Colombia for US Expats: Taxes, Visas & the $1,300/Month Life

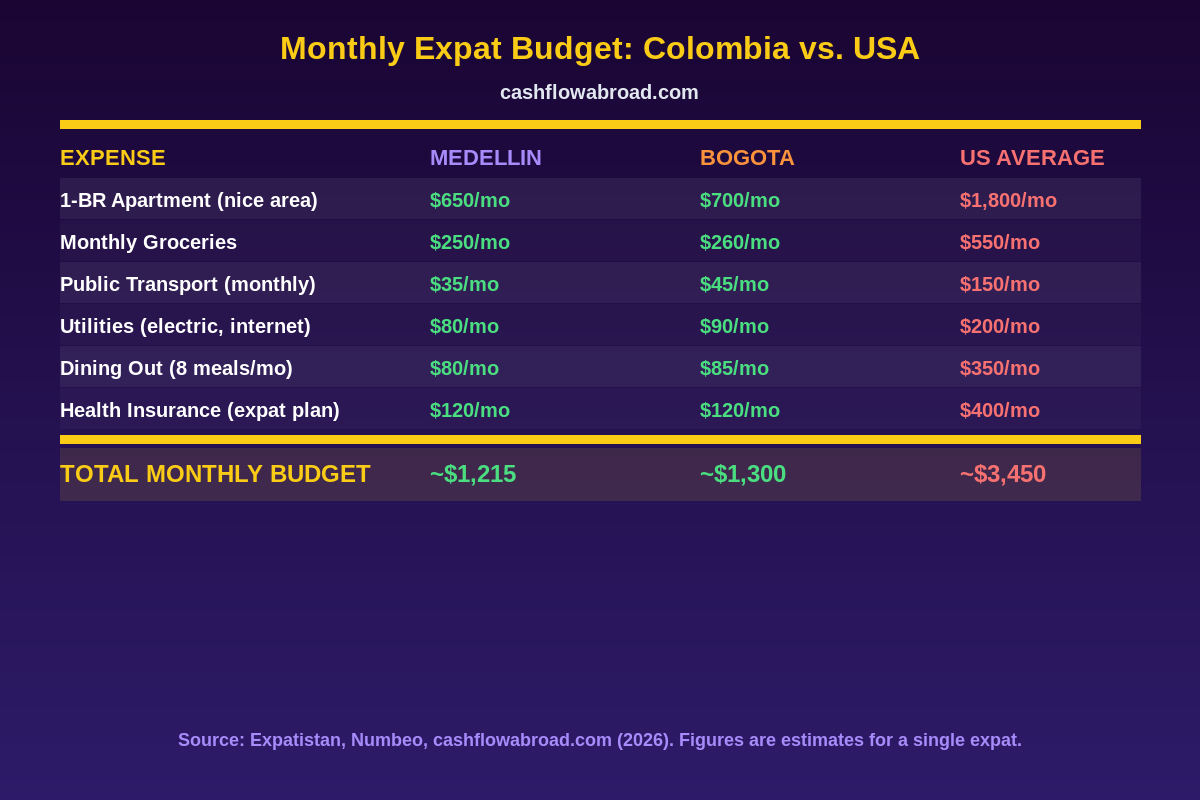

The average American household spends $3,450 a month on housing, food, and transportation. That gap isn't a rounding error.

The average American household spends $3,450 a month on housing, food, and transportation. That gap isn't a rounding error.

The average American household spends $3,450 a month on housing, food, and transportation. In Medellín, a comfortable expat life — nice apartment, restaurant meals, metro pass, private health insurance — runs closer to $1,200. That gap isn't a rounding error. It's an extra $26,000 a year staying in your pocket, compounding in investments while you enjoy eternal spring weather at 5,000 feet elevation.

Colombia has quietly become one of the hottest destinations for US expats, remote workers, and retirees who figured out that earning in dollars and spending in pesos is the closest thing to a legal cheat code in personal finance. But there's a tax trap most people stumble into — and unlike most expat destinations, Colombia has no tax treaty with the United States. One wrong move past the 183-day mark and two countries can each claim your income. This guide tells you exactly how to structure your time and finances so neither scenario catches you off guard.

Why Colombia Has 1.6 Million US Visitors a Year — And Growing Expat Numbers

Colombia has spent a decade aggressively rebranding itself, and it's working. Medellín was named one of the most innovative cities in the world by the Wall Street Journal (beating out New York and Tel Aviv). Bogotá has one of the largest urban cycling networks in the Americas. The country has stable internet infrastructure, direct flights to Miami in under 3 hours, and a population that is genuinely welcoming of foreigners.

The numbers bear out the trend. The US State Department estimates over 1 million Americans visit Colombia annually, and the expat community — those who have actually relocated — is growing rapidly, concentrated in Medellín's El Poblado, Bogotá's Chapinero and Usaquén, and coastal Cartagena. Cost of living is 51% lower than the US average overall, with rent running 71% cheaper. A quality one-bedroom in Medellín's nicest neighborhood costs what a parking spot rents for in San Francisco.

But Colombia isn't a tax haven. It's a regular tax country with a progressive income tax that tops out at 39% — higher than most US states combined with federal rates at middle-income levels. The smart move is understanding exactly where the line is drawn.

The 183-Day Tax Residency Trap

Colombia's tax residency threshold is 183 calendar days within any 365-day rolling window — not a calendar year. The 365-day window doesn't reset on January 1st. If you arrive September 1 and stay past February 28, you may cross the threshold before the year ends.

Once you're a Colombian tax resident, Colombia taxes your worldwide income at progressive rates. This is the key distinction. Unlike territorial tax countries (Panama, Paraguay, Georgia) where foreign income stays untouched, Colombia follows a residence-based model identical in structure to the US system. Two countries, both taxing worldwide income, no treaty to prevent overlap. That's how you end up with a tax bill on both sides of the equator.

The practical playbook for most digital nomads and early retirees: stay under 183 days in Colombia per rolling year. Non-residents only owe Colombian tax on Colombian-source income, which at a flat 35% withholding rate may not even apply to you if you're earning from US clients or a US business entity.

If you plan to settle permanently — over 183 days — you'll need to use the Foreign Tax Credit (not FEIE) to offset Colombian taxes paid against your US bill. Read the full breakdown at US Expat Banking & Taxes Guide and the FEIE vs FTC decision framework.

Colombia's Income Tax Brackets (2026)

For residents, Colombia uses a progressive bracket system denominated in UVT units (Unidad de Valor Tributario). For 2026, 1 UVT equals approximately COP 49,799, with the exchange rate running roughly 4,200 COP per USD.

| Annual Income (USD approx.) | Colombia Tax Rate |

|---|---|

| Up to ~$14,000 | 0% |

| $14,001 – $22,000 | 19% |

| $22,001 – $55,000 | 28% |

| $55,001 – $195,000 | 33% |

| Over $195,000 | 39% |

For non-residents earning Colombian-source income, a flat 35% withholding applies. If you're working entirely for US-based clients as a non-resident, Colombia doesn't touch your income at all.

What You Still Owe the IRS

Moving to Colombia does not reduce your US tax obligations one peso. As a US citizen, you file a US return every year regardless of where you live. What changes is your strategy for reducing that bill.

Foreign Earned Income Exclusion (FEIE): Exclude up to $130,000 of foreign-earned income using either the physical presence test (330 days outside the US in a 365-day period) or the bona fide residence test. Passive income — dividends, capital gains, rental income — is never excluded by FEIE. See the deep dive at How to Pay Zero Federal Tax as a US Expat.

Foreign Tax Credit (FTC): If you become a Colombian tax resident and pay Colombian income tax, you can credit those taxes dollar-for-dollar against your US tax liability. With Colombian rates running 28–33% for mid-range earners, the FTC often wipes out most or all of the US liability. But you can't use both FEIE and FTC on the same dollars simultaneously.

FBAR & FATCA: Colombian bank accounts over $10,000 trigger FBAR reporting. Colombian investment or brokerage accounts trigger FATCA Form 8938. Neither is a tax — both are reporting requirements with penalties up to $10,000 per violation for non-willful failures. Keep records current.

Maintaining a US virtual mailbox preserves your US banking relationships, credit score, and IRS correspondence address. Traveling Mailbox gives you a real US street address in 50+ cities with mail scanning and check deposits for $15/month — the baseline setup for any serious expat.

Colombia Visa Breakdown: Which One Fits

Colombia's visa system runs on three tiers: V (visitor, short-term), M (migrant, multi-year), and R (resident, permanent). Here's what actually matters for US expats planning a real move.

| Visa Type | Income Requirement | Duration | Key Notes |

|---|---|---|---|

| Digital Nomad (V) | ~$1,400/month from foreign sources | 2 years | $52 application fee; remote work only |

| Pensionado / Retirement (M) | ~$1,400/month pension | 3 years (renewable) | Leads to PR after 2 years on M visa |

| Rentista (M) | ~$4,700/month passive income | 2 years (renewable) | No active work allowed; passive income only |

| Investor / Property (M) | Property or business worth ~$35,000+ | 3 years (renewable) | 100x SMMLV for business; property qualifies |

For most remote workers and freelancers, the Digital Nomad Visa is the entry point. The income threshold is low (3x the Colombian monthly minimum wage), the application fee is $52, and it's processed online through the Cancillería platform in 5–30 days. The detailed application walkthrough is over at colombiamove.com's nomad visa guide.

Retirees drawing Social Security or a pension should look at the Pensionado Visa. If your monthly pension exceeds $1,400, you qualify, and after two years on the M visa you can apply for permanent residency — a much faster track than most Latin American countries offer. For more on stretching Social Security in Colombia, see Retire Abroad: Where Social Security Goes 5x Further.

The Rentista Visa has one expensive catch: Colombia requires approximately $4,700/month in demonstrable passive income — dividends, rental income, or similar. That's a high bar designed to ensure you're not quietly working Colombian clients under the radar. Most freelancers don't qualify; most retirees with significant investment portfolios do.

Property buyers get another path: purchase real estate worth at least 100x the Colombian monthly minimum wage (roughly $35,000 at current rates) and you qualify for an Investor M Visa. With property prices in Medellín still well below comparable US cities, this doubles as a real estate strategy. For the full global digital nomad and visa landscape, see Digital Nomad Visas Ranked: 15 Best Countries.

Cost of Living: Medellín, Bogotá, Cartagena

Medellín: The Expat Capital

Medellín is the first stop for most new arrivals. Average temperature stays at 72°F (22°C) year-round — locals call it the ciudad de la eterna primavera. The metro system plus cable cars costs $35/month for unlimited rides. The city has fast fiber internet widely available, a booming coworking scene, and the highest concentration of English-speaking professionals in the country.

1-BR in El Poblado (nicest expat area): $600–$1,000/month furnished

In Laureles (local, hip, 30% cheaper): $400–$650/month

Monthly groceries for one: $200–$280

Comida corriente lunch (restaurant): $3–6

Dinner for two, mid-range: $20–40

Total monthly budget: $1,000–$1,500

The most detailed breakdown of Medellin's actual costs — by neighborhood, lifestyle tier, and spending category — is at colombiamove.com's Medellín budget breakdown.

Bogotá: The Business Hub

Bogotá sits at 8,600 feet elevation — bring a jacket. The capital is Colombia's financial center, which matters if you need in-person banking relationships, legal services, or professional networking. Costs run about 10–15% higher than Medellín for comparable neighborhoods. Chapinero, Usaquén, and Zona Rosa have robust expat communities. Monthly budget: $1,200–$1,800.

Cartagena: Coastal Heat, Higher Prices

Cartagena is where you go if ocean access outweighs budget discipline. As a tourist hub, prices are inflated by visitor demand — expect to pay 20–30% more than Medellín for comparable housing. Monthly budget: $1,400–$2,200. Worth it for the lifestyle; not the right call if maximizing geographic arbitrage is the goal.

Banking and Money for Colombia Expats

Keep a US bank account active. This is non-negotiable for maintaining your credit score, receiving transfers, and accessing dollar savings. Charles Schwab's international checking account is the gold standard: no foreign transaction fees, unlimited ATM fee rebates worldwide, and no minimum balance. Open it before you leave. Open a Schwab account here.

Opening a Colombian bank account requires a cédula extranjería (foreign ID tied to your visa) or at minimum a valid visa stamp. Most major banks — Bancolombia, Davivienda, BBVA Colombia — require this. The full breakdown of foreign-friendly options is at Best Banks in Colombia for Foreigners.

For dollar-denominated savings and spending flexibility, ARQ Finance was built specifically for this problem. ARQ holds balances in USDC/EURc (stablecoins pegged to the dollar and euro), lets you swap to COP at competitive rates for daily spending, and earns up to 4% on your dollar balance. You can also accept USDT/USDC deposits from external wallets and access a Mastercard with cashback. Available in Colombia, Mexico, Argentina, and Brazil.

For sending money from the US to Colombia, Remitly consistently beats the alternatives on USD-to-COP transfers. Lock in the exchange rate at transfer time and funds typically arrive within minutes via bank deposit or mobile wallet.

Your US banking relationships depend on a valid US address on file. A virtual mailbox like Traveling Mailbox handles this — $15/month for a real US street address with mail scanning, so your bank, brokerage, and IRS correspondence always has a valid US destination.

Healthcare: Surprisingly Good Quality, Dramatically Lower Cost

Private clinics in Medellín and Bogotá routinely treat patients at a fraction of US prices. A specialist consultation runs $30–80, a dental cleaning $20–40, and major dental work (implants, crowns) at 70–80% below US rates. Medellín has become a significant medical tourism hub for cosmetic procedures, dentistry, and orthopedics — some expats specifically pick Colombia for the dental arbitrage alone.

For comprehensive international health insurance that covers Colombia and everywhere else you travel, SafetyWing Nomad Insurance runs $120–200/month for most US citizens under 40. Colombia also requires proof of health insurance for most visa types — it's a condition of visa validity, not optional paperwork. For a detailed comparison of expat health options, see Expat Health Insurance: How I Pay $120/Month for Better Coverage.

The Geographic Arbitrage Math

A US remote worker earning $80,000/year and living in a mid-tier American city (Austin, Denver, Nashville) spends $42,000–$50,000 annually to maintain a comfortable life — leaving $30,000–$38,000 to save or invest.

That same income in Medellín, staying under the 183-day threshold and using FEIE to shield the earned income from US tax, results in roughly $15,000–$18,000 in annual expenses. That's $62,000–$65,000 available to invest — almost double the US scenario without earning an extra dollar. Compounded over 10 years at 8%, the Colombia-based worker accumulates $200,000+ more than the US-based counterpart purely through cost arbitrage.

For a deeper framework on structuring your finances around geographic arbitrage, see The Geographic Arbitrage Playbook: $2K/Month Buys a $6K Lifestyle. And for the complete picture on moving to Colombia — neighborhoods, healthcare, schools, and on-the-ground logistics — colombiamove.com's relocation guide is the most comprehensive US-focused resource on the subject.

On-the-Ground Resources Once You're There

Colombia's expat infrastructure has matured significantly. The colombiamove.com platform runs several tools worth bookmarking:

- Trabajo Colombia — free jobs and services board for expats; post work, hire local professionals, or find freelance gigs

- Colombia Jobs — for finding or posting formal employment in Colombia

- Colombia Classifieds — buy, sell, or rent real estate and goods

The Bottom Line

Most people who come to Medellín for three months end up looking at apartments. The quality of life — weather, food, social scene, cost efficiency — creates genuine attachment. The path to permanent residency is faster than most competitors (2 years on an M visa), the visa income thresholds are low, and the gateway to South America is genuinely useful if you want geographic flexibility across the continent.

The two traps to avoid are the 183-day tax residency threshold (if you're not prepared to become a Colombian tax resident) and the no-treaty status with the US (which requires careful selection of FEIE vs FTC depending on your income type and amount). Both are manageable with planning. Neither is a reason to pass on a country where $1,300 a month buys a lifestyle that $4,000 barely approximates in a US city.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and vary by individual circumstance. Consult a qualified tax professional with experience in US expat taxation and Colombian tax law before making residency, visa, or financial decisions. ARQ Finance is not an investment advisor. Affiliate links in this post may earn a commission at no extra cost to you.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.