Costa Rica: The Zero-Tax Retirement Most Americans Miss

The average US Social Security benefit clears Costa Rica’s Pensionado visa bar by nearly double — and Costa Rica taxes all foreign income at $0. Here’s the full picture.

The average US Social Security benefit clears Costa Rica’s Pensionado visa bar by nearly double — and Costa Rica taxes all foreign income at $0.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The average American Social Security benefit hit $1,907 per month in 2024. Costa Rica's Pensionado retirement visa requires just $1,000 per month from a guaranteed pension. And Costa Rica taxes foreign income — Social Security, 401(k) distributions, US dividends, foreign pensions — at exactly $0.

That math is almost too clean to be true. For a retiree living on Social Security alone, Costa Rica may be the only country on earth where you can legally owe nothing in taxes to either government simultaneously. Yet almost no one in the expat finance world talks about it — they're busy debating Panama, Paraguay, and Portugal.

Here's the full picture: the upsides, the real costs by town, and the traps that turn this paradise into a tax nightmare for the wrong person.

Costa Rica's Territorial Tax: What It Actually Covers

Costa Rica operates on a pure territorial tax system. The rule is simple: only income earned within Costa Rica is subject to Costa Rican tax. Income earned outside the country — from any source — is completely exempt.

For a US retiree, this translates directly:

| Income Type | Costa Rica Tax | Notes |

|---|---|---|

| US Social Security | $0 | 100% exempt as foreign-sourced income |

| 401(k) / IRA distributions | $0 | Foreign retirement income — exempt |

| US stock dividends & capital gains | $0 | Foreign-sourced — exempt |

| US rental income | $0 | Foreign-sourced — exempt |

| Costa Rican dividends/interest | 15% flat | Locally-sourced — taxable |

| Income from CR employer | Progressive (10–25%) | Locally-earned — fully taxable |

One important clarification: this doesn't eliminate your US tax bill. The IRS taxes US citizens on worldwide income regardless of where they live. Your Social Security, dividends, and IRA distributions are still reported on your 1040. But here's the kicker — if your combined income (Social Security + other) stays under $34,000 as a single filer or $44,000 married filing jointly, up to 85% of your Social Security escapes US taxation too. Many retirees in Costa Rica who are drawing down modest Social Security plus dividends end up in a very low US bracket or even below the threshold. When Costa Rica also charges $0, the combined tax bill can genuinely approach zero.

See our full breakdown of how US expats can legally owe zero federal income tax for context on optimizing the US side of this equation.

The Pensionado Visa: Lower Bar Than You Think (But a Catch)

Costa Rica's Pensionado visa — the retirement residency pathway — has a $1,000/month income floor. With the average Social Security benefit at $1,907 in 2024, most American retirees clear this by nearly double.

But the type of income matters more than the amount. The requirement specifies a guaranteed lifetime pension. That means:

- Qualifies: US Social Security, federal/state government pensions, military pensions, corporate defined-benefit pensions

- Does NOT qualify: 401(k) balances you haven't annuitized, IRA withdrawals, investment income, rental income

A retiree with $600,000 in a 401(k) and no pension can't use that balance to qualify — even though the $600k could sustain $3,000/month indefinitely. The visa requires the pension to be ongoing and guaranteed, not discretionary. Many retirees are blindsided by this distinction.

What You Need to Apply

- Valid passport (all pages), 2 biometric passport photos

- Official letter from the pension authority certifying lifetime income — must be apostilled

- Birth certificate (apostilled)

- Police clearance from all countries of residence in the past 5 years (apostilled)

- Marriage certificate if applicable (apostilled)

Government fees: $200–$400. Most expats hire a local immigration attorney ($1,500–$3,000), which is strongly advised given Costa Rica's bureaucratic complexity.

Timeline: Officially up to 90 days. Reality: 6–12+ months is common. You can enter on tourist status while waiting, but manage your passport validity carefully.

The bonus most people don't know about: Pensionado residents receive legal discounts — 20% on utility bills, 15% on restaurant meals, 50% on entertainment, 25% off airfare within Central America, and 20% off medical consultations. A couple dining out regularly saves $100+/month on meals alone.

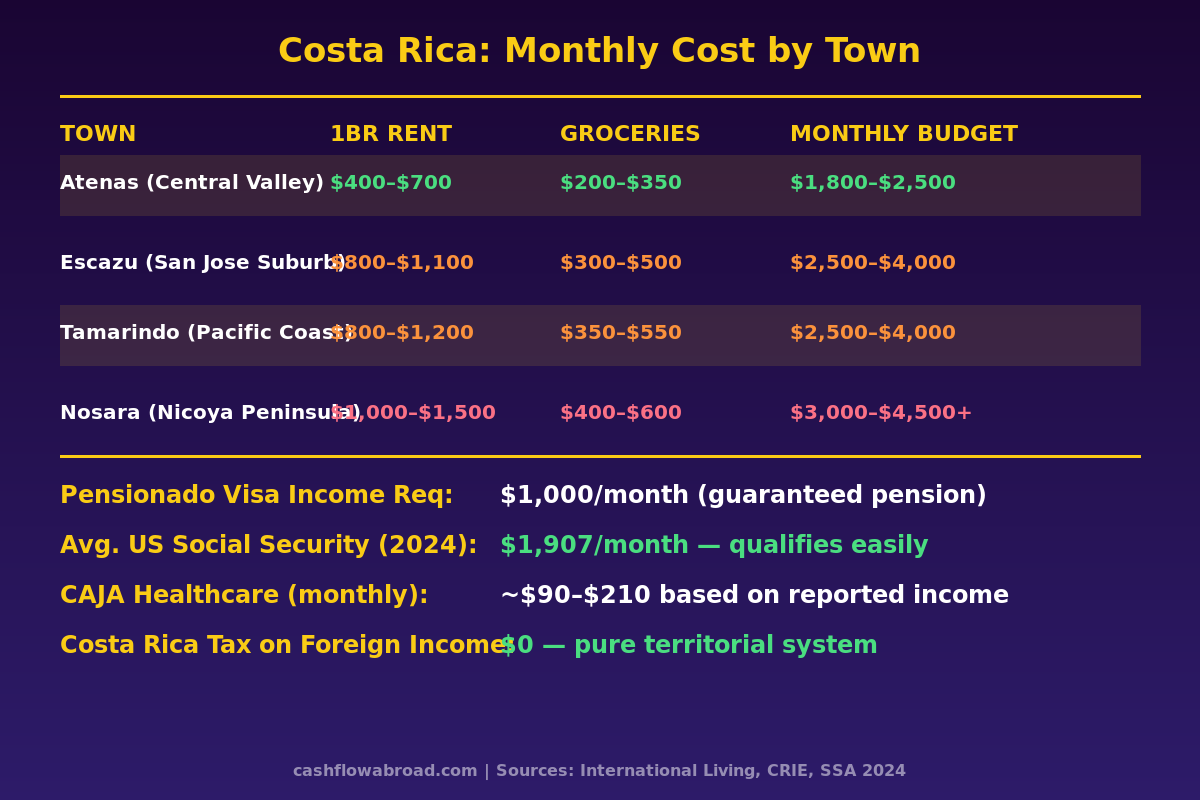

Cost of Living: Four Towns, Four Price Points

Costa Rica is not a monolith. Where you settle determines whether you're spending $1,800 or $4,500 per month.

Atenas — The Smart Retiree's Pick

A small colonial town in the Central Valley, roughly 25 minutes from the San José international airport. National Geographic once called it home to the world's best climate — low humidity, consistent 75°F year-round, no extremes. A 1-bedroom apartment runs $400–$700/month, groceries $200–$350/month, and a comfortable couple's budget lands around $1,800–$2,500 all-in.

The trade-off: limited nightlife and fewer urban conveniences. This is a quiet retirement town with a high concentration of North American expats, not a cosmopolitan hub. For retirees who want low cost and low noise, it's the best value in the country.

Escazú — The American Suburb of San José

Costa Rica's most developed suburb has everything: international supermarkets, Starbucks, multiplexes, and — critically — Hospital CIMA San José directly across the highway. CIMA is part of a Texas-based international hospital group with English-speaking specialists and equipment comparable to a solid US hospital. The price: $800–$1,100/month for a 1BR, monthly budgets of $2,500–$4,000 for a couple.

Tamarindo — Pacific Surf Town

"Gringo pricing" is real here. Tamarindo has become an international beach destination with strong tourism economics. Rents run $800–$1,200/month for a 1BR. The dry season (December–April) is picture-perfect Pacific paradise; the rainy season brings daily downpours and occasional isolation. Monthly budget: $2,500–$4,000.

Nosara — The Wellness Premium

The Nicoya Peninsula's flagship expat town has become a celebrity-adjacent wellness destination and one of Costa Rica's five Blue Zone communities — areas with extraordinary concentrations of centenarians. The price reflects the status: 1BR apartments run $1,000–$1,500/month, couple's budgets hit $3,000–$4,500+. Roads are notoriously terrible, hospitals are an hour away, and internet is inconsistent in rural sections. You're paying for remoteness and vibe as much as actual amenities.

Grocery Benchmark

| Item | Local Market Price |

|---|---|

| Dozen eggs | $2–$3 |

| Chicken breast (1 lb) | $3–$4 |

| Farmers market weekly haul | $20–$40 |

| Local beer (Imperial) | $1.00–$1.50 |

| Meal at local "soda" (café) | $4–$8 |

| Mid-range restaurant meal | $12–$25 |

Healthcare: The WHO Ranked Costa Rica Above the US

In the World Health Organization's global health system rankings, Costa Rica placed 36th globally — one spot above the United States at 37th. The country has maintained its reputation for quality care at low cost for decades.

Every legal resident is required to enroll in CAJA (Caja Costarricense de Seguro Social), the public health system. Once enrolled, CAJA covers doctor visits, hospital stays, surgeries, specialist referrals, and prescription drugs with no copays or deductibles.

Monthly CAJA cost is income-based — roughly 7%–11% of reported monthly income. A retiree reporting $1,000/month pays approximately $90–$110/month. On $1,907 (average Social Security), expect $133–$210/month. That's your mandatory healthcare floor.

The catch: public CAJA hospitals can have long wait times for non-emergency specialist care. Most expats run a dual strategy:

- Enroll in CAJA (mandatory anyway) for emergencies and primary care

- Add private coverage or pay out-of-pocket at CIMA for specialist care

Private plans in Costa Rica run $115–$475/month depending on coverage level — far below comparable US premiums. If you're not yet 65 and navigating the gap between employer coverage and Medicare, Costa Rica's system dramatically reduces that cost. Our expat health insurance guide covers the pre-65 gap in detail, including international options like SafetyWing that can supplement or replace CAJA for mobile retirees.

The Self-Employment Tax Trap: Who This Doesn't Work For

Costa Rica's tax advantages are real — but they apply specifically to retirees living on passive income. For anyone with active self-employment income, the picture changes sharply.

The US and Costa Rica have no totalization agreement. The US has signed these treaties with 30 countries — including most of Europe, Australia, and Japan — to prevent Americans abroad from paying Social Security taxes twice. Costa Rica is not on that list.

What this means for a self-employed American in Costa Rica:

| Tax Obligation | Rate | Notes |

|---|---|---|

| US Self-Employment Tax | 15.3% | Applies to net SE income — no exemption abroad |

| Costa Rica CAJA (self-employed) | 4.75%–7.25% | On locally-sourced income |

| Effective combined hit | ~20%–22.5% | No treaty relief available |

The Foreign Earned Income Exclusion (FEIE) can exclude up to $126,500 (2024) of active earned income from US income tax — but it does not eliminate self-employment tax. A freelancer earning $80,000 in Costa Rica still owes $12,240 in SE tax to the IRS on top of any income tax owed after the exclusion. CAJA contributions don't generate US Social Security credits, and there's no mechanism to cross-apply them.

The one partial relief: the IRS allows a deduction of 50% of SE tax from gross income when calculating income tax. A minor offset, not a real solution.

If your income is Social Security, pension, IRA distributions, US dividends, or rental income — Costa Rica is excellent. If you're a freelancer or consultant with active income, the SE tax math eats the benefit. Compare your options via our totalization agreements guide to find countries where that 15.3% double-hit disappears.

Banking and Staying Connected to US Financial Infrastructure

Maintaining US banking from Costa Rica requires planning. Most US banks close accounts once they discover you're a foreign resident. The exceptions that consistently work for expats: Charles Schwab International reimburses all ATM fees worldwide, charges zero foreign transaction fees, and integrates with their brokerage for investment management — everything a retiree needs from one account. For business banking if you maintain a US LLC, Mercury is fully remote-friendly.

A valid US mailing address is non-negotiable — the IRS needs it, your bank needs it, and your state domicile depends on it. Traveling Mailbox provides a real US street address in 50+ cities, scans your mail, and handles check deposits for about $15/month. Full breakdown in our virtual mailbox guide.

For transferring money between Costa Rica and the US, Remitly offers competitive exchange rates and fast delivery — typically within minutes for colón transfers.

Before you move, locking in the right US state domicile determines whether you'll owe state income tax while abroad. Florida, South Dakota, and Wyoming have no state income tax and are the most expat-friendly options. Read the full breakdown in our state domicile guide.

The Honest Drawbacks

Any article that only sells the upside is doing you a disservice. Here's what actually goes wrong:

Crime

San José province accounts for roughly 32% of national homicides. The US State Department rates Costa Rica at Level 2 ("exercise increased caution"). Violent crime against expats is lower than against locals, but opportunistic theft — bag snatching, car break-ins — is common in urban areas and tourist zones. Rural Central Valley towns like Atenas and Grecia have notably lower crime rates. The beach towns, particularly Tamarindo and port cities like Limón, have more.

Bureaucracy

"Tico time" is not a stereotype — it's the operating rhythm of government offices. Pensionado visa processing at 6–12 months is standard. Opening a local bank account as a non-resident can take weeks of document gathering. Budget for professional help; attempting to navigate Costa Rican immigration alone is a decision many expats deeply regret.

Traffic and Roads

San José has some of Latin America's worst gridlock. Road quality outside the Central Valley deteriorates sharply — potholes, unpaved sections, no guardrails on mountain routes. Rainy season (May–November) brings landslides that close roads for days.

The Attrition Reality

Roughly 40% of expats who move to Costa Rica eventually leave, driven by crime anxiety, bureaucratic fatigue, and the gap between the idea of paradise and the daily reality of inconsistent infrastructure. This isn't a reason not to go — it's a reason to rent before buying, visit across multiple seasons, and spend extended time in your specific target town before committing.

Who This Works For (And Who It Doesn't)

Costa Rica's zero-tax retirement path fits a specific profile precisely:

- Ideal: US retiree, 60–75, living primarily on Social Security + modest IRA withdrawals + US dividend income. Qualifies for Pensionado visa easily. Owes $0 to Costa Rica, potentially very little to the IRS. Healthcare covered via CAJA at $90–$210/month. Central Valley lifestyle for $1,800–$2,500/month as a couple.

- Workable but less clean: Early retiree (before 65) with significant passive income but no guaranteed pension. The Rentista visa ($2,500/month from any passive source) is the alternative pathway.

- Wrong fit: Active freelancer or self-employed consultant with US-sourced earned income. The 15.3% SE tax is unavoidable, and no totalization agreement provides relief. The geographic arbitrage playbook covers alternatives where that double-hit disappears.

For the right retiree — passive income, Social Security, modest lifestyle expectations — Costa Rica's combination is one of the most underrated retirement setups in the expat world. The people who figured it out already live there. That, in itself, tells you something.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual circumstances vary. Consult a qualified US expat tax professional and a licensed Costa Rican immigration attorney before making decisions based on this content. All figures reflect publicly available data as of the research date and may not reflect current regulations.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageMay 28, 2026

Geographic ArbitrageMay 28, 2026

Panama Residency: Live on $2,000/Month, Zero Local Tax

Panama taxes zero on foreign income and runs on the US dollar. Full guide to visas, costs, banking, and Pensionado discounts for expats.

Geographic ArbitrageMay 24, 2026

Geographic ArbitrageMay 24, 2026

Costa Rica Expat Guide: $2,100/Month, 0% Foreign Tax

Costa Rica taxes zero on foreign income. Live on $2,100/month and qualify with $1k/month SS. Complete visa, tax, banking, and cost of living guide.

Geographic ArbitrageMay 19, 2026

Geographic ArbitrageMay 19, 2026

Panama for US Expats: Dollar Economy, Territorial Tax, Visa Reality

Panama uses the US dollar, taxes zero foreign income, and has 53 international banks. Full guide to visas, costs, and banking for US expats.