Charles Schwab for Expats: Bank Free in Any Country

Your bank hides ,400/year in exchange rate markups. Charles Schwab eliminates ATM fees worldwide, charges zero FX fees, and has no minimum balance.

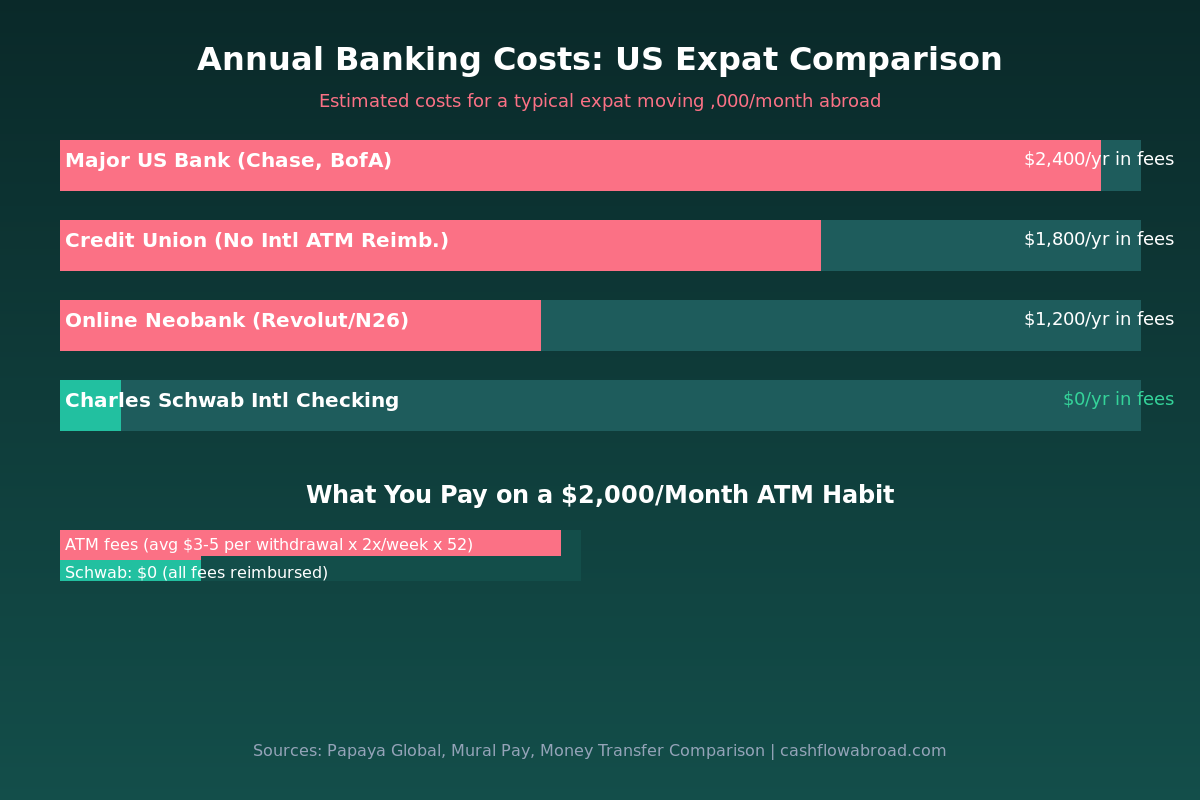

Stop losing $2,400/year to hidden banking fees. Charles Schwab reimburses all ATM fees worldwide with zero foreign transaction fees for expats.

Your bank is probably charging you $2,400 a year in fees you never see on any statement. Not because it's hiding them—it's doing something cleverer: it bakes the cost directly into the exchange rate and calls the transfer "free."

For expats moving money abroad or withdrawing local cash regularly, this invisible markup compounds fast. Someone pulling $2,000/month from ATMs abroad through a major US bank pays $3–5 per withdrawal in ATM fees, plus a 1–3% foreign transaction fee on every purchase, plus a 2–4% exchange rate markup on transfers. Run those numbers for 12 months and you're looking at $1,800–$2,600 gone with nothing to show for it.

There's one account that eliminates all of this: the Charles Schwab Bank Investor Checking account. It refunds every ATM fee worldwide with no cap, charges zero foreign transaction fees, and applies no currency conversion markup at withdrawal. Here's exactly how it works and how to set one up from anywhere in the world.

The Hidden Fee Problem Nobody Warns You About

Most people budget for the obvious fees: the $30 outgoing wire, the $15 incoming wire, the $5 ATM charge. Those hurt but at least you can see them. The truly expensive fee is the one your bank never discloses as a fee at all.

Banks set their own exchange rates. The real, interbank mid-market rate—what Reuters or Google shows—is what banks actually use with each other. What they quote retail customers is a marked-up version. The spread is typically 2–5% on any conversion. On a $5,000 international transfer, a 3% markup costs you $150 per transaction. Do that monthly and you've lost $1,800 in a year to a fee that never appeared on your statement.

Even services marketed as "fee-free" play this game. The flat fee disappears; the exchange rate gets worse. The total cost is often higher than just paying the flat fee at a bank with a better rate.

| Fee Type | Typical Major Bank | Charles Schwab |

|---|---|---|

| ATM fee reimbursement | None (or capped at $5–10/mo) | Unlimited worldwide |

| Foreign transaction fee | 1–3% per purchase | 0% |

| Currency conversion markup | 2–4% above mid-market | ~0% (Visa network rate) |

| Monthly account fee | $12–$35 | $0 |

| Minimum balance | $1,500–$25,000 | $0 |

How Charles Schwab Actually Works Abroad

The Schwab Bank Investor Checking account comes with a Visa Platinum debit card. When you withdraw cash from any Visa-accepting ATM anywhere in the world, Schwab charges you nothing and reimburses whatever fee the local ATM operator charged—credited back to your account at the end of the same billing month.

The exchange rate Schwab uses is the Visa network rate, which tracks closely to the mid-market rate with a spread typically under 0.5%. This is categorically different from the 2–4% markup a bank like Chase or Bank of America applies.

One critical caveat: if the foreign ATM offers to charge you in US dollars instead of local currency—called Dynamic Currency Conversion (DCC)—always decline. Always choose local currency. DCC is a third-party markup of 3–5% that Schwab explicitly does not reimburse, because it's not technically an ATM fee. The machine is doing the conversion at a terrible rate. Always let Schwab's Visa network handle it instead.

Opening Schwab from Abroad: The Actual Process

Contrary to what many expat forums say, Schwab does not require a US address. Their international program specifically accommodates US citizens living abroad. Here's what the application actually requires:

- Valid US passport (or government-issued photo ID)

- Proof of foreign residence: utility bill, bank statement, or lease—must show your name, foreign address, and date

- SSN required: this is a US-regulated account; the IRS requires it for all US citizens regardless of where they live

- Brokerage account: you must open a Schwab One brokerage account simultaneously (free, $0 minimum—it's bundled)

- Processing time: 3 days to 2 weeks for international applicants

- No minimum deposit to open; fund via ACH or wire after approval

If you're still in the US, open the account before you leave—it's faster. If you're already abroad, the international application works fine with the documentation above. Apply via the Charles Schwab international referral link.

The Schwab + Remitly Combination: Zero Leakage in Either Direction

Schwab is unbeatable for pulling local currency from ATMs and paying for things in foreign currencies. Where it falls short is sending money internationally—outgoing wire transfers cost $25 per transaction, which adds up if you're paying rent or moving money to family regularly.

The fix: use Remitly for outbound international transfers. Remitly offers competitive exchange rates with transparent fees—no hidden markup. Delivery to major corridors (Mexico, Colombia, Philippines, India, Europe) is often same-day or next-business-day.

Together, the two tools cover every direction:

- Withdrawing local currency: Schwab ATM, zero fees

- Sending money internationally: Remitly, low transparent fees

- US subscriptions and purchases: Schwab debit card, zero foreign transaction fees

For a deeper breakdown of transfer cost comparisons, see our expat money transfer guide.

The One Complication: You Still Need a US Address

Even though Schwab accommodates international applicants with foreign addresses, many US financial institutions, credit card issuers, and state tax authorities still require a permanent US street address on file. A P.O. box doesn't count. Using a family member's address works until it creates address mismatch issues with credit bureaus.

The cleanest solution is a virtual mailbox service. Traveling Mailbox provides a real US street address in 50+ cities, scans incoming mail on request, and can deposit checks—starting at $15/month. It's essential for maintaining a clean US banking setup, receiving IRS correspondence, and preserving state domicile while living abroad. Full details in our virtual mailbox guide for expats.

The Overlooked Bonus: Schwab as an Expat Brokerage

Because you're required to open the Schwab One brokerage account alongside checking, you might as well use it for investing. For expats, it's one of the few US brokerages that still accepts accounts with international addresses—many others (Fidelity, Vanguard) have closed accounts held by people who moved abroad.

Key features relevant for expats:

- $0 commissions on US-listed stocks and ETFs

- $0 account minimums

- SIPC protection up to $500,000 for eligible securities

- Access to international equity markets through the Schwab Global Account program

One critical warning for US expats: if you invest in foreign-domiciled funds or ETFs (anything not listed on a US exchange), you may trigger Passive Foreign Investment Company (PFIC) rules—one of the most punishing provisions in the US tax code. Stick to US-domiciled ETFs from Vanguard, iShares, or SPDR and you avoid this entirely. Our expat investing and PFIC guide covers this in detail.

The Full Expat Banking Stack

Schwab handles most of what expats need, but not everything. Here's how a complete setup looks:

| Use Case | Best Tool | Cost |

|---|---|---|

| ATM withdrawals abroad | Charles Schwab | $0 |

| Sending money internationally | Remitly | Low transparent fee |

| US business banking | Mercury | $0/month |

| US street address abroad | Traveling Mailbox | From $15/month |

| Dollar balances in Latin America | ARQ Finance | Free (earn up to 4% yield) |

| Data connectivity abroad | Saily eSIM | From ~$4/week |

Mercury is worth highlighting separately. If you run a US LLC or corporation from abroad, Mercury handles ACH, wires, and international transfers cleanly without the legacy bank friction. It's become the default for location-independent founders. Read our guide on running a US business while living abroad for the full setup.

The Real Cost Comparison Over Time

Let's make this concrete. Assume you're withdrawing $2,000/month from ATMs and spending $1,000/month locally in foreign currency—a modest expat budget.

| Bank | Annual ATM Fees | Annual FX Markup | Total Annual Cost |

|---|---|---|---|

| Chase Total Checking | ~$520 (avg $5/withdrawal, 2x/week) | ~$1,080 (3% on $36K in ATM cash) | $1,600+ |

| Bank of America | ~$500 ($5/intl ATM) | ~$1,440 (4% on $36K) | $1,940+ |

| Charles Schwab | $0 (fully reimbursed) | ~$0 (Visa rate ≈ mid-market) | $0 |

Over five years abroad, the difference between using Bank of America and Schwab at this spending level is approximately $9,700. That's not a rounding error—it's a real number that funds travel, investments, or simply stays in your account.

Bottom Line

The Schwab Bank Investor Checking account has been quietly recommended in expat forums for over a decade because nothing better has come along. No monthly fees, no minimums, unlimited ATM reimbursement, zero foreign transaction fees. The account is free to open and the international application process, while not instant, is straightforward.

Set it up before you move if possible. If you're already abroad, gather your foreign proof of residence and apply through the international portal. Add Remitly for outbound transfers, a virtual mailbox for your US address, and Mercury if you have a US business entity—and your banking overhead drops to close to zero per year.

Open your Schwab account: Charles Schwab International Checking (referral link).

Financial disclaimer: This post is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Banking products, fees, and eligibility requirements can change—verify current details directly with Charles Schwab and all other providers before making decisions. Some links in this post are affiliate links; we may earn a commission at no additional cost to you. Consult a qualified financial advisor for personalized guidance.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

The 3 Bank Accounts Every US Expat Actually Needs

Stop paying $2,400/year in bank fees abroad. This 3-account expat banking setup—Schwab, Mercury, Traveling Mailbox—costs just $180/year.

Expat Tax & FinanceMay 10, 2026

Expat Tax & FinanceMay 10, 2026

FATCA vs. GDPR: Why US Expats Lose European Banks

Belgium declared FATCA illegal under GDPR. Now EU banks face a catch-22. Here is what US expats need to know about European banking in 2026.

Expat Tax & FinanceMay 8, 2026

Expat Tax & FinanceMay 8, 2026

Why Foreign Banks Refuse American Expats (And What to Do)

FATCA costs banks $16,600 per American account. Learn why foreign banks refuse US expats and which banking solutions actually work abroad.