gross salary plus a relevant university degree. Processing runs 60–90 days. If your employer is a US company with Czech or EU subsidiary operations, they may be able to sponsor you through this route.

Permanent Residency and the EU Passport Path

After 5 years of continuous legal residence, you can apply for Czech permanent residency. Requirements include financial self-sufficiency, a clean record, and passing a Czech language exam at the B1 level. The language requirement is the part people underestimate. Czech has seven grammatical cases and phonemes that don't exist in English. Five years gives you enough time, but only if you start studying in year one, not year four.

After 10 total years of residence (the last 5 as a permanent resident), Czech citizenship becomes available. That's an EU passport — the right to live and work in all 27 member states, visa-free access to 186 countries, and one of the most powerful travel documents in the world. For Americans thinking in decades rather than gap years, this is what puts the Czech Republic in a different strategic category than most digital nomad destinations.

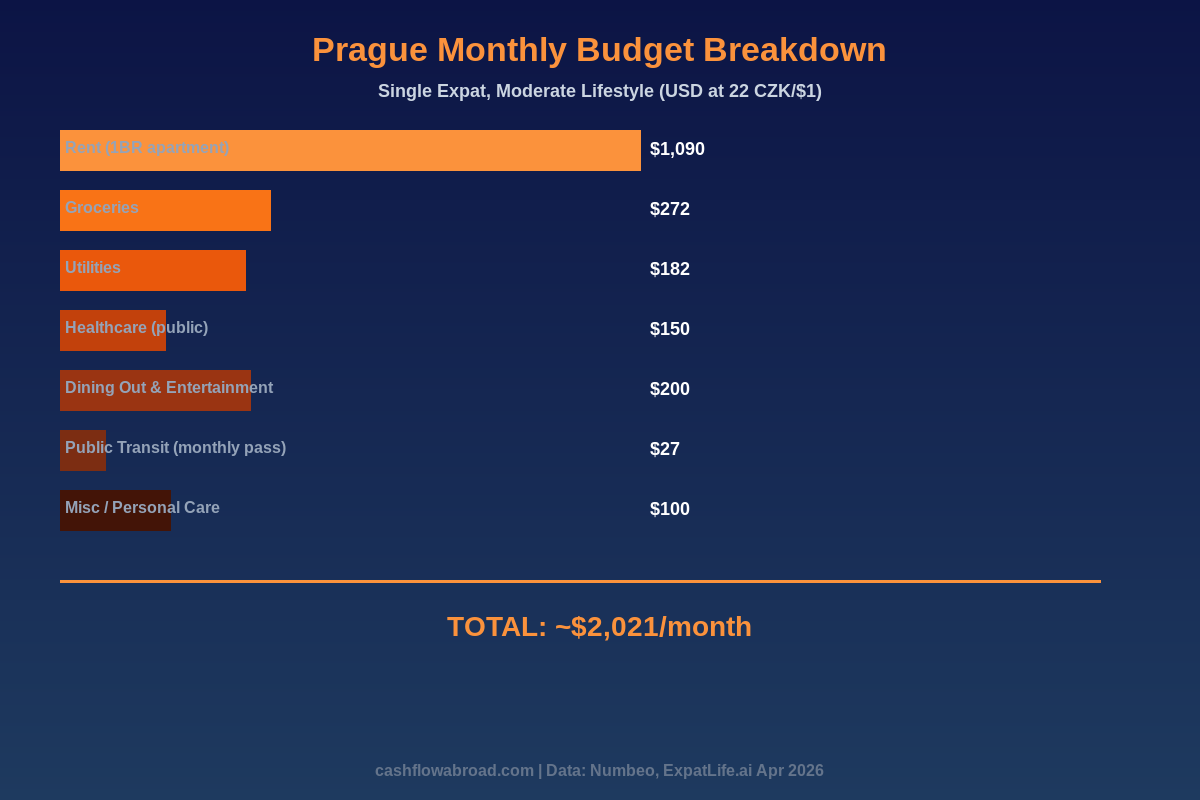

Cost of Living: City-by-City Numbers

Prague is more expensive than anywhere else in the country, but still dramatically cheaper than Western European capitals. Here's an honest comparison:

| Expense | Prague (USD) | Brno (USD) | Olomouc (USD) | Berlin (USD) |

|---|---|---|---|---|

| 1BR apartment (nice area) | $1,090 | $790 | $590 | $1,900 |

| Groceries (monthly) | $272 | $240 | $220 | $430 |

| Utilities | $182 | $160 | $145 | $300 |

| Public transit (monthly) | $27 | $22 | $18 | $90 |

| Healthcare (public contribution) | $150 | $150 | $150 | Employer split |

| Dining out / entertainment | $200 | $165 | $140 | $380 |

| Total monthly estimate | ~$2,021 | ~$1,527 | ~$1,263 | ~$3,500+ |

A dinner for two at a mid-range Prague restaurant runs $36–$54. A half-liter of Czech beer at a neighborhood pub: $2.25–$3.60. Czech pub culture was built for long winters and is priced accordingly. The grocery bill looks higher than you'd expect for Central Europe because Prague has fewer discount chains than German cities — but you're still spending half what a comparable lifestyle would cost in Amsterdam or Zurich.

Banking, Transfers, and Expat Finance Setup

The Czech Republic uses the Czech Koruna (CZK), not the Euro, despite EU membership. Euro adoption has been perpetually delayed with no concrete target date. For day-to-day life it's a non-issue; for wire transfers and exchange rate management, you need to account for the USD/CZK conversion (currently ~22 CZK per $1).

For your US banking, Charles Schwab International is the standard expat-approved setup — no foreign transaction fees, worldwide ATM rebates, and no account minimums. It's the account that doesn't penalize you for living abroad. Pair it with a local Czech bank account once you have your residence permit (Raiffeisen Bank and Moneta Money Bank both have decent English support).

For moving money between US and Czech accounts, Remitly consistently beats bank exchange rates on CZK transfers without the hidden spread that traditional wires bury in the conversion. For transfers above $10,000, compare Remitly's fee structure against your bank's wire fee — the difference is usually $50–$150 per transfer.

Maintaining a US mailing address is non-negotiable for keeping your US banking active, receiving IRS correspondence, and establishing state domicile. Traveling Mailbox ($15/month) gives you a real US street address in 50+ cities with mail scanning and check deposit capabilities — it's infrastructure, not a luxury. The full virtual mailbox guide for expats covers why it matters and how to set it up before you leave.

If you're investing from Czechia, read the PFIC trap guide before touching any EU-domiciled ETFs. Buying them through a Czech brokerage can trigger IRS PFIC rules at 37%+ effective rates. Stick with US-domiciled funds through Schwab or tastytrade.

Healthcare: Public System, Private Clinics, and Expat Coverage

The Czech public healthcare system ranks consistently in the top third of EU member states — universal coverage, functional hospitals, low out-of-pocket costs for legal residents. Self-employed expats who register in the system pay a minimum monthly health insurance contribution of CZK 3,306 (~$150) in 2026. Most GP visits and specialist referrals carry a nominal CZK 90 ($4) administrative fee. Hospitalization is generally covered without catastrophic costs.

The gap: you can't access the public system until you have legal residence status — a long-term visa or permit. During the application period (often 2–4 months), you need private coverage. SafetyWing Nomad Insurance starts at $45.08/month for under-40s and covers medical emergencies across the Schengen zone — the practical bridge until your Czech health registration kicks in. For a full breakdown of options, the expat health insurance guide compares SafetyWing, Cigna Global, and Allianz Care side by side.

Prague has several international private clinics — Canadian Medical, Unicare, and EUC Klinika — with English-speaking staff, short wait times, and prices far below US private care for equivalent services. An English-language GP consultation typically runs CZK 1,500–2,500 ($68–$113).

Where to Live: Prague Neighborhoods and Beyond

Prague is the default choice, and usually the right one for a first move. Neighborhood selection matters more than people expect:

- Vinohrady / Žižkov: The expat sweet spot. Walkable, excellent restaurants, younger crowd, strong café scene, 15 minutes by metro from center. 1BR: CZK 22,000–26,000 ($1,000–$1,180).

- Holešovice: Up-and-coming, strong arts and startup presence, 20% cheaper than Vinohrady, excellent transport. 1BR: CZK 19,000–23,000 ($865–$1,045).

- Smíchov / Nusle: More local character, older housing stock, quieter. 1BR: CZK 17,000–21,000 ($773–$955).

- Old Town / New Town center: Spectacular location, constant tourist traffic, overpriced for the quality. Not recommended for long-term renting.

Outside Prague, Brno deserves serious consideration. Czech Republic's second city, home to Masaryk University and a growing tech ecosystem, 90 minutes by train from Vienna. Monthly costs run $400–$600 less than Prague, the quality of life is genuinely high, and you're not competing with tourist-season crowds for coffee. Olomouc offers an even lower cost floor and is consistently rated one of the most livable Czech cities by locals — just smaller and less internationally connected.

The Downsides Nobody Talks About

Czech is a genuinely difficult language. Seven grammatical cases, consonant clusters unusual in European languages, and a phonology that takes months just to hear correctly. You can function in Prague on English — especially in tech, hospitality, and anything tourist-adjacent. But immigration offices, lease agreements, and tax forms run in Czech. Budget for a bilingual assistant or relocation service in year one, and start Czech lessons before you arrive if you're serious about staying long-term.

Housing is tighter than it was. Prague's rental market has squeezed significantly since 2021. Short-term rental platforms removed substantial stock, construction hasn't kept pace, and landlords in desirable neighborhoods often ask for 2–3 months' deposit upfront. Start your search at least two months before arrival, use expat Facebook groups and local real estate sites (Bezrealitky, Sreality) rather than tourist-facing platforms, and be prepared to move quickly when you find something good.

Opening a Czech bank account before you have a residency permit is hard. Most Czech banks require a registered address and valid long-term visa or permit. During your first 90 days, you'll rely on your US accounts and cash — another reason the Schwab international account (with ATM rebates) matters from day one.

US tax compliance doesn't get simpler just because you moved. You still file a 1040 annually. You still track FBAR if your Czech account exceeds $10,000 at any point in the year. The FEIE handles the math but doesn't eliminate the compliance overhead. Budget $500–$1,500/year for an expat-specialized CPA, especially in year one when you're establishing residency and splitting the year between countries.

Winter. Prague runs cold and grey from November through February — highs around 2–4°C (35–39°F), often overcast for weeks at a stretch. People from sunny climates consistently underestimate this. Czech pub culture, however, was invented precisely for this purpose, which helps.

The Bottom Line

The Czech Republic is one of the most underrated expat destinations in Europe, which is still its biggest advantage. You get genuine EU membership, a 15% base income tax rate, a working US tax treaty with totalization agreement, and a cost of living that makes a $5,000/month remote income feel like $10,000 in purchasing power. Prague is a legitimately world-class city: extraordinary architecture, functional public transit, internationally ranked universities, a serious restaurant and café scene, and crime rates that make most US cities look anxious by comparison.

The Digital Nomad Visa is the cleanest entry point for IT and marketing professionals. Apply at your nearest Czech consulate, give yourself 60–90 days processing time, line up housing before your Schengen 90 days run out, and register for the public health system as soon as your permit lands. The Trade License route works for freelancers who don't fit the IT mold. Either way, you're five years from permanent residency and ten years from an EU passport — which means this is a country worth treating as a real long-term play, not just an extended nomad stop.

If you're still comparing options, the ranked digital nomad visa guide puts Czechia in context. And before you make any move, get the expat tax and banking foundation right — it's the infrastructure everything else depends on.

Financial disclaimer: This post is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and visa regulations change frequently, and individual circumstances vary significantly. Consult a qualified expat tax professional and immigration attorney for guidance specific to your situation before making any financial or residency decisions.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 29, 2026

Expat Tax & FinanceJuly 29, 2026

Form 4868 vs 2350 for Expats

Compare Form 4868 and Form 2350 for expats, choose the right extension, and protect cash flow before claiming Form 2555.

Expat Tax & FinanceJuly 28, 2026

Expat Tax & FinanceJuly 28, 2026

US Mortgage as an Expat: Document Checklist

Prepare the income, asset, credit, translation, and closing documents lenders ask for when expats apply for a U.S. mortgage.

Expat Tax & FinanceJuly 27, 2026

Expat Tax & FinanceJuly 27, 2026

EU VAT for US Ecommerce Sellers

Learn when U.S. ecommerce sellers need EU VAT, OSS, or IOSS, and fix checkout rules before taxes erase profit margins overseas.