The Big Beautiful Bill: What US Expats Won and Lost

The OBBB passed — FEIE hit $132,900 and citizenship-based taxation survived untouched. Here's the full expat scorecard, plus the RBT bill that could change everything.

FEIE rose to $132,900 but citizenship-based taxation survived the OBBB unchanged. Full expat scorecard + why the RBT compliance clock is ticking.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Nine million Americans live outside the United States. Fewer than 1.1 million file US tax returns from foreign addresses each year. That compliance gap has existed for decades — and after the most ambitious US tax overhaul in a generation, the One Big Beautiful Bill Act (OBBB), it's still essentially unchanged.

If you were waiting for Congress to finally fix citizenship-based taxation — the rule that makes the US one of only two countries on Earth that taxes its citizens no matter where they live — the OBBB delivered roughly $6,400 worth of relief and a new fee you didn't ask for. Here's what actually happened, what it costs you, and why the next 12 months still matter more than the last three years.

What the OBBB Actually Passed for Expats

The OBBB was primarily a TCJA extension bill with additions. For the 9 million Americans abroad, here's the complete picture of what changed:

The FEIE Limit Got a Bump

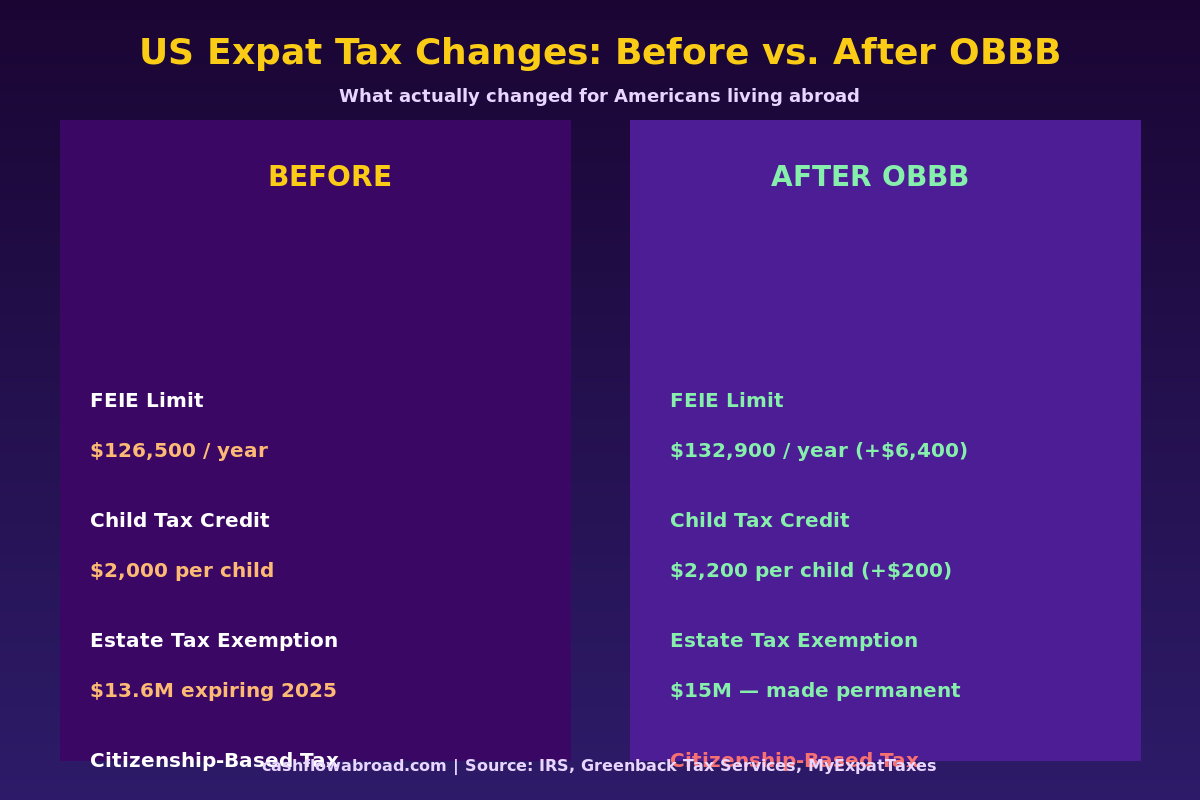

The Foreign Earned Income Exclusion for 2026 is $132,900 — up from roughly $126,500 the prior year. That $6,400 increase is inflation-indexed and represents one of the largest single-year jumps in recent history, but it's still an exclusion mechanism, not a fundamental reform. You're still filing. You're still reporting. You're still paying a CPA $500–$1,200 per year to navigate a system that 95% of the world doesn't impose on its emigrants.

Combined with the 2026 standard deduction, a single expat filing abroad can theoretically earn up to roughly $149,000 in foreign wages and pay zero US federal income tax. The key word is "theoretically" — rental income, dividends, capital gains, and self-employment income all have different treatment. See our full FEIE guide for the breakdowns that actually matter.

Estate Tax and Child Tax Credit Changes

Two provisions benefiting expats with significant assets or children abroad:

- Estate tax exemption: $15 million (up from $13.6 million), now made permanent. Previously, the doubled TCJA exemption was set to sunset at the end of 2025, which would have cut it in half. That didn't happen.

- Child Tax Credit: $2,200 per child (up from $2,000). The refundable portion was also expanded, though expats using FEIE often can't claim the refundable component — that limitation wasn't fixed.

The "Revenge Tax" Was Killed — and That's Actually Big

An early version of the OBBB included Section 899, a proposed surtax targeting foreign corporations with US-connected income from countries the US deemed to have "discriminatory" tax systems. It would have indirectly affected expats earning US-connected income through foreign entities registered in France, Germany, Canada, or the UK — while limiting their ability to use the Foreign Tax Credit to offset the new charge.

Section 899 was stripped from the final bill. That's a genuine win, even if most expats won't realize it. The FTC remains fully intact.

What the Bill Didn't Touch

The fundamental architecture of US international taxation is identical to what it was before the OBBB was signed. Citizenship-based taxation (CBT) remains in force. If you're a US citizen anywhere on Earth, the IRS can claim a share of your income. The only tools available to reduce that claim — the FEIE, the Foreign Tax Credit, the Foreign Housing Exclusion — all survived, but none of them eliminate the underlying filing obligation or the compliance cost that comes with it.

The Residence-Based Taxation bill championed by Rep. Darin LaHood (R-IL) and Sen. Todd Young (R-IN) was explicitly not included in the OBBB. Congressional procedural rules were the stated reason — the LaHood bill's treatment of FICA and self-employment tax for overseas Americans triggers the Senate's Byrd Rule, which blocks Social Security changes from passing through budget reconciliation. The bill needs regular order with bipartisan support, or a vehicle in a year-end tax extender package.

| Provision | Before OBBB | After OBBB | Net Change |

|---|---|---|---|

| FEIE Limit (2026) | ~$126,500 | $132,900 | +$6,400 |

| Child Tax Credit | $2,000/child | $2,200/child | +$200/child |

| Estate Tax Exemption | $13.6M (expiring) | $15M (permanent) | +$1.4M + certainty |

| Foreign Tax Credit | Intact | Intact (Section 899 killed) | Status quo protected |

| Citizenship-Based Taxation | In force | In force | Zero change |

| US Remittance Tax | None | 1% on cash transfers abroad | New burden (Jan 1, 2026) |

The New Burden Nobody Warned You About

Buried in the OBBB is a provision that directly hits people sending money internationally: a 1% federal remittance tax on outbound money transfers from US bank accounts using cash, money orders, or cashier's checks, effective January 1, 2026.

The practical impact for expats depends on how you move money. The tax targets cash-equivalent transfers — not standard wire transfers or ACH from US accounts. But it's a signal about where tax policy is trending, and it adds another reason to use direct wire transfers or established platforms rather than cash-conversion services when moving money between countries. For the full breakdown on keeping transfer costs minimal, see our expat money transfer guide. We specifically recommend Remitly for international transfers — it avoids the new tax and consistently offers better exchange rates than cash-based services.

The RBT Bill: Where It Actually Stands

The Residence-Based Taxation for Americans Abroad Act would do something no FEIE increase can: it would let qualifying Americans living outside the US elect to be treated as non-resident aliens for tax purposes, ending their obligation to pay US tax on foreign-source income entirely.

Here's how the LaHood bill works:

- Voluntary election — you choose to enter the RBT system; those who don't elect remain under CBT.

- Five years of compliance required — you must have five consecutive years of properly filed US tax returns to qualify. No exceptions.

- Departure tax for high-net-worth electors — individuals with net worth above a finalized threshold would pay a one-time "departure tax" on unrealized gains when they make the election.

- US-source income still taxed — you'd still owe US tax on US-sourced dividends, rental income from US property, and other domestic income streams. RBT ends the reach on foreign wages and foreign business income only.

As of mid-2026, the Joint Committee on Taxation is completing its revenue score — a mandatory step before formal reintroduction. Advocacy groups including American Citizens Abroad (ACA) and Tax Fairness for Americans Abroad expect the bill to be reintroduced in the current Congress, though passage before year-end is uncertain. The unprecedented combination of presidential support and bipartisan congressional backing gives the bill its best chance in decades.

| What RBT Would Mean for Expats | Current CBT System | Under Proposed RBT |

|---|---|---|

| Foreign wages (electors) | Taxable, offset by FEIE/FTC | Not taxable in the US |

| Foreign business income | Taxable (complex reporting) | Not taxable in the US |

| US dividends/interest | Taxable | Still taxable |

| Annual US tax filing | Required for all citizens | Simplified or eliminated for electors |

| Compliance cost | $450–$1,200/year | Significantly reduced |

| Eligibility requirement | N/A | 5 years of prior compliance |

Why You Should Start the 5-Year Compliance Clock Now

This is the part of the RBT story most expats miss: the eligibility gate is retroactive compliance, not future compliance. The bill requires five years of properly filed US tax returns as a condition of making the RBT election. That clock is running whether or not the bill has passed yet.

An estimated 7–8 million of the 9 million Americans abroad are not filing US returns. If the LaHood bill passes with a five-year lookback and you have unfiled returns, you would be locked out of the RBT election — stuck in CBT while compliant peers opt out entirely.

If you haven't been filing, the IRS has a streamlined compliance procedure specifically for non-willful non-filers abroad: the Streamlined Foreign Offshore Procedure. It involves filing three years of back returns and paying modest penalties. The window to get compliant before a potential bill passage is narrowing.

For maintaining your US presence while filing from abroad — including keeping a valid US address for IRS correspondence, state domicile, and banking — a virtual mailbox service is essential. Traveling Mailbox gives you a real US street address in 50+ cities, mail scanning, and check deposits for around $15/month. It's what keeps your IRS filing address clean and your banking intact. See our full virtual mailbox guide for the complete setup.

Banking and Brokerage Under the New Rules

FBAR and FATCA reporting remain fully in force — the OBBB didn't touch either threshold. If you hold more than $10,000 in foreign financial accounts at any point in a calendar year, you're filing an FBAR. If your foreign assets exceed $200,000 (single filer abroad), you're filing Form 8938.

For US-based brokerage access while living abroad — the cleanest way to hold US equities without triggering PFIC rules — Charles Schwab International remains the standard. It offers free global ATM withdrawals, a US brokerage account that doesn't close when you move abroad, and no foreign transaction fees. For the full breakdown of which accounts actually stay open, see our expat brokerage guide.

For US banking that's built for remote founders and freelancers, Mercury separates business and personal finances cleanly. And for health coverage abroad — untouched by the OBBB — SafetyWing starts at around $45/month for solid international coverage. See the full expat health insurance guide for comparisons.

The Action List

The OBBB passed. Citizenship-based taxation survived. The RBT bill is pending. Here's what to do:

- File your current-year return on time. Every compliant year is one year closer to the five-year RBT eligibility window. The FEIE limit is $132,900 — make sure you're claiming it.

- Catch up if you're behind. Use the IRS Streamlined Foreign Offshore Procedure to back-file without criminal exposure. Three years of returns clears most compliance gaps.

- Audit your transfer method. The new 1% remittance tax doesn't hit electronic wire transfers, but verify how your current service moves money. Cash-based methods now carry an added federal charge.

- Lock in a US address. You need one for IRS correspondence, state domicile maintenance, and banking. Traveling Mailbox handles it for $15/month.

- Watch the LaHood bill timeline. If it passes with a five-year lookback and you've been filing, you'll have the option to opt out of CBT entirely — a potentially life-changing financial decision that requires preparation, not a last-minute scramble.

The Bottom Line

The One Big Beautiful Bill gave American expats a higher FEIE, a slightly better Child Tax Credit, a more secure estate tax exemption, and one meaningful defensive win in the removal of Section 899. It also added a 1% remittance tax on cash-based international transfers. The foundational problem — the US taxing its citizens on worldwide income regardless of where they live — was not addressed.

That problem has its best legislative advocate in years. The preparation window is open. The compliance clock is ticking. Being ready isn't optional if you want to opt out when the door finally opens.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. US tax law is complex and fact-specific. Consult a qualified CPA or tax attorney before making decisions based on this content. FEIE thresholds and legislative details are based on publicly available information current as of the date of publication and are subject to change.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Moving Abroad Mid-Year: Maximize Your Tax Benefits

Moving in Q4 instead of Q1 costs you up to $30K in FEIE exclusions. Learn how pro-ration works, state tax traps, and FBAR obligations in year one.

Expat Tax & FinanceMay 26, 2026

Expat Tax & FinanceMay 26, 2026

How Expats Legally Pay $0/Month on Student Loans

Use the FEIE + IBR combination to reduce student loan payments to $0/month while living abroad. SAVE is dead — here is what works in 2026.