Brazil for US Expats: Taxes, Visas & the $1,500/Month Life

Zero. Not a reduced-withholding clause, not a tie-breaker rule, not a pension exemption. Brazil doesn't. That's the risk.

Zero. Not a reduced-withholding clause, not a tie-breaker rule, not a pension exemption. Brazil doesn't. That's the risk.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's a fact that stops most expat planners cold: Brazil is the fifth-largest country on earth, home to an estimated 80,000+ American residents — and the United States has no income tax treaty with Brazil. Zero. Not a reduced-withholding clause, not a tie-breaker rule, not a pension exemption. Every other major expat destination in Latin America (Mexico, Costa Rica, Chile, Colombia) has some form of tax agreement. Brazil doesn't. That's the risk. The reward is a country where a comfortable, full-flavored life in a coastal city runs $1,200–$1,800/month, the USD buys nearly 5.6 Brazilian reais, and the world's largest tropical country is practically in your backyard.

This guide covers the real numbers: visa options, tax exposure on both sides of the equation, what cities cost, and what to set up before you land.

Visa Options for Americans

As of April 2025, US citizens can no longer enter Brazil visa-free. You now need an eVisa before departure — apply online through Brazil's immigration portal, it costs around $80, and approval takes 3–10 business days. Once you have it, you can stay up to 90 days, extendable to 180 days per calendar year. That's your baseline for testing the country.

For longer stays, Brazil offers three realistic paths for Americans:

Digital Nomad Visa (VITEM XIV)

Brazil's digital nomad visa requires proof of at least $1,500/month in remote income or $18,000 in savings. You must work for a company or clients outside Brazil and carry private health insurance valid in the country. The visa is valid for one year, renewable once for a second year — after two years, you can apply for temporary residency. Processing takes 4–8 weeks through a Brazilian consulate in the US. Add dependents at an extra $500/month per person in income documentation.

Retirement Visa

Men over 65 and women over 60 can apply for a retirement visa by demonstrating a pension income of $2,000/month transferred to a Brazilian bank account. The visa grants a one-year stay, renewable, and converts to permanent residency after four years. No minimum asset requirement, no lump-sum deposit — just proven passive income. One of the more accessible retirement visas in South America.

Permanent Residency Paths

Outside standard visas, Americans commonly reach permanent residency through a Brazilian spouse or partner (fastest path), through investment (minimum ~$150,000 USD in a Brazilian company), or by converting temporary residency to permanent after four consecutive years. Permanent residency holders receive a CPF number — Brazil's equivalent of a Social Security number — which unlocks full banking access and local services.

Cost of Living: What $1,500/Month Actually Gets You

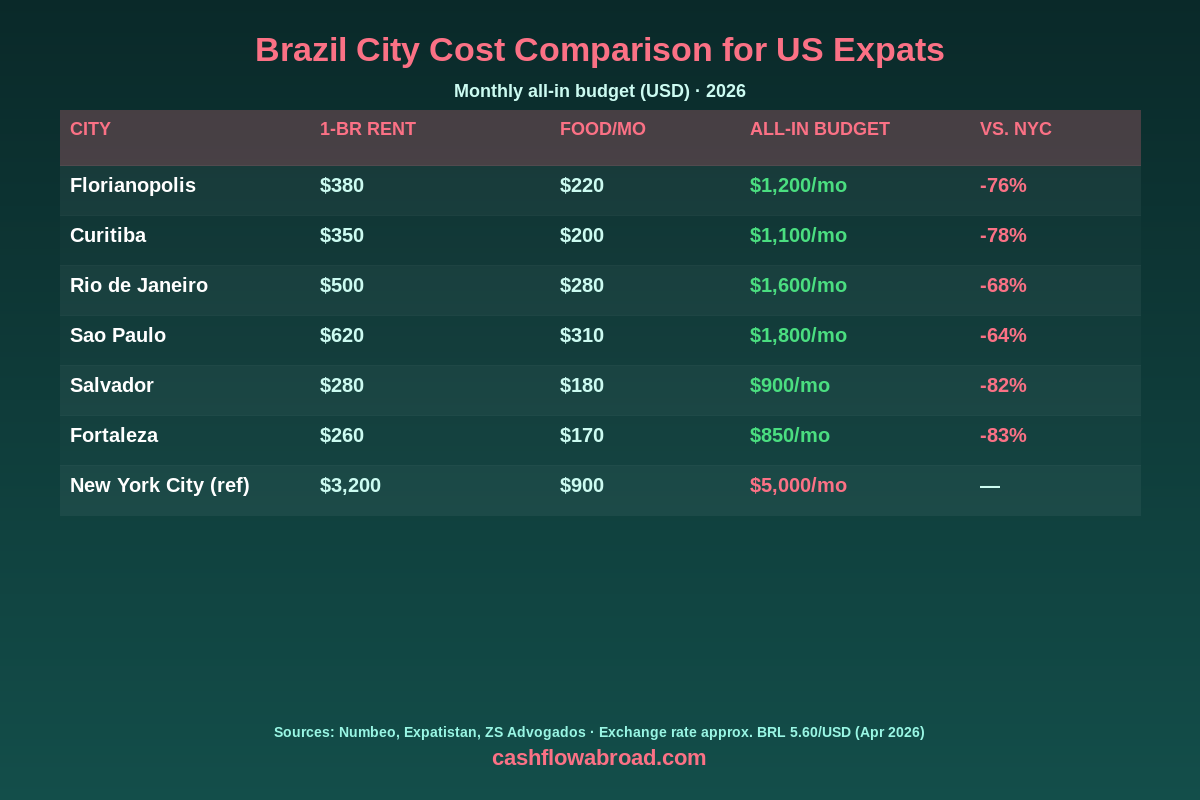

The exchange rate does heavy lifting here. At roughly BRL 5.60 per dollar in April 2026, American incomes stretch dramatically. A sit-down restaurant meal costs R$45–65 ($8–$12). A one-bedroom apartment in a desirable Florianópolis neighborhood rents for R$2,100–2,800/month ($375–$500). Groceries for a single person run R$900–1,200/month ($160–$215).

| City | 1-BR Rent (USD) | Groceries/Mo | All-In Budget | vs. NYC |

|---|---|---|---|---|

| Florianópolis | $380–$500 | $180–$220 | $1,200–$1,500 | -76% |

| Curitiba | $320–$430 | $170–$200 | $1,100–$1,400 | -78% |

| Fortaleza | $240–$320 | $150–$180 | $850–$1,100 | -83% |

| Salvador | $260–$360 | $160–$190 | $900–$1,200 | -82% |

| Rio de Janeiro | $450–$620 | $220–$300 | $1,500–$1,900 | -68% |

| São Paulo | $550–$750 | $260–$340 | $1,700–$2,200 | -64% |

| New York City (ref) | $3,000–$3,500 | $700–$1,000 | $5,000–$6,500 | — |

Florianópolis is the expat darling — a coastal island with 42 beaches, a tech and startup scene, warm weather, and consistently ranked as Brazil's safest large city. Curitiba is cooler (average 65°F), beautifully planned, often called the most livable city in Brazil. Fortaleza offers beach living and near-zero winters at prices that border on absurd by any developed-world measure.

São Paulo is Brazil's financial capital — if you're building a business or need fast networking, the premium is justifiable. Rio has the lifestyle mystique but costs more in desirable neighborhoods; research specific barrios (Botafogo, Flamengo, Leblon) rather than the city broadly.

Brazilian Taxes: What You Owe as a Resident

Once you spend 183 days or more in Brazil in a calendar year — or establish a permanent home there — Brazil considers you a tax resident. As a tax resident, Brazil taxes your worldwide income. That means US rental income, Roth conversion income, brokerage dividends, and freelance earnings all become reportable to Brazil's Receita Federal.

Brazil's individual income tax, the IRPF, runs on a progressive scale:

| Monthly Income (BRL) | Monthly Income (USD approx.) | Rate |

|---|---|---|

| Up to R$2,428 | Up to ~$434 | 0% (exempt) |

| R$2,429 – R$3,751 | $435 – $670 | 7.5% |

| R$3,752 – R$4,664 | $671 – $833 | 15% |

| R$4,665 – R$6,101 | $834 – $1,089 | 22.5% |

| Above R$6,101 | Above ~$1,090/mo | 27.5% |

The 2026 IRPF filing deadline (covering 2025 income) is May 29, 2026. You'll need a CPF number to file. Brazil recognizes a reciprocity principle with the US — it allows offsetting some Brazilian tax against US taxes paid on the same income — but this is administrative practice, not enforceable treaty law.

US Taxes: You Still File, No Matter What

Moving to Brazil doesn't end your IRS obligations. US citizens owe federal returns regardless of residence. Two tools do the heavy lifting:

Foreign Earned Income Exclusion (FEIE)

For tax year 2025, qualifying expats can exclude up to $130,000 of foreign earned income from US taxes using Form 2555. You qualify via the bona fide residence test (official residency established) or the physical presence test (330+ days outside the US in any 12-month period). FEIE only covers earned income — wages, freelance, self-employment. It does not cover passive income: dividends, interest, capital gains, rental income.

Watch for the FEIE trap: if you exclude all earned income via FEIE, you have zero earned income for Roth IRA contribution purposes. Brazil-based expats making $90,000/year in freelance income and using FEIE can legally owe $0 in US federal income tax — but they also can't contribute to a Roth that year.

Foreign Tax Credit (FTC)

File Form 1116 to claim a dollar-for-dollar credit against US taxes for Brazilian income tax paid on the same income. Since Brazil's 27.5% top rate is lower than the US 37% top rate, the FTC often leaves some US tax still owed at high income levels. For passive income — which FEIE doesn't cover — the FTC is the primary tool. Most expats combine both: FEIE for earned income under the exclusion limit, FTC for passive income. See the complete US expat tax guide for the FBAR and FATCA layer on top.

The No-Treaty Problem, Explained

Brazil is the only major expat destination in the Americas with no comprehensive US income tax treaty. What that actually means in practice:

- No pension protection — US Social Security income could be taxable in Brazil with no exemption to invoke

- No tie-breaker rules — if both countries claim you as a tax resident simultaneously, there's no treaty mechanism to resolve the dispute

- No reduced withholding — dividends from Brazilian companies face full domestic withholding rates

- No mutual agreement procedure — if you're double-taxed, there's no formal diplomatic appeal process

This doesn't make Brazil unlivable from a tax standpoint. The FEIE and FTC still do real work. But unlike moving to Mexico, Costa Rica, or Portugal — where treaty provisions backstop your planning — in Brazil you're working without a net. A CPA who specifically handles US-Brazil dual-filers is worth hiring before your first Brazilian tax year closes.

Banking Setup: US and Brazilian Accounts

Before you leave the US, lock down your banking infrastructure. Many US banks and brokerages quietly close accounts when they discover you've relocated abroad. Open a Charles Schwab International account before departure: free ATM withdrawals worldwide, no foreign transaction fees, and no tendency to close accounts for living abroad. Mercury works well for freelancers and business owners who need a US bank that won't flag an overseas IP address.

You'll need to maintain a US mailing address for banking, IRS correspondence, and state domicile purposes. A Traveling Mailbox provides a real US street address in 50+ cities — mail gets scanned and accessible online, checks can be deposited remotely. Essential for keeping US financial accounts active and your IRS address current. The virtual mailbox guide walks through the full setup.

For Brazilian banking: once you have a CPF number, Nubank is the easiest entry point. English-language app, low friction on documentation, and a debit card that works everywhere. You'll need your CPF, passport, Brazilian address, and proof of income. For USD-to-BRL transfers, Remitly offers competitive rates with transparent fees — typically delivers within minutes.

Healthcare in Brazil

Brazil has universal public healthcare — the SUS (Sistema Único de Saúde) — technically open to residents including foreigners with a CPF. In major cities, SUS handles emergencies adequately. For routine care and specialist access without months-long waits, expats use private coverage.

Private Brazilian health plans (planos de saúde) run R$900–2,200/month ($160–$390) for solid individual coverage, varying by city and age. Most expats on the digital nomad visa arrive with international coverage that satisfies the visa requirement, then add local Brazilian insurance once they have a CPF and residency.

SafetyWing's Nomad Insurance starts around $56/month and covers travel medical needs globally — a solid bridge while establishing local coverage. See the expat health insurance guide for a full comparison of international options vs. local Brazilian plans.

Best Cities for US Expats

Florianópolis is the consensus pick for quality of life — a coastal island with 42 beaches, 300 sunny days per year, strong broadband infrastructure, and Brazil's most organized expat community. Property prices have risen but still land 35–45% below comparable beachside US cities.

Curitiba earns its "most livable city in Brazil" label from urban planning that actually works: bus rapid transit, a network of parks, real recycling infrastructure, and a temperate climate (65°F average). Lower costs than Floripa, strong safety reputation, and a food scene shaped by German and Italian immigrant culture.

Rio de Janeiro is the lifestyle pick — Copacabana sunsets, Carnaval, the world's most famous skyline. The trade-off: neighborhood selection matters enormously. Botafogo, Flamengo, Leblon, and Barra da Tijuca are expat-comfortable. Use 99 or Uber rather than relying on public transit for daily movement.

Fortaleza and Natal in the northeast offer beach living at prices that feel pre-gentrification. Year-round heat, excellent coastline, and growing expat communities from Europe and North America chasing the deepest possible dollar stretch.

What to Do Before You Move

- Apply for the Brazil eVisa — required for Americans; don't arrive at the airport without one

- Open Charles Schwab and Mercury — before leaving US soil; far harder after

- Set up a Traveling Mailbox — keeps your US address, bank correspondence, and IRS records intact

- Get international health insurance — required for the digital nomad visa; SafetyWing covers the bridge period

- Get a CPF number at a Brazilian consulate — unlocks banking, phone plans, and eventual tax filing in Brazil

- Hire a dual-filer CPA — the no-treaty situation means Brazil-specific advice matters more than in other expat destinations; nail your FEIE vs. FTC strategy before your first Brazil tax year closes

- Review your US state tax exposure — some states pursue income tax even when you're abroad. The geographic arbitrage playbook covers state domicile strategy alongside country selection

Bottom Line

Brazil is one of the most underrated expat destinations for Americans willing to do their homework. The geoarbitrage math is hard to argue with: a Florianópolis lifestyle that costs $1,400/month would run $5,000+ in a comparable US coastal city. The tax picture is more complex than treaty countries — but manageable with the right structure. The no-treaty issue isn't a dealbreaker; it's a reason to plan rather than improvise. If you've explored the geographic arbitrage playbook, Brazil deserves a serious place on your shortlist.

Financial disclaimer: This post is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws in both the US and Brazil change frequently. Consult a licensed tax professional familiar with US expat taxation and Brazilian tax law before making residency or financial decisions.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.